Euro Under Fire Again As Frances Macron Hunts For Sixth Prime Minister In Two Years

Euro came under renewed selling pressure today, particularly in crosses, as investors reacted nervously to deepening political uncertainty in France. President Emmanuel Macron’s search for a new prime minister dominated headlines. His office confirmed that he would appoint a replacement “within 48 hours,” after outgoing Prime Minister Sebastien Lecornu spent two days in futile talks to resolve what has become France’s worst political crisis in decades. Macron’s next pick would be his sixth prime minister in less than two years, highlighting the instability that has plagued his administration.

The abrupt resignation of Lecornu—after just 27 days in office—surprised markets, which had largely assumed that the next step in France’s political drama would be a snap parliamentary election. Instead, the prospect of yet another reshuffle with no clear end to the legislative gridlock has rekindled investor anxiety about France’s fiscal direction and reform capacity.

Meanwhile the ECB’s September meeting accounts, released overnight, reaffirmed that the central bank is firmly on hold and in no rush to adjust interest rates. Importantly, the minutes also made clear that “moderate fluctuations of inflation around the target” should not prompt a policy adjustment — effectively confirming that the ECB sees little reason to move in the near term. The reiteration of patience was already priced in by markets, and provided no meaningful support to the Euro, which continues to trade on political headlines rather than monetary expectations.

Elsewhere, currency market performance this week remains broadly consistent. Yen continues to lead losses, pressured by risk-on sentiment and doubts over further BoJ tightening. The Euro ranks second worst, with the Kiwi close behind following the RBNZ’s dovish 50bps cut. In contrast, Aussie and Loonie remain top performers. Dollar holds firm in the upper tier. Sterling and the Swiss Franc are trading mixed in the middle.

In Europe, at the time of writing, FTSE is down -0.18%. DAX is up 0.53%. CAC is up 0.50%. UK 10-year yield is up 0.016 at 4.737. Germany 10-year yield is up 0.01 at 2.692. Earlier in Asia, Nikkei rose 1.77%. Hong Kong HSI fell -0.29%. China Shanghai SSE rose 1.32%. Singapore Strait Times fell -0.35%. Japan 10-year JGB yield fell -0.007 to 1.697.

ECB minutes show comfort with current policy, high value in waiting

Minutes of the ECB’s September 10–11 meeting revealed broad agreement among policymakers that there was “no immediate pressure” to adjust interest rates. Officials noted that recent data confirmed inflation is “in a good place” while the domestic economy remains “resilient,” risks to growth now seen as “more balanced.”

The ECB recognized that the environment remains more uncertain than usual. The situation was likely to “change materially at some point” but the timing and direction were still unclear. The minutes noted the “high option value” of waiting for more evidence before altering policy, given two-sided inflation risks and the potential for unexpected shocks. The current rate level was described as “sufficiently robust” to manage a range of outcomes.

It also stressed that monetary policy should not be recalibrated for “moderate fluctuations of inflation around the target,” but only when a “significant deviation” is expected over the medium term. Though, while large, sustained deviations from target—like those seen over the past decade—are rare, monetary policy will still be ready to deliver “cyclical responses” to demand shocks.

BoE’s Mann: Inflation scarring still weighing on consumption, justifies policy restraint for longer

BoE policymaker Catherine Mann cautioned in a speech today that monetary policy must remain restrictive despite signs of weak consumption, arguing that high inflation has scarred UK consumers and continues to suppress spending.

“If the consumption gap was my only concern, reducing the restrictiveness of monetary policy would be appropriate,” she said. “However, in light of elevated inflation and expectations, maintaining restrictiveness for longer would be appropriate.”

Mann said the Bank’s analysis points to two drivers of the consumption gap: first, inflation and consumer scarring, and second, the channels through which monetary policy affects consumption.

The former, she explained, is a legacy of the rapid price surge that eroded purchasing power and altered household behavior. “High inflation itself is behind income uncertainty and weak consumption growth,” she said. “Monetary policy needs to continue to focus on reducing inflation” so households can return to a sustainable spending pattern.

For the second, she emphasized that higher rates have already exerted a material drag on demand, and the tightening effect is already waning. “Monetary policy has indeed loosened,” Mann said, adding that its impact on consumption has peaked.

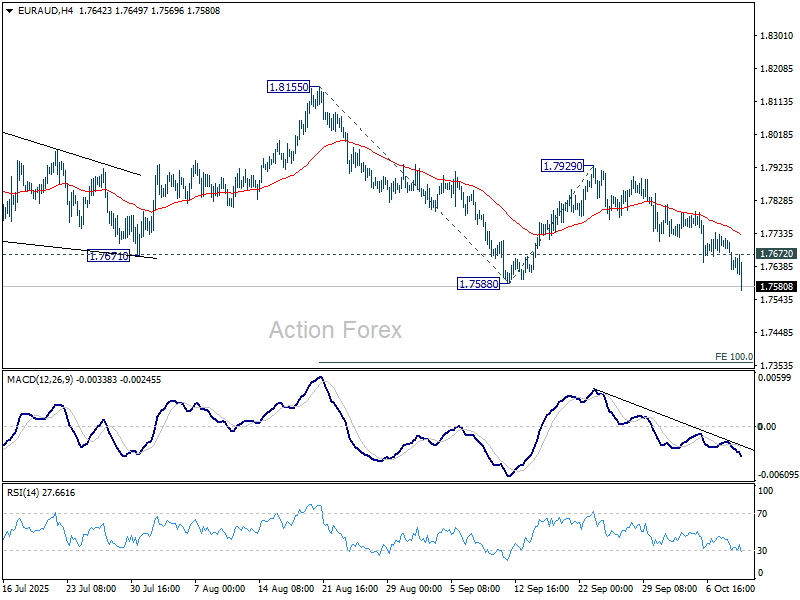

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.7612; (P) 1.7667; (R1) 1.7703; More…

EUR/AUD’s break of 1.7588 support confirms resumption of the fall from 1.8155. Such decline is seen as the third leg of the corrective pattern from 1.8554 high. Intraday bias is back on the downside for 100% projection of 1.8155 to 1.7588 from 1.7929 at 1.7362. On the upside, above 1.7672 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more