Dollar Soars On Strong US Data, 10-Yr Yield Jumps Toward 4.2%

Dollar rallied broadly at the New York open after a powerful run of data, with Treasury yields surging as investors trimmed Fed cut bets. The 10-year note climbed toward 4.2%, while stock futures dipped modestly, reflecting the possibility that stronger growth could keep policy tighter for longer.

A major catalyst came from the upward revision of Q2 GDP growth from 3.3% to 3.8% annualized, a strong signal that economic momentum held firm despite tariff escalation concerns earlier in the summer. That’s a clear sign that tariff risks have not derailed activity. The data also confirmed that the US economy carried far more momentum into the second half of the year than many expected.

Labor market signals added to the strength, with jobless claims falling back to their July lows. Durable goods orders also surprised with a broad expansion, defying forecasts of contraction and reinforcing the message of resilient investment demand.

Taken together, the reports are forcing markets to question whether the Fed needs to deliver as much easing as priced. Odds of two cuts this year to a 3.50–3.75% range have slipped below 70%, down from over 80% just last week, highlighting a subtle but important shift in expectations.

The Swiss Franc, by contrast, was on the defensive after the SNB left rates at 0.00% in a widely anticipated hold. Chair Martin Schlegel repeated that the bar for reintroducing negative rates remains high, though he stressed the central bank is ready to act if necessary. His cautious reassurance did little to support the Franc.

Overall, Dollar led performance on the day, with Loonie and Yen behind. Swiss Franc fell to the bottom of the board, with Sterling and Euro also under pressure. Commodity currencies traded mixed. North American currencies are in control, while European majors lag.

In Europe, at the time of writing, FTSE is down -0.47%. DAX is down -1.09%. CAC is down -0.85%. UK 10-year yield is up 0.068 at 4.744. Germany 10-year yield is up 0.027 at 2.781. Earlier in Asia, Nikkei rose 0.27%. Hong Kong HSI fell -0.13%. China Shanghai SSE fell -0.01%. Singapore Strait Times fell -0.39%. Japan 10-year JGB yield rose 0.01 to 1.649.

US durable goods surge 2.9% mom in August, crushing expectations

US durable goods orders surged 2.9% mom to USD 312.1B in August, far stronger than the expected -0.5% mom contraction. Excluding transportation, orders still rose 0.4% mom to USD 201.9B, beating forecasts for a small decline of -0.1% mom. Ex-defense orders climbed 1.9% mom to USD 290.7B.

The headline gain was led by a 7.9% mom jump in transportation equipment to USD 110.2B, but the breadth of gains pointed to firm underlying demand.

US initial jobless claims fall to 218k, vs exp 240k

US initial jobless claims fell -14k to 218k in the week ending September 19, much better than expectation of 240k. Four-week moving average of initial claims fell -3k to 238k.

Continuing claims fell -2k to 1926k in the week ending September 13. Four-week moving average of continuing claims fell -4.5k to 1930.

SNB holds at 0.00%, inflation outlook unchanged

The SNB opted to keep its policy rate at 0.00% in September, delivering the first pause since its rate-cutting cycle began in December 2023. The move matched expectations and reflects a balance between subdued inflation and a weaker growth backdrop.

The central bank noted that inflation has edged up slightly, from -0.1% in May to 0.2% in August, driven mainly by tourism and higher prices for imported goods. Still, it stressed that inflationary pressures remain broadly unchanged since June, with the conditional forecast holding within its definition of price stability across the “entire forecast horizon”. Annual inflation is projected at 0.2% in 2025, 0.5% in 2026, and 0.7% in 2027, assuming interest rates stay at 0%.

However, the SNB warned that the economic outlook has worsened due to “significantly higher US tariffs.” It said the measures are expected to weigh on exports and investment, with the machinery and watchmaking sectors particularly exposed. As a result, the SNB maintained its GDP forecast of 1–1.5% growth for 2025 but down graded expectations for 2026 to just under 1%.

BoJ minutes point to year-end hike possibility

The BoJ’s July meeting minutes revealed a growing debate among policymakers over the need to raise rates toward neutral levels. One member argued that with prices elevated and the output gap near zero, it was appropriate for the BoJ to “return the policy rate to its neutral level where possible.”

Another member warned against being “overly cautious,” saying the central bank should not miss the opportunity to hike rates, particularly as stock markets have reacted positively to the recent U.S.–Japan trade deal. Several others echoed this view, suggesting that another hike could be feasible before year-end if tariffs cause only limited drag on the economy.

Meanwhile, policymakers were divided on inflation. While one saw the overshoot as temporary and food-related, others highlighted the risk that persistent food price increases could entrench higher inflation expectations.

The debate has since intensified, as seen in September’s meeting when two members dissented in favor of lifting rates to 0.75%. The growing hawkish faction raises the prospect that the BoJ could still deliver another rate hike in the coming months, particularly if growth and inflation prove resilient.

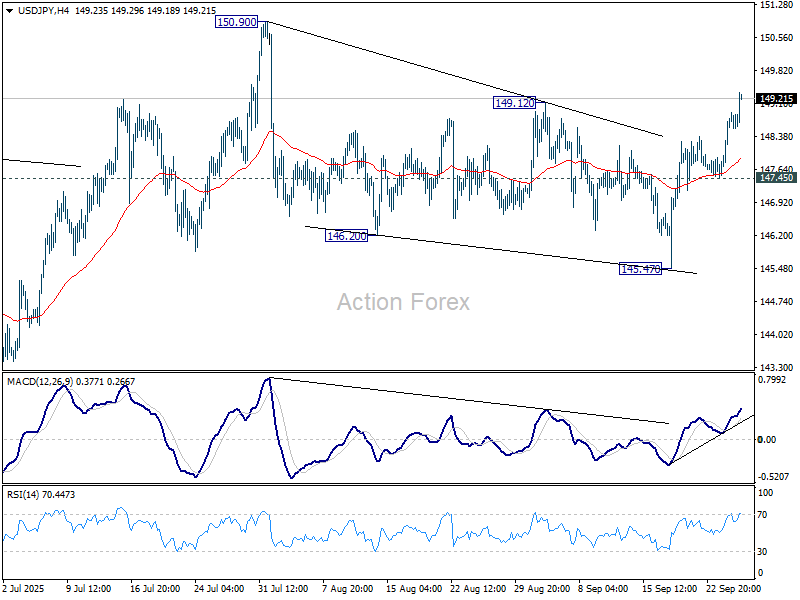

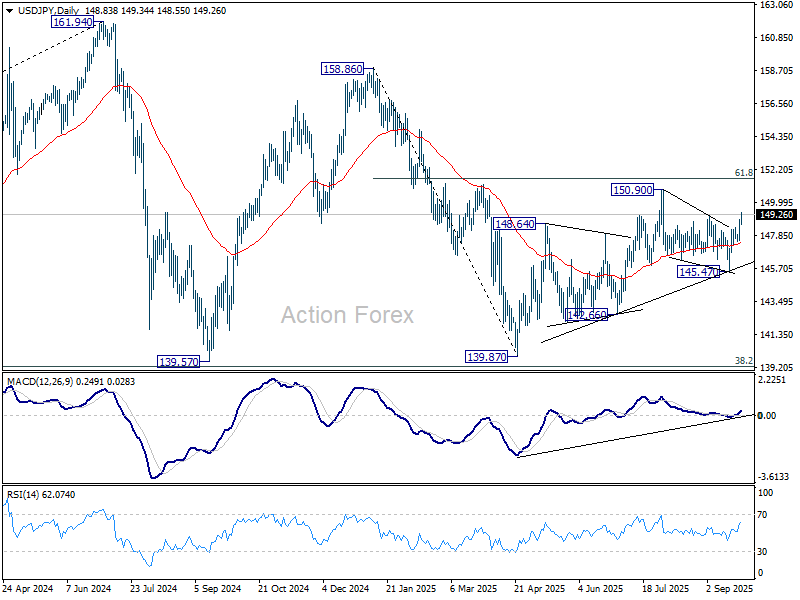

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.98; (P) 148.45; (R1) 149.38; More…

USD/JPY’s rise from 145.57 extends higher today. The break of 149.12 resistance should confirm that correction from 150.90 has completed at 145.47. Further rally should be seen to retest 150.90. Break there will resume whole rise from 139.87. For now, risk will stay on the upside as long as 147.45 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more