Markets Stay Risk-Off But Dollar Loses Safe-Haven Edge

Markets remain firmly in risk-off mode, with US equities extending their selloff overnight and Asian markets staying under pressure. The backdrop continues to be dominated by conflicts in the Middle East, with energy markets at the center of the shock. Yet, despite the deterioration in sentiment, a notable divergence has emerged in currency markets.

There was a brief moment of relief after US President Donald Trump urged Israel not to strike Iran’s energy infrastructure, raising hopes for de-escalation. However, that optimism quickly faded as Israel launched a new wave of attacks, reinforcing the view that the conflict is now in a more entrenched and dangerous phase.

A joint statement from major countries including the UK, France, Germany, Italy, the Netherlands, Japan, and Canada signaled readiness to ensure safe passage through the Strait of Hormuz. While this move aims to stabilize markets, it is largely seen as defensive rather than transformative.

In practice, the logistical challenges of securing shipping routes through an active conflict zone remain significant. Insurance premiums for tankers are already surging, effectively acting as a “shadow tax” on global trade and growth. This embedded cost pressure is likely to persist even without further escalation.

Oil prices reflect this reality. Although Brent crude has pulled back from its spike to 119 yesterday, it remains firmly elevated above 105, sustaining a powerful inflationary impulse. This keeps markets focused not just on geopolitical risks, but also on the second-round effects on global inflation and policy.

Against this backdrop, Dollar’s inability to strengthen stands out. Traditionally, risk aversion would support the greenback, but that relationship appears to be breaking down. Instead, Dollar is being weighed down by shifting expectations around monetary policy.

The Federal Reserve’s latest projections still point to one rate cut this year, even if conviction has softened. In contrast, markets are increasingly pricing in tightening from other major central banks, particularly in Europe, where the inflation impact of higher energy prices is more pronounced.

For the Bank of England, markets are now pricing roughly a 70% chance of a rate hike by year-end, with some expectations of two increases. Meanwhile, ECB rate expectations have shifted significantly, with one to two hikes now priced for 2026. This divergence is reshaping currency dynamics.

The rationale is clear: European economies are more directly exposed to the energy shock, increasing the likelihood of persistent inflation pressures. As a result, central banks in the region may be forced into a more hawkish stance compared to the Fed, despite weaker growth conditions.

In currency markets, for the week so far, Loonie is the weakest performer, followed by Dollar and Swiss Franc. Kiwi leads gains, followed by Aussie and Sterling, while Euro and Yen sit in the middle.

In Asia, Japan is on holiday. Hong Kong HSI is down -0.61%. China Shanghai SSE is down -0.48%. Singapore Strait Times is down -0.39%. Overnight, DOW fell -0.44%. S&P 500 fell -0.27%. NASDAQ fell -0.28%. 10-year yield rose 0.022 to 4.281.

Gold stabilizes at 4,500 as liquidation exhausts, 4,000 remains target

Gold steadies near 4500 after a liquidity-driven selloff triggered margin calls and ETF outflows. With forced selling fading, consolidation may follow, but broader downside still points toward 4000. Read more.

NZ exports hit by soft China and Japan demand

NZ’s trade balance slipped into deficit as exports to China and Japan declined while imports surged. Soft Asian demand and rising external imbalance could weigh further on NZD. Read more.

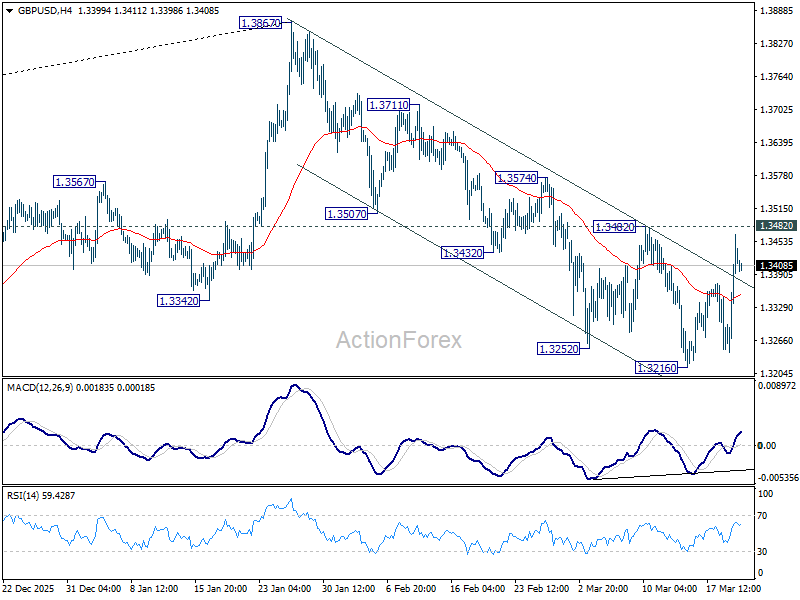

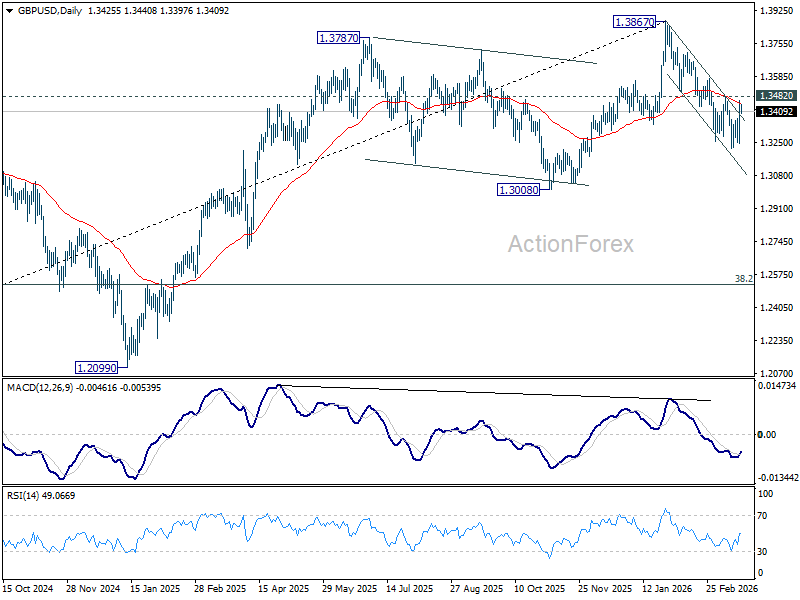

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3295; (P) 1.3382; (R1) 1.3517; More…

GBP/USD rebounded strongly but stays below 1.3482 resistance. Intraday bias remains neutral first. Further decline is still in favor. Below 1.3216 will resume the fall from 1.3867 to 1.3008 structural support. However, decisive break of 1.3482 will argue that the fall from 1.3867 has completed, and turn bias back to the upside for retesting this high.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place from 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or under further development.

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more

Gyrostat May Market Outlook: When The Cost Of Protection Falls - Signals For Portfolio Positioning

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. It... Read more