Calm Returns To Markets, Loonie Holds Firm, Yen Stays Weak

The forex market turned noticeably quieter in Asian session today, with traders taking a breather after the risk-on rally seen earlier in the week. Most major pairs and crosses remain confined within last week’s ranges, reflecting a more balanced tone as global sentiment stabilizes. Canadian Dollar continues to hold firm, extending support from Tuesday’s hotter-than-expected inflation data, while Aussie and Kiwi are also chalking up steady gains for the week.

By contrast, the Japanese Yen remains under heavy pressure, ranking as the weakest performer among the majors, followed by Euro and Sterling. Dollar and Swiss Franc are trading in the middle of the pack. The consolidation reflects a market still awaiting the next round of data to offer clearer trading cues, including Friday’s U.S. CPI

Nevertheless, the day’s spotlight turns to UK inflation figures first, expected to show headline CPI rising to 4% year-on-year in September — its highest since early 2024 and double the BoE’s 2% target. An upside surprise would bolster the case for the BoE to hold rates steady at its November 6 meeting, reinforcing arguments from policy hawks like Chief Economist Huw Pill.

Meanwhile, even a mild downside surprise may not be sufficient to sway the MPC toward an immediate rate cut. The committee remains deeply divided, and with the UK Budget due on November 26, most members are likely to delay major policy moves until the fiscal outlook becomes clearer.

Elsewhere, trade developments are drawing attention in South Asia. Indian media outlet Mint reported that the U.S. is preparing to substantially reduce tariffs on Indian exports as part of an emerging trade deal with New Delhi. According to the report, tariffs could be slashed to 15–16% from the current 50%, contingent on India agreeing to scale back its purchases of Russian oil. The move would mark a significant thaw in bilateral trade ties.

U.S. President Donald Trump confirmed on Tuesday that he had spoken with Prime Minister Narendra Modi, who assured Washington that India would reduce its intake of Russian crude. In a post on X the following morning, Modi described the call as “productive,” saying both countries would continue to stand “united against terrorism in all its forms,” though he avoided any direct reference to energy imports.

In Asia, at the time of writing, Nikkei is up 0.16%. Hong Kong HSI is down -1.12%. China Shanghai SSE is down -0.46%. Japan 10-year JGB yield is down -0.007 at 1.656. Overnight, DOW rose 0.47%. S&P 500 rose 0.00%. NASDAQ fell -0.16%. 10-year yield fell -0.023 to 3.963.

Japan’s exports rise for first time in five months, but U.S. demand still weak

Japan’s exports rose in September for the first time in five months, signaling tentative recovery in external demand even as shipments to the U.S. continued to contract sharply.

Exports climbed 4.2% yoy to JPY 9.41T, slightly below expectations of 4.6%. The rebound was driven largely by strength in Asia, where exports jumped 9.2%, including a 5.8% rise to China. In contrast, shipments to the U.S. fell -13.3%, with auto exports down -24.2%, extending months of weakness despite being a smaller drop than August’s 28.4% decline.

Imports also grew faster than expected, rising 3.3% yoy to JPY 9.65T, compared with forecasts of 0.6%. As a result, Japan posted a trade deficit of JPY 234.6B.

The data come just weeks after Washington finalized a new trade agreement with Tokyo, implementing a 15% baseline tariff on nearly all Japanese imports, down from the initial 27.5% rate.

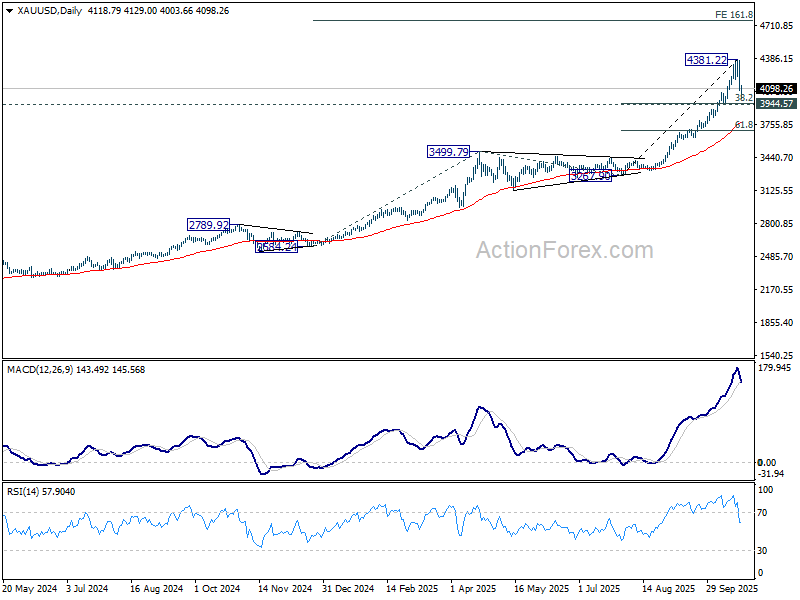

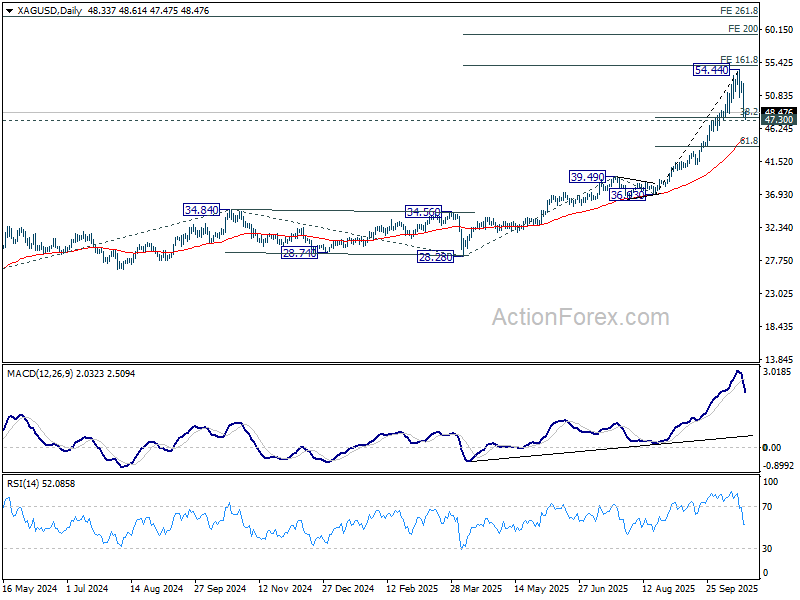

Gold, Silver in brief healthy consolidation as speculative heat cools

Gold and Silver saw heavy selling this week, pausing their record-setting advance as traders took profits and liquidity conditions improved. The decline has raised questions about whether the market is entering a deeper downturn, but technicals suggest the move is more of a healthy correction within a still-bullish backdrop.

Reports of increased Silver flows from the U.S. and China into London’s spot market added to the selling pressure, easing recent supply constraints that had intensified price momentum. The additional liquidity gave traders room to unwind speculative positions, accelerating the pullback but also helping to stabilize the market longer-term. This as part of a natural rebalancing after overbought conditions earlier in the month.

While the losses have been sharp, there is no clear structural threat to the broader uptrend. The latest pullback reflects profit-taking and short-term positioning adjustments rather than a breakdown in investor confidence. Demand for precious metals remains underpinned by global macro uncertainty, moderate inflation expectations, and central bank diversification away from U.S. assets.

Technically, Gold remains supported above 3,944.57 cluster, a level that separates sideway consolidation from deeper correction. As long as this level holds, consolidations from 4,381.22 should remain relatively brief. Sustained break above 4,381.22 would signal renewed strength, opening the path toward 161.8% projection of 2,584.24 to 3,499.79 from 3,267.90 at 4,749.25.

However, break of 3,944.57 would argue the latest rise leg from 3,267.90 has completed, and bring deeper correction to 55 D EMA (now at 3,781.78). Such a move would extend consolidation but not necessarily signal a full trend reversal.

Silver is showing a similar pattern. As long as 47.30 cluster holds, correction from 54.44 should stay shallow and short-lived. Another rise to 200% projection of 28.28 to 39.49 from 36.93 at 59.30 should be seen sooner rather than later.

However, a fall below 47.30, would trigger deeper pullback toward 55 D EMA (now at 44.76), before uptrend resumes.

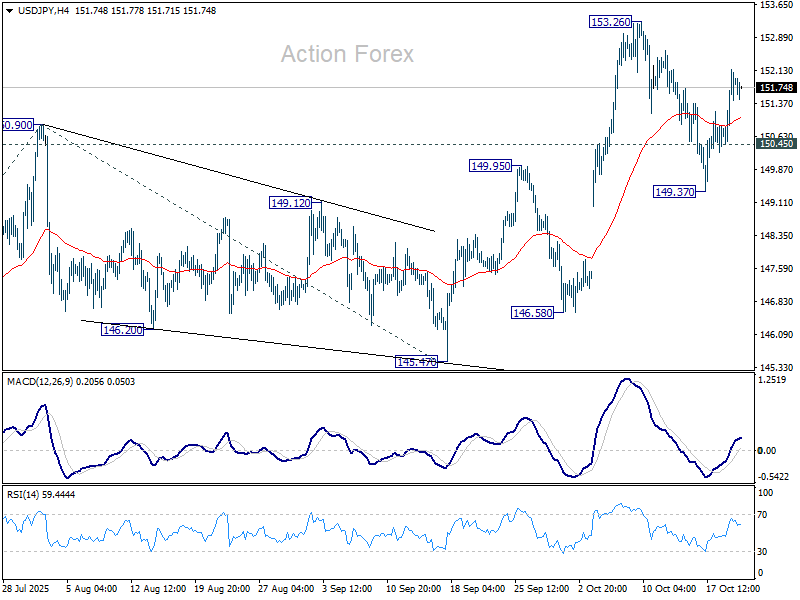

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.87; (P) 151.53; (R1) 152.58; More…

Intraday bias in USD/JPY remains on the upside for retesting 153.26. Break there will resume larger rally from 139.87 to 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there would prompt upside acceleration to 161.8% projection at 158.80. on the downside, below 150.45 minor support will dampen this bullish view and turn bias neutral again first.

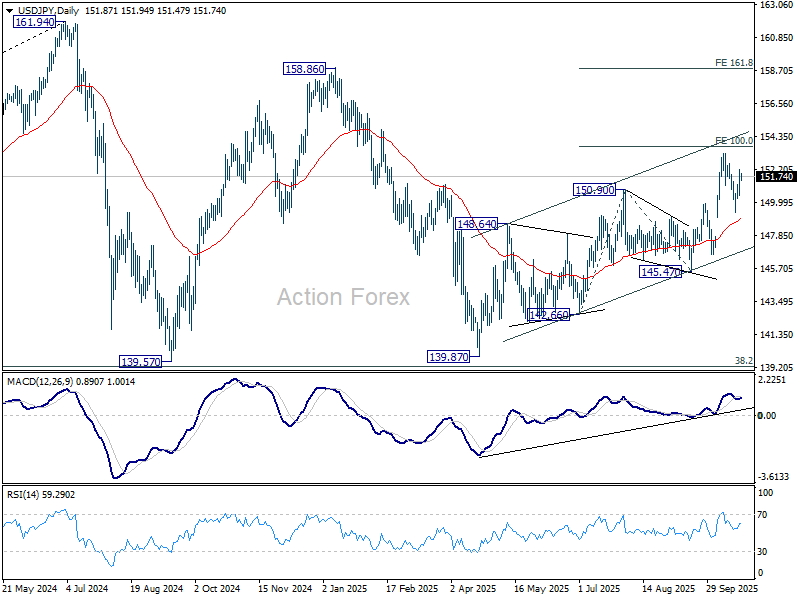

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more