Sterling Eases After CPI Miss, Overall Markets Quiet

The foreign exchange market traded quietly today, with investors reluctant to take fresh major positions. With risk sentiment mixed and volatility muted, most major pairs remained confined to familiar ranges

The British Pound was under mild pressure as traders raised their bets on another BoE rate cut later this year, albeit not in November. Euro and Swiss Franc also traded on the defensive, mirroring the Pound’s mild weakness.

In contrast, commodity currencies held up better. Aussie, Kiwi, and Loonie all registered modest gains. Dollar and Japanese Yen hovered in the middle of the performance board.

Overall trading activity might stay low until key data releases at the end of the week including the U.S. CPI on Friday and a series of PMI surveys from major economies.

Beyond the data focus, trade diplomacy was also in the spotlight. U.S. Trade Representative Jamieson Greer and Treasury Secretary Scott Bessent were set to travel to Malaysia for talks with Chinese officials over what Washington described as “incredibly aggressive” restrictions on rare earth exports.

Bessent said there remains a potential slot for a meeting between President Trump and President Xi, though it would depend on mutual readiness. Greer added that while China’s actions breached earlier commitments to maintain rare earth supply, there was still a “good landing zone” for rebalancing trade ties.

In Europe, at the time of writing, FTSE is up 0.96%. DAX is down -0.18%. CAC is down -0.30%. UK 10-year yield is down -0.084 at 4.404. Germany 10-year yield is up 0.008 at 2.567. Earlier in Asia, Nikkei fell -0.02%. Hong Kong HSI fell -0.94%. China Shanghai SSE fell -0.07%. Singapore Strait Times rose 0.29%. Japan 10-year JGB yield fell -0.008 to 1.655.

UK CPI at 3.8% in September, undershoots expectations of 4.0%

UK inflation came in softer than expected in September. Headline CPI was unchanged at 3.8% yoy, below consensus of 4.0%. Core CPI (excluding energy, food, alcohol and tobacco) eased to 3.5% from 3.6%.

Breakdowns showed a mixed picture under the surface. CPI goods component rose marginally from 2.8% yoy to 2.9%, highest since October 2023. Services inflation held unchanged at 4.7%.

On a monthly basis, consumer prices were flat, another sign that the inflation pulse has moderated heading into the final quarter of the year.

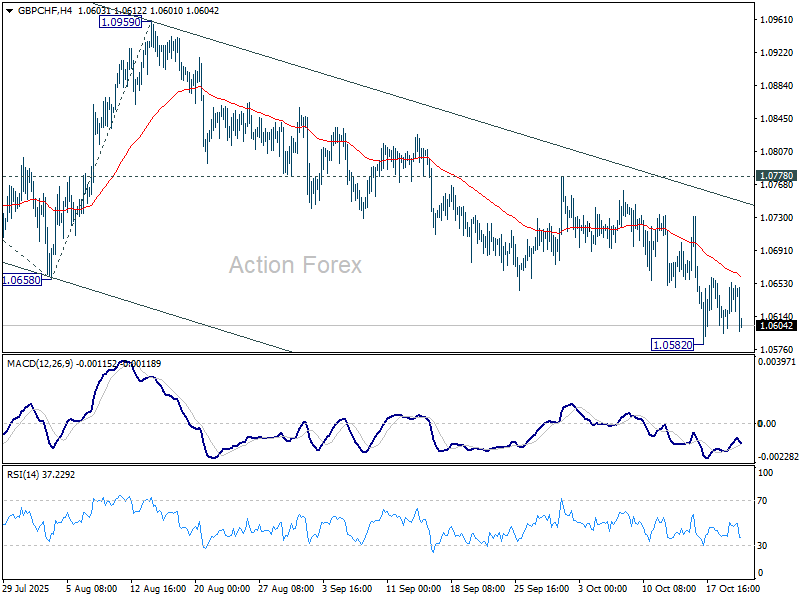

GBP/CHF dips but range holds as UK CPI not dovish enough

Sterling slipped today after softer-than-expected UK inflation data reinforced expectations that the BoE remains on track to cut rates again this year—though not as soon as the next meeting. A November pause still appears more likely, with solid reasons to wait until after the November 26 Budget and another round of inflation data before committing to further easing.

However, expectations for a December rate cut have strengthened notably. Interest-rate futures now assign roughly a 75% probability that the BoE will lower the Bank Rate to 3.75% from 4.00% at the December meeting—up from about 46% before the CPI release. Traders have also brought forward expectations for the next move, fully pricing a second 25-basis-point cut by February 2026, a month earlier than previously anticipated.

In the currency market, the Pound’s selloff was broad but relatively shallow. The muted reaction reflected that traders see the BoE cutting soon—but not urgently—keeping Sterling supported above key levels for now.

Technically, GBP/CHF is still holding above 1.0582 temporary lower despite today’s dip. Some more consolidations could still be seen. Nevertheless, near term outlook is staying firmly bearish with 1.0778 resistance intact. Break of 1.0582 will pave the way to 100% projection of 1.1204 to 1.0658 from 1.0959 at 1.0413.

Japan’s exports rise for first time in five months, but U.S. demand still weak

Japan’s exports rose in September for the first time in five months, signaling tentative recovery in external demand even as shipments to the U.S. continued to contract sharply.

Exports climbed 4.2% yoy to JPY 9.41T, slightly below expectations of 4.6%. The rebound was driven largely by strength in Asia, where exports jumped 9.2%, including a 5.8% rise to China. In contrast, shipments to the U.S. fell -13.3%, with auto exports down -24.2%, extending months of weakness despite being a smaller drop than August’s 28.4% decline.

Imports also grew faster than expected, rising 3.3% yoy to JPY 9.65T, compared with forecasts of 0.6%. As a result, Japan posted a trade deficit of JPY 234.6B.

The data come just weeks after Washington finalized a new trade agreement with Tokyo, implementing a 15% baseline tariff on nearly all Japanese imports, down from the initial 27.5% rate.

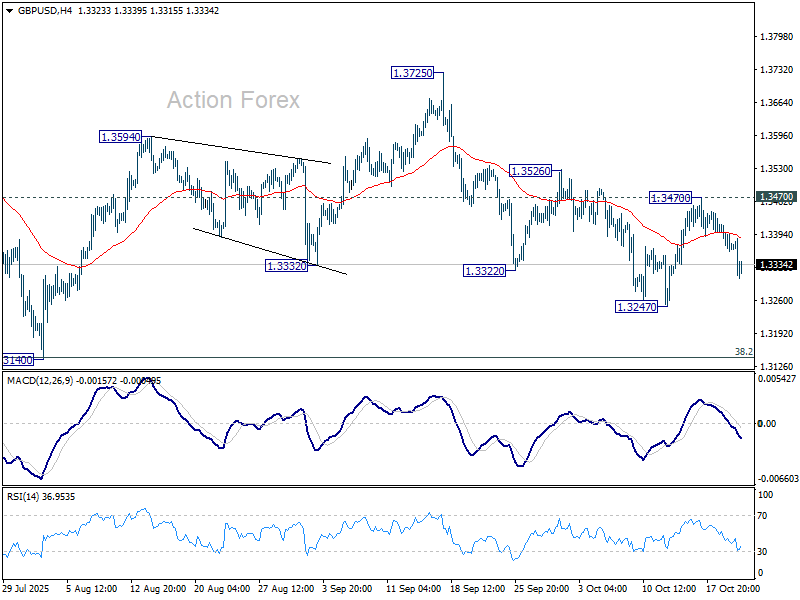

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3346; (P) 1.3383; (R1) 1.3404; More…

GBP/USD dips notably today but stays above 1.3247 support. Fall from 1.3725 could extend lower, and break of 1.3247 will target 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected there to contain downside to complete the corrective pattern from 1.3787. On the upside, break of 1.3170 resistance will turn bias back to the upside for 1.3526 resistance. Firm break there will target 1.3725/87 resistance zone.

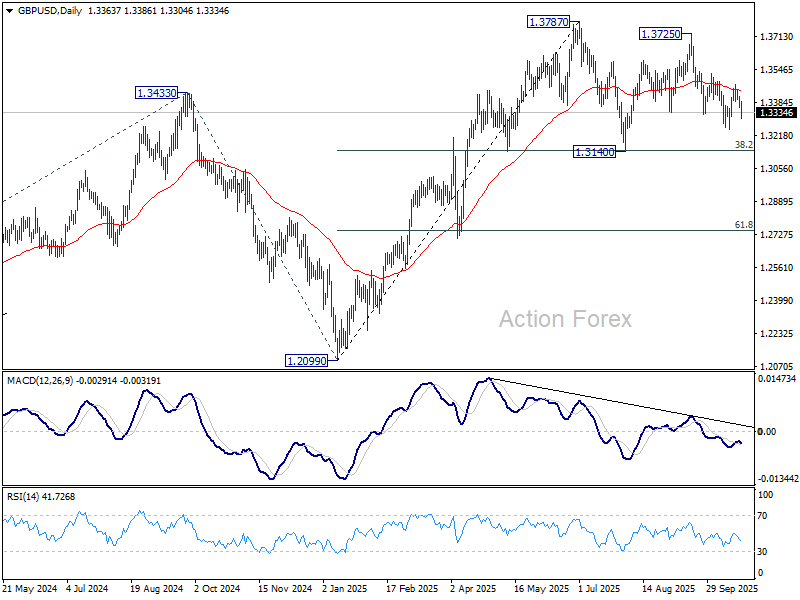

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more