Pound Pressured By Soft Jobs Data, Franc Climbs On Tariff Relief Hopes

Sterling fell mildly across the board today as weak UK labor market data reinforced expectations that the BoE would deliver a rate cut in December. Yet, as seen in comments from MPC member Megan Greene, not all policymakers are convinced, leaving December’s decision finely balanced.

The data comes just days after a closely divided 5–4 MPC vote to hold rates, with Governor Andrew Bailey’s deciding vote narrowly favoring caution. The combination of rising joblessness and easing wage momentum supports the view that inflationary pressures are subsiding faster than expected.

Traders now see the probability of a 25bps cut in December rising sharply, contingent on next week’s Autumn Budget confirming the deflationary tilt hinted at by Chancellor Rachel Reeves. Looking ahead, money markets are now pricing in 65bps of BoE rate cuts by end-2026, up from 55bps yesterday, suggesting investors expect a more extended easing cycle.

While Sterling weakened, Swiss Franc surged on reports that Washington and Bern are close to a deal to cut U.S. tariffs on Swiss exports. Multiple outlets, including Bloomberg, said the current 39% duty could be reduced to 15%, matching the rate applied to European Union goods. A Swiss economy ministry spokesperson declined to confirm details but said Economy Minister Guy Parmelin remains “in regular contact” with U.S. officials, including USTR Jamieson Greer.

In today’s currency rankings so far, Swiss Franc stands as the strongest performer, followed by Euro and New Zealand Dollar. At the other end of the spectrum, Sterling leads the laggards, trailed by Aussie and Loonie. Dollar and Kiwi sit in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.77%. DAX is up 0.08%. CAC is up 0.73%. UK 10-year yield is down -0.085 at 4.383. Germany 10-year yield is down -0.006 at 2.663. Earlier in Asia, Nikkei fell -014%. Hong Kong HSI rose 0.18%. China Shanghai SSE fell -0.39%. Singapore Strait Times rose 1.20%. Japan 10-year JGB yield fell -0.087 to 1.696.

BoE’s Greene wtays hawkish despite rise in UK unemployment

BoC policymaker Megan Greene pushed back against expectations for a December rate cut, saying this morning’s weaker labor data is not enough to change her stance.

Speaking at a conference in London, Greene—one of the five MPC members who voted to hold rates steady last week—argued that the labor market has likely moved past its sharpest adjustment phase.

She pointed to “higher-frequency data” showing early stabilization, adding that many companies still plan to lift wages substantially. Greene said it is “possible that the worst is behind us,” although she acknowledged that the latest 5.0% unemployment rate—the highest in four years—was “not great.”

UK unemployment rate jumps to four year high, wages growth slow

UK labor market data released today showed further cooling, reinforcing expectations that the BoC would deliver another rate cut in December.

In October, Payrolled employment fell -0.1% mom, or -32k, while claimant count rose 29k, exceeding expectations of a 20.3k rise. Wage pressures also eased significantly. Median monthly pay grew just 3.1% yoy, sharply down from 5.9% previously and marking the weakest pace since mid-2020.

In the three months to September, unemployment rate climbed from 4.8% to 5.0%, the highest in four years. Average earnings growth slowed from 5.0% yoy to 4.8% including bonuses, and from 4.7% yoy to 4.6% excluding them. Both readings highlight that the pay cycle is losing momentum as inflation falls and labor slack builds.

German ZEW falls to 38.5, but Eurozone improves

Investor confidence in Germany softened slightly in November, signaling continued caution about Europe’s largest economy despite signs of broader regional improvement. German ZEW Economic Sentiment Index slipped to 38.5 from 39.3, missing expectations of 42.5. Current Situation Index improved modestly from -80.0 to -78.7.

In contrast, Eurozone-wide ZEW Sentiment Index rose to 25.0 from 22.7, beating forecasts of 23.5. Current Situation Index improved to -27.3, up 4.5 points.

ZEW President Achim Wambach noted that while sentiment remains broadly stable, investors’ trust in Germany’s economic policy response has weakened. He said the government’s investment initiatives may deliver short-term stimulus, but “structural problems continue to exist”.

Australia Westpac consumer confidence surges to 103.8, marking end of prolonged pessimism

Australian consumer confidence jumped sharply in November, marking a clear break from years of pessimism. The Westpac Consumer Sentiment Index rose 12.8% mom to 103.8, its first positive reading since early 2022 and the highest in seven years, excluding the brief COVID-era spike. The surge was underpinned by a sharp improvement in views on the economy, with the 12-month and five-year outlook sub-indexes rising 16.6% and 15.3%, respectively—both now well above long-run averages.

Westpac said the result “draws a clearer line” under the prolonged period of consumer strain caused by high inflation, elevated interest rates, and rising tax burdens. The rebound likely reflects stronger domestic momentum, particularly in housing and consumer demand, as well as a more stable external backdrop. The recent de-escalation in U.S.–China trade tensions and a new Australia–U.S. deal on critical minerals have also buoyed sentiment.

The real surprise, according to Westpac, is how decisively these positive forces outweighed lingering worries about inflation and future rate settings. The data suggest households are regaining confidence in Australia’s recovery prospects even as monetary policy remains tight—offering a fresh signal that consumer resilience could help underpin growth heading into 2026.

RBNZ survey points to one more cut, then extended hold through 2026

New Zealand’s inflation expectations remain well anchored, while rate projections signal the RBNZ’s easing cycle is nearing its end.

The latest RBNZ Survey of Expectations showed the mean one-year-ahead inflation expectation edging up slightly to 2.39% from 2.37%. Two-year expectation stayed unchanged at 2.28%. Longer-term views were broadly steady, with the five-year expectation easing to 2.22% and the ten-year measure rising modestly to 2.18%—all consistent with the Bank’s 1–3% target midpoint.

Respondents now see the Official Cash Rate, currently at 2.50% following October’s 50bps cut, at 2.25% by year-end, implying just one more 25bps reduction before policy stabilizes. The one-year-ahead OCR expectation fell sharply to 2.31% from 2.86%, indicating that market participants expect the RBNZ to remain on hold through much of 2026 as inflation trends near target and growth moderates.

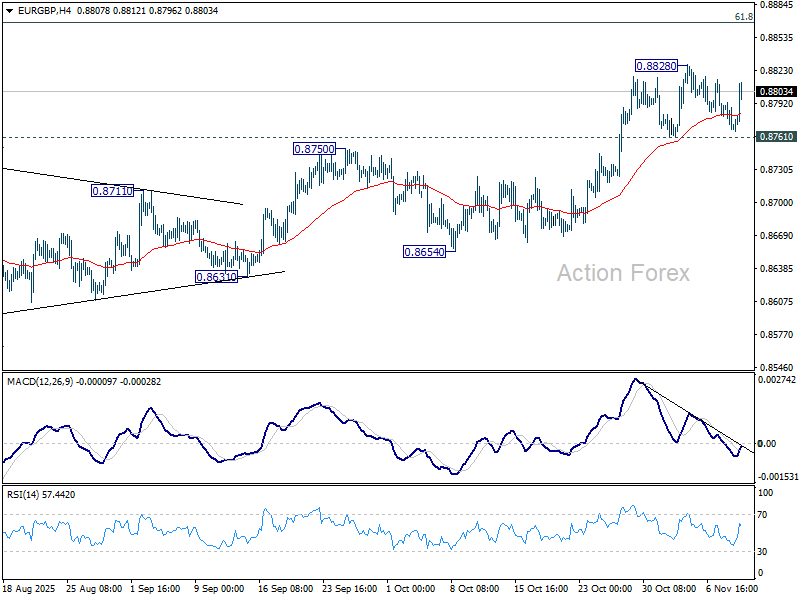

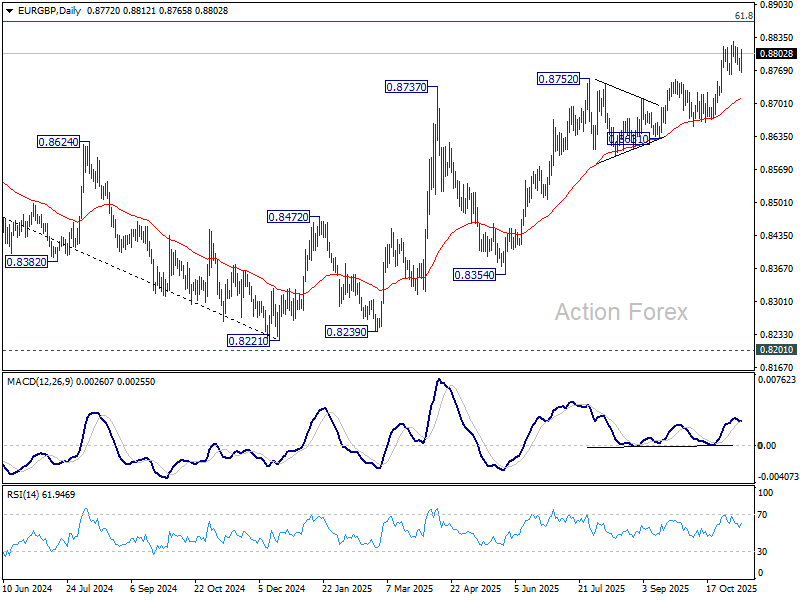

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8762; (P) 0.8779; (R1) 0.8788; More…

EUR/GBP rebounded notably today but stays in range below 0.8828. Intraday bias remains neutral and more consolidations could be seen. Further rally is expected as long as 0.8761 support holds. On the upside, break of 0.8828 will resume the whole rise from 0.8221 and target 0.8867 fibonacci level. Firm break there will carry larger bullish implications. However, considering bearish divergence condition in 4H MACD, decisive break of 0.8761 will confirm short term topping, and bring deeper fall to 55 D EMA (now at 0.8710).

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Firm break of 0.8654 support will be the first sign that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high).

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more