Dollar Dominates As Strong Data Cuts Odds Of Aggressive Fed Easing

Currency markets closed last week with a shift in tone, as traders suddenly found themselves recalibrating on Fed’s easing path once again. The resilience of the US economy surprised many. Growth, hiring, and investment all showed more strength than anticipated, fueling doubts about whether policymakers truly need to accelerate the pace of cuts. The question now is not whether the Fed will ease in October, but how much conviction remains for December and beyond.

That uncertainty helped knock the wind out of equity markets. After a record-breaking run, stocks lost momentum as investors considered the possibility of a shallower easing path. Treasury yields, in turn, extended their rebound, while Dollar surged, benefiting from both yield support and some safe-haven demand.

Not all currencies fared equally in this recalibration. Swiss Franc and Euro managed to post gains, albeit much more modestly than Dollar. Both benefited from steady central bank stances. Their strength, however, was as much about avoiding weakness as it was about genuine optimism.

At the other end of the spectrum, commodity currencies struggled. Kiwi tumbled further on continuous expectations of a jumbo RBNZ cut and leadership transition at the central bank. Loonie slid despite GDP rebound, as underlying economic weakness left markets convinced more BoC easing is on the horizon. Yen also weakened, pressured by yield differentials.

Aussie managed to sit in the middle, alongside Sterling. Support came from upside inflation surprise in Australia that pared back RBA cut bets, though conviction will ultimately hinge on quarterly CPI later in October. Sterling, meanwhile, drifted, caught between softer growth data and speculation over how hawkish the BoE will turn.

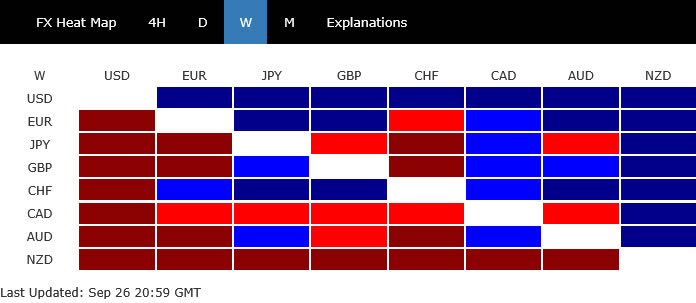

The performance scoreboard tells the story clearly: Dollar, Franc, and Euro at the top; Kiwi, Loonie, and Yen anchored at the bottom; and Aussie and Sterling caught in the middle.

US Data Resilience Tempers Fed Cut Bets Beyond October

Expectations for Fed easing shifted notably last week as a string of stronger-than-expected US data challenged the case for aggressive rate cuts. The upgraded Q2 GDP print, resilient September PMIs, firmer jobless claims, and robust durable goods orders underscored economic resilience despite tariff headwinds.

This recalibration left futures still pricing a near-certain October cut, but with far less conviction for December. The adjustment has rippled across markets: US stocks lost momentum from record highs, Treasury yields extended their rebound, and Dollar surged to finish the week as the strongest major currency.

The US economy continues to defy expectations. The final estimate for Q2 GDP was revised up sharply to 3.8% annualized, from 3.3% previously, showing that activity held firm despite tariff headwinds. Rather than slowing sharply, growth carried strong momentum into Q3.

PMI surveys for September reinforced that resilience. At 52.0 for manufacturing and 53.9 for services, both sectors remain comfortably in growth territory. The composite data suggest output is expanding at a 2.2% annualized pace this quarter, consistent with a gradual rather than abrupt cooling.

Employment signals have also steadied. Weekly jobless claims fell back below 220k, a level that implies hiring is not collapsing. The settlement of reciprocal tariffs in August may be encouraging firms to resume normal recruitment, easing fears of sudden weakness in the labor market.

Meanwhile, durable goods orders surged unexpectedly. Headline orders rose 2.9% in August, led by a near-8% jump in transportation equipment, while core measures also surprised to the upside. The numbers suggested that businesses still have confidence to invest in capital goods, even amid global uncertainty.

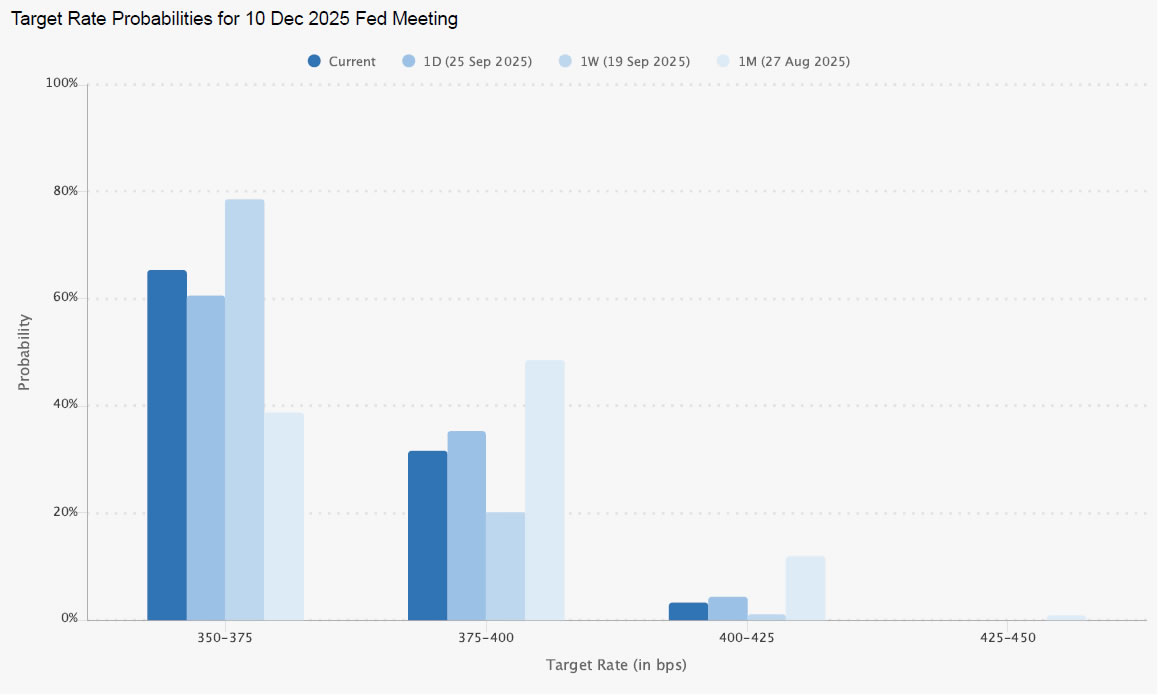

These strong data have shifted market views on the Fed. Futures continue to price a high probability — 87.7% — of another cut in October, but bets on a December move have dropped to 65.4%, well below nearly 80% seen a week ago. The market message: another “insurance” cut is likely, but an extended easing cycle is less certain.

Fed officials have largely echoed that cautious stance. With the notable exception of Governor Stephen Miran, who continues to argue for deeper cuts, most policymakers emphasize that policy decisions must remain tied to the flow of data. That position has been reinforced by evidence of economic resilience.

Still, risks remain. Fed Chair Powell acknowledged that job creation is slipping below the “breakeven” pace needed to keep unemployment steady. If hiring deteriorates further, the Fed may still be forced to accelerate easing despite the strong GDP backdrop.

The September non-farm payrolls report will be pivotal. A strong outcome could validate the case for a slower easing pace, but a weak print would push the Fed toward more “risk management” reductions. Until then, expectations remain fluid, with markets balancing solid growth against fragile employment signals.

Equities Lose Momentum as Fed Bets Reprice, But Uptrend intact

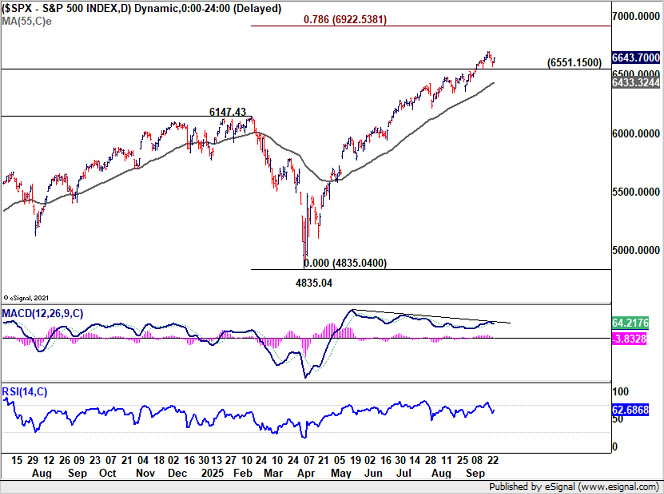

US equities lost some steam last week as the stronger economic backdrop forced investors to reassess the extent of Fed easing ahead. S&P 500 retreated from record highs, and the immediate focus now falls on whether the index can hold above key short-term support at 6551.15.

Decisive break below this level would confirm near term topping and open the way for a deeper correction toward the 55 Day EMA (now at 6433.32). Even so, the broader uptrend remains intact, and strong buying interest should be expected on dips, with the EMA zone offering a cushion.

Conversely, strong rebound from current levels would quickly shift sentiment back to the upside. S&P 500 could then resume its rally toward 78.6% projection of 3491.58 to 6147.43 from 4835.04 at 6922.53, extending the impressive run that has defined much of 2025.

The trajectory will hinge heavily on the next round of labor and inflation data, which could either validate or challenge the market’s current positioning.

10-Year Yield Extends Rebound But 4.3 Should Cap

US Treasuries sold off further last week, with 10-year yield extending its corrective rebound from the 3.992 low to close at 4.187. The move reflects shifting Fed expectations after the stronger run of economic data.

Technically, the yield is currently eyeing further rise to 55 D EMA (now at 4.215) and possibly above. But falling channel ceiling near 4.300 should provide strong resistance to limit upside, reinforcing the broader decline from 4.629 that remains intact.

On the downside, break back below 4.110 would suggest that the rebound has already run its course, and put the spotlight back on the 3.992 low.

Dollar Index Rebound to Continue as Short Term Bottom Formed

Dollar Index’s extended rebound and break of 55 D EMA (now at 98.05) should confirm short term bottoming at 96.21. Considering bullish convergence condition in D MACD, it’s possible that whole fall from 110.17 has completed too. Further rise is in now favor to as long as 97.22 support holds, to 100.25 resistance.

However, the zone between 38.2% retracement of 110.17 to 96.21 at 101.54 and 55 EMA (now at 101.10) would be a huge hurdle. It would requires either extended rise in yield through the falling channel, or extended correction in stocks, or both, to give Dollar Index the fuel to overcome this resistance zone.

Meanwhile, break of 97.22 support will dampen near term bullishness and bring retest of 96.21.

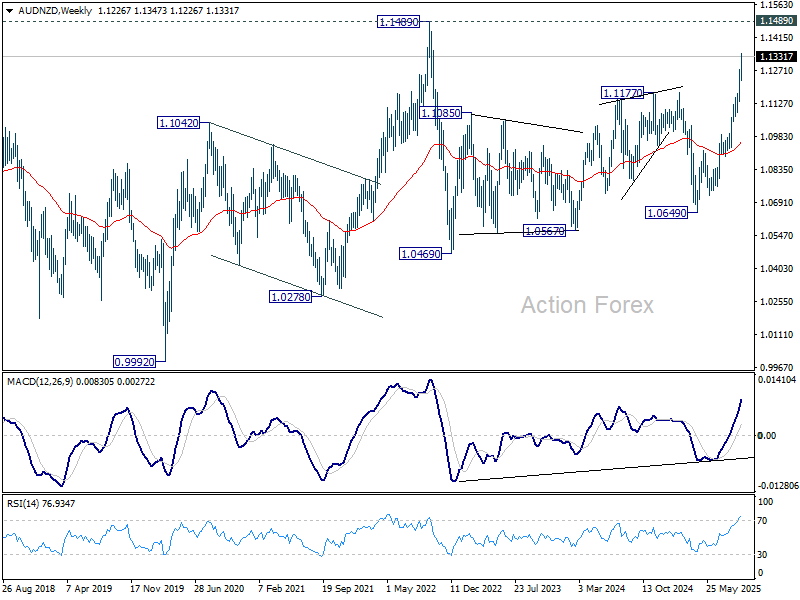

Kiwi and Loonie Struggle, Aussie Flaring Slightly Better

Commodity currencies struggled last week, with New Zealand Dollar leading losses as markets braced for a more aggressive easing path. Weak domestic data have already built the case for a 50bps RBNZ cut on October 8, and sentiment was further clouded by uncertainty around a leadership change at the central bank.

In a surprise announcement, Swedish economist Anna Breman was named the next Governor of the RBNZ, set to take office on December 1. Currently the First Deputy Governor at the Riksbank, Breman’s appointment was welcomed as bringing global experience, though it carries little weight for the imminent policy meetings. She may attend November’s gathering as an observer, but she will not hold voting power.

The more immediate implication lies in the departure of Governor Christian Hawkesby, who steps down at the end of November. Markets suspect that, given his exit, Hawkesby may be less inclined to forcefully shape consensus in the MPC. That could tilt the balance toward a bolder move in October, especially with the economy under strain. As a result, traders see rising odds that the RBNZ will opt for a half-point cut at the next meeting.

Canadian Dollar also underperformed, despite July GDP showing a 0.2% monthly rebound. It was the first growth in four months and offered some relief after a string of soft prints. But the optimism quickly faded as advance estimates suggested August GDP was flat, underscoring that any recovery is still fragile.

The composition of growth revealed familiar challenges. Goods-producing industries delivered the bulk of the gains, while retail trade pulled down the services side. Real estate and wholesale activity showed some resilience, but overall momentum remains tepid, and only just over half of all sectors reported expansion.

Against this backdrop, the BoC’s rate cut to 2.50% earlier this month looks more like a first step than a solution. Market chatter has turned to the likelihood of two more cuts before year-end, with October seen as a strong candidate for the next move. Weak business investment and ongoing trade frictions with the US amplify the need for policy support.

Unlike its Kiwi and Loonie peers, Australian Dollar found some support last week after inflation surprised on the upside. August’s monthly CPI accelerated to 3.0%, above consensus expectations and pushing headline inflation back to the top of the RBA’s 2–3% target band.

The stronger data prompted a sharp reaction in bonds, with three-year government yields jumping to the highest level since May. Money markets quickly pared back expectations for a November RBA cut, pricing the probability of easing below 40% compared with over 60% earlier in the week.

The RBA, however, is unlikely to alter its steady approach. Governor Michele Bullock has emphasized that the Bank needs to balance encouraging household spending with ensuring inflation stays anchored. That means the October 29 quarterly CPI will be decisive, with November’s policy decision still finely balanced.

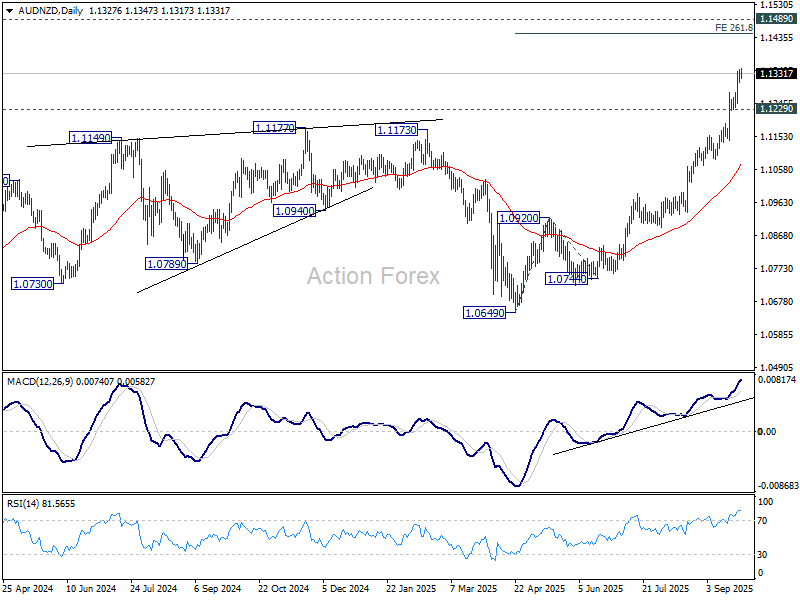

Technically, AUD/NZD remains in upside acceleration as seen in D MACD. Further rally is expected as long as 1.1229 support holds. Current rise from 1.0649 is in progress for 261.8% projection of 1.0694 to 1.0920 from 1.0744 at 1.1453. However, 1.1489 (2022 high) should cap upside, at least on first attempt.

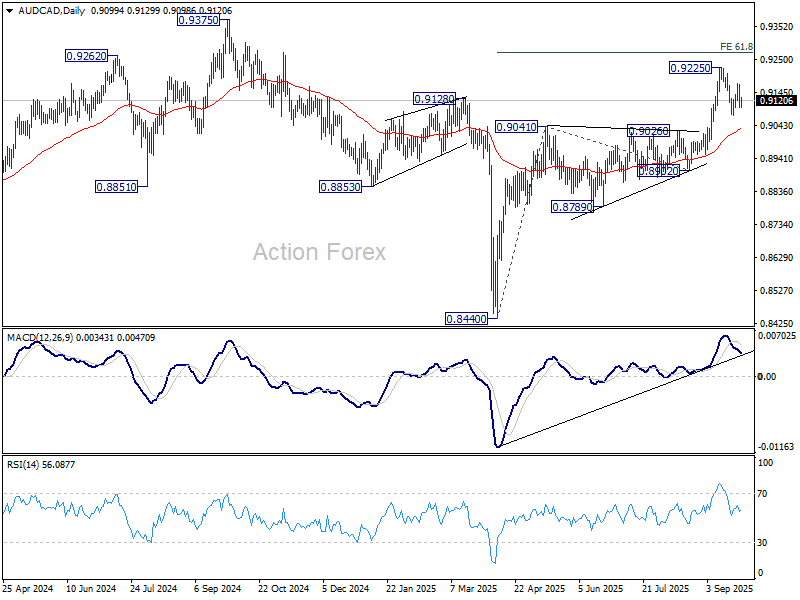

AUD/CAD‘s rally was, however, was disappointing as the intra-week rally attempt failed well below 0.9225 resistance. Nevertheless, near term outlook will stay bullish as long as 0.9041 resistance turned support holds. Rise from 0.8440 is expected to resume at a later stage to 61.8% projection of 0.8440 to 0.9041 from 0.8902 at 0.9273. Firm break there will pave the way to 0.9375 key structure resistance (2024 high) next.

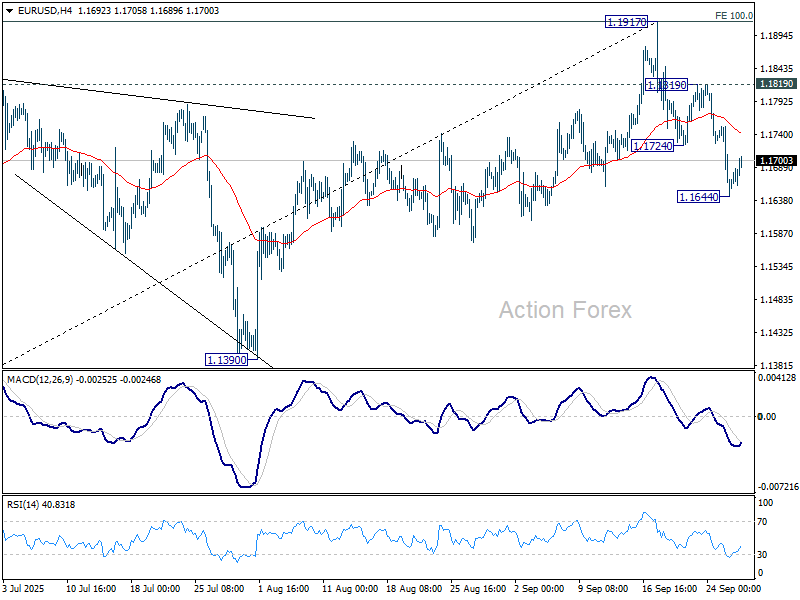

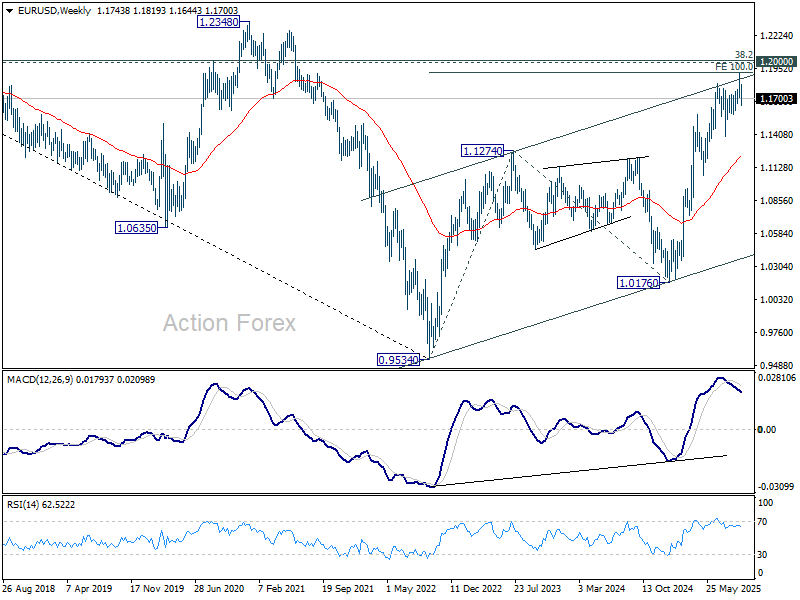

EUR/USD’s fall from 1.1917 short term top extended to 1.1644 last week, but recovered since again. Initial bias is turned neutral this week first. Further fall is expected as long as 1.1819 resistance holds. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA (now at 1.1668) will argue that 1.1917 was already a medium term top. Deeper fall should then be seen to 1.1390 support next.

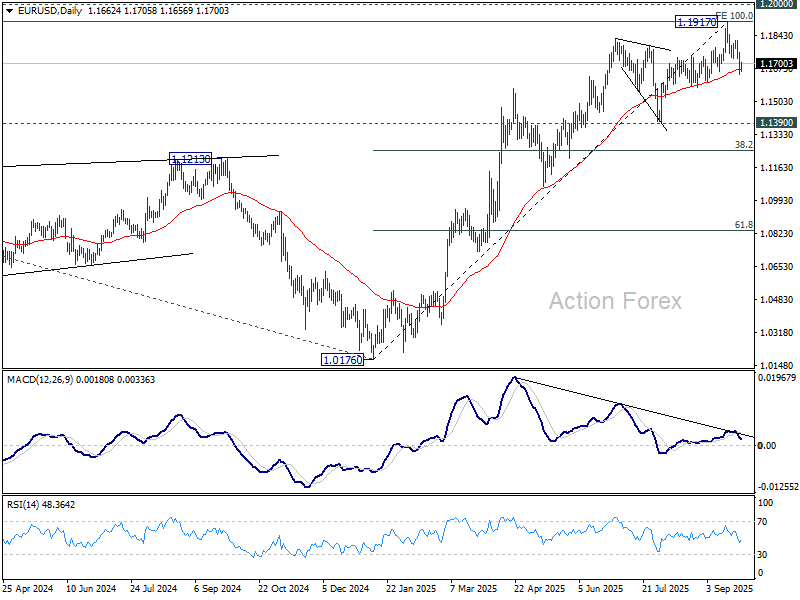

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1231).

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more