Trumps New Tariff Wave Hits Sentiment, PCE Data Eyed

Asian stocks edged lower today as investors digested fresh U.S. tariff announcements from President Donald Trump and tempered expectations for aggressive Fed easing. Risk appetite softened, with trade uncertainty once again colliding with questions over monetary policy.

At the Fed, officials remain hesitant to commit to a firm easing path. Outside of Governor Stephen Miran’s calls for deeper and faster moves, most policymakers are emphasizing data dependence. The message is clear: cuts are still coming, but the pace and scale will be dictated by incoming numbers.

As it stands, markets see back-to-back easing in October as highly likely, with futures pricing an 87.7% probability of a cut. However, the chance of another move in December has slipped to 62%, reflecting unease over whether the Fed will need to accelerate the pace of its cuts.

That puts sharper focus on today’s PCE inflation release, the Fed’s preferred gauge. A stronger-than-expected print could dampen easing expectations further, while a soft outcome could revive bets for a December cut. Even so, the decisive test will come with next week’s non-farm payrolls, which will give the clearest signal on labor market health.

On the trade front, Trump announced sweeping new duties, including 100% tariffs on imported branded drugs, 25% on heavy-duty trucks, and 50% on kitchen cabinets. Bathroom vanities and upholstered furniture will also face tariffs of 50% and 30% respectively, with all measures set to take effect on October 1. Uncertainty remains high as Trump did not clarify whether the duties would be layered on top of existing tariffs or if key trading partners with agreements—such as the EU or Japan—would be exempt.

In currencies, Dollar has emerged as the week’s strongest performer, followed by Swiss Franc and Euro. At the bottom, Kiwi leads losses, trailed by Yen and Loonie, while Sterling and Aussie hold middle ground.

In Asia, Nikkei fell -0.64%. Hong Kong HSI is down -0.56%. China Shanghai SSE is down -0.28%. Singapore Strait Times is up 0.01%. Japan 10-year JGB yield rose 0.009 to 1.658. Overnight, DOW fell -0.38%. S&P 500 fell -0.50%. NASDAQ fell -0.50%. 10-year yield rose 0.025 to 4.172.

Fed’s Goolsbee cautions against front-loading cuts, Daly favors gradual approach

Speaking overnight, Chicago Fed President Austan Goolsbee noted he is “somewhat uneasy” with front-loading too many rate cuts based solely on slowing payroll growth. With inflation above 2% for nearly five years and moving “the wrong way,” he warned that simply assuming price pressures are transitory is a risky strategy.

Separately, San Francisco Fed President Mary Daly reiterated that further easing will likely be needed but emphasized a measured pace. She argued that cutting “a little bit more over time” while reassessing incoming data is the safer way to balance the Fed’s dual mandate.

Daly cautioned that moving too quickly could risk undermining either employment or price stability. A gradual approach, she said, allows the central bank to “actually get to a good achievement” by avoiding overcorrections.

Tokyo CPI core stays at 2.5% in September, core-core slows

Tokyo inflation came in softer than expected in September, with core CPI (ex-fresh food) unchanged at 2.5% yoy versus forecasts of 2.8% yoy. The moderation was largely attributed to measures by the metropolitan government, including cuts to childcare fees and water charges, easing some of the burden from rising living costs.

Core-core inflation, stripping out fresh food and energy, slowed sharply from 3.0% yoy to 2.5% yoy, while headline CPI was also steady at 2.5% yoy. Food inflation excluding fresh items cooled to 6.9% yoy from 7.4% yoy, highlighting a broadening slowdown in price pressures.

The weaker data may give the BoJ some breathing room, though markets still price another 25bps hike in the months ahead. Opinion remains divided on whether policymakers act as soon as October or hold off until January.

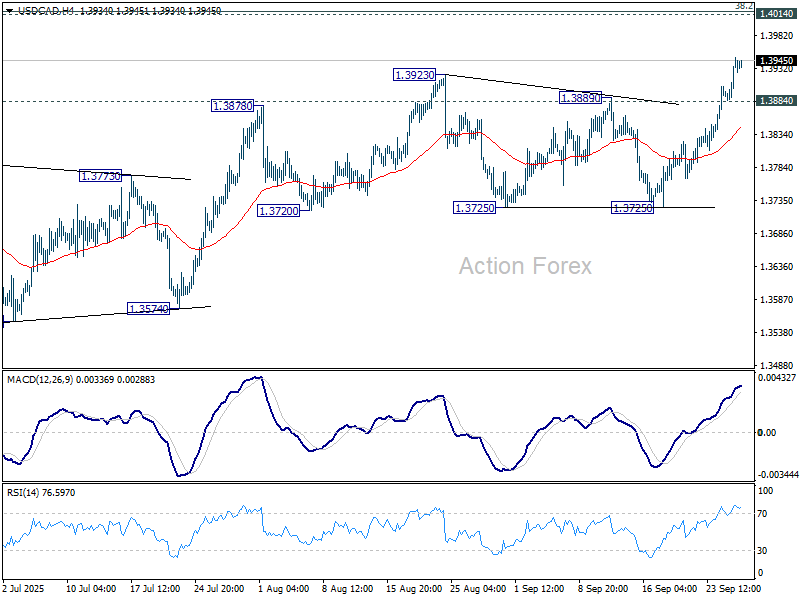

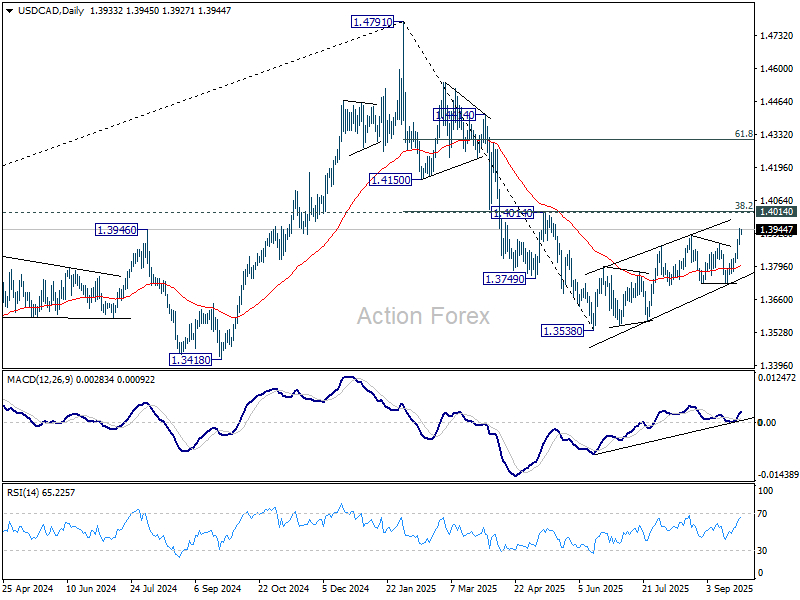

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3900; (P) 1.3925; (R1) 1.3965; More…

USD/CAD’s rally continues and the break of 1.3923 confirms resumption of whole rebound from 1.3538. Intraday bias stays on the upside for 1.4014 cluster resistance. Strong resistance is expected from there to limit upside to complete the corrective rise. On the downside, below 1.3884 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069. However, sustained break of 1.4014 will argue that fall from 1.4791 has completed, and bring stronger rally to 61.8% retracement at 1.4312.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more