BoJ Hawkish Lean Fails To Lift Yen, Franc Outperforms Ahead Of SNB

Trading remains subdued in the Asian session, with all major currency pairs locked inside yesterday’s ranges. Directional conviction remains elusive as traders look to fresh catalysts from both data and central bank events.

Minutes from the BoJ’s July meeting leaned hawkish, showing more board members are warming to the idea of returning to rate hikes. The tone was consistent with the September policy meeting, where two members dissented in favor of raising the policy rate to 0.75%. Yet the hawkish signals have done little to lift Yen. Instead, the currency is pressured by sustained risk-on sentiment across equities and stabilization in U.S. Treasury yields.

Meanwhile, Dollar is pausing after yesterday’s rally attempt, with investors awaiting fresh direction. Durable goods orders and jobless claims are due later in the day, providing an early test before Friday’s PCE inflation, the Fed’s preferred gauge. A slate of Fed officials are also scheduled to speak.

So far this week, the Franc leads gains as investors position for the SNB decision later today. Dollar ranks second and Aussie third with boost quickly fading. At the bottom, Loonie lags, followed by Kiwi and Yen. Euro and Sterling are trading in the middle.

In Asia, at the time of writing, Nikkei is up 0.23%. Hong Kong HSI is down -0.05%. China Shanghai SSE is down -0.13%. Singapore Strait Times is down -0.25%. Japan 10-year JGB yield is up 0.009 at 1.648. Overnight, DOW fell -0.37%. S&P 500 fell -0.28%. NASDAQ fell -0.33%. 10-year yield rose 0.027 to 4.147.

BoJ minutes point to year-end hike possibility

The BoJ’s July meeting minutes revealed a growing debate among policymakers over the need to raise rates toward neutral levels. One member argued that with prices elevated and the output gap near zero, it was appropriate for the BoJ to “return the policy rate to its neutral level where possible.”

Another member warned against being “overly cautious,” saying the central bank should not miss the opportunity to hike rates, particularly as stock markets have reacted positively to the recent U.S.–Japan trade deal. Several others echoed this view, suggesting that another hike could be feasible before year-end if tariffs cause only limited drag on the economy.

Meanwhile, policymakers were divided on inflation. While one saw the overshoot as temporary and food-related, others highlighted the risk that persistent food price increases could entrench higher inflation expectations.

The debate has since intensified, as seen in September’s meeting when two members dissented in favor of lifting rates to 0.75%. The growing hawkish faction raises the prospect that the BoJ could still deliver another rate hike in the coming months, particularly if growth and inflation prove resilient.

Fed’s Daly: Unsure on next cut, economy still needs policy bridling

San Francisco Fed President Mary Daly said she “fully supported” last week’s rate cut and expects more reductions will likely be needed. However, at an event overnight, she stressed that the timing for further cuts remains uncertain.”It’s hard to say”, she said.

Daly described the labor market as no longer solid but not weak either, calling it “sustainable.” She said she does not want to see further softening, noting that the Fed’s latest decision was effectively an “insurance” move to support jobs while inflation continues to moderate.

The economy, she added, still requires “monetary policy bridling, but not as much as we had.”

BoE’s Greene: Must prioritize inflation, cuts should be cautious

BoE MPC member Megan Greene said in a speech overnight that UK inflation remains an outlier among developed peers, with headline CPI running above target for over four years and rising again over the past year. She noted that disinflation has been concentrated in rate-sensitive sectors, suggesting “the bulk of disinflation may have already come through”, while labor market slack has emerged.

Greene argued that the data has the “hallmark of an adverse supply shock,” but said second-round wage effects are unlikely to pose major risks as the labor market loosens. She added that while risks from trade persist, they have eased somewhat, and GDP growth is expected to rebound without a sharp deterioration in jobs.

She stressed two lessons from recent supply shocks: when inflation persistence is uncertain, policymakers should prioritize inflation to prevent it from becoming entrenched, and that prices may respond faster than output when inflation is elevated.

Against that backdrop, she said “an appropriate response to the uncertainty and risks we are currently facing should involve a cautious approach to rate cuts going forward”, reinforcing her vote last week to keep Bank Rate at 4%.

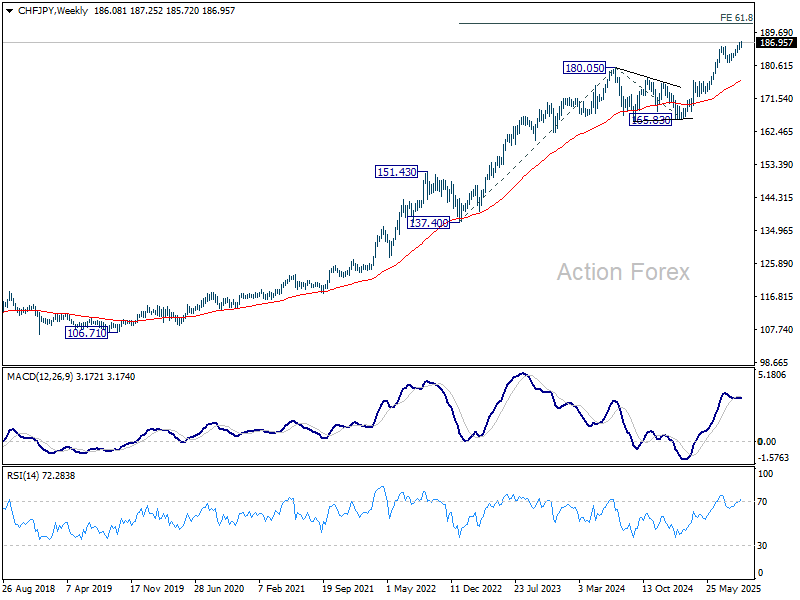

SNB set to hold at 0.00%, CHF/JPY rising toward 189.45

SNB’s policy decision is the main focus for today’s European session, with the central bank widely expected to keep rates unchanged at 0.00%. This would mark its first pause since December 2023, reflecting both steady inflation trends and a more stable external backdrop.

Inflation has stabilized slightly above 0% since June, easing fears of a return to deflation. With the ECB also settling at 2.00%, appreciation pressure on Swiss Franc has moderated, reducing the need for the SNB to counter imported disinflation. Additionally, Chairman Martin Schlegel has stressed that the bar for reintroducing negative rates is high, further supporting a steady stance.

Market consensus is strongly aligned with this view. A Reuters poll taken last week showed 40 out of 41 economists expect no change, with only one forecasting a cut to -0.25%. More than 80% of economists see rates remaining on hold through year-end, and a strong majority (21 of 25 economists) expect policy to stay unchanged at 0.00% even through 2026.

Swiss Franc has been one of the better performers this month, underpinned by its safe-haven appeal amid persistent geopolitical risks, particularly the war in Ukraine. Expectations of SNB stability have also lent support. That said, the rebound in U.S. and European bond yields has capped further upside for Franc, although the pressure has weighed more heavily on Yen.

Technically, for the near term, further rally is expected in CHF/JPY as long as 55 D EMA (now 183.63) holds. Current rise from 181.45 is seen as the fifth wave of the whole rally from 165.83. It should be on track to 61.8% projection of 173.06 to 186.02 from 181.45 at 189.45.

The bigger hurdle would be in 61.8% projection of 137.40 to 180.05 from 165.83 at 194.88, which could limit upside and bring a more notable consolidation or pullback.

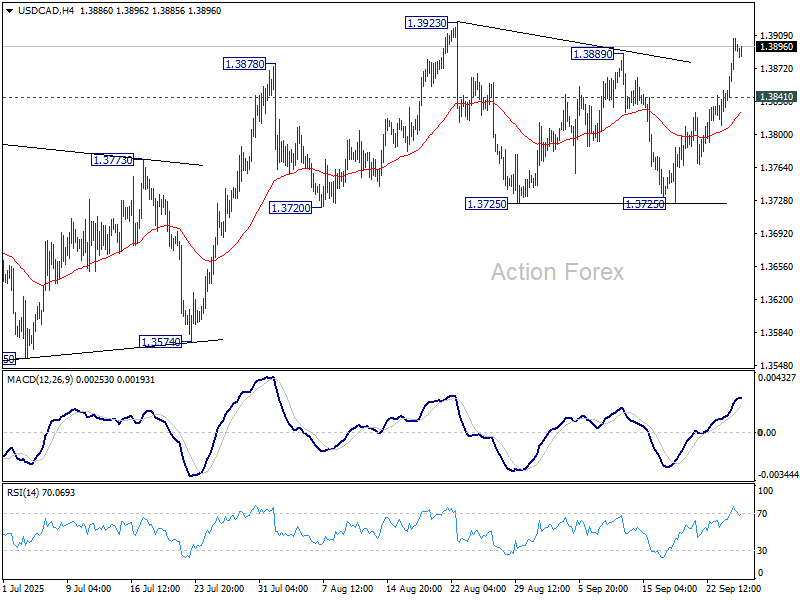

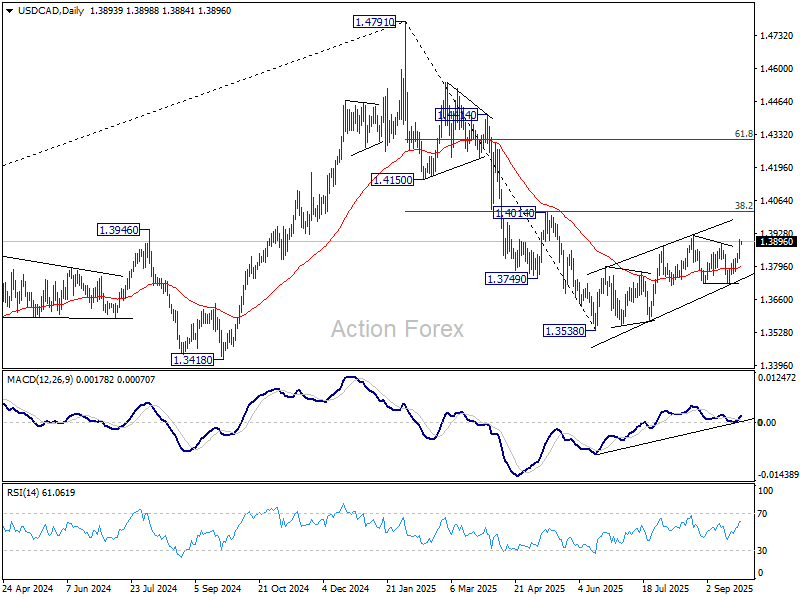

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3815; (P) 1.3832; (R1) 1.3853; More…

USD/CAD’s break of 1.3889 resistance should confirm that consolidations from 13.923 has completed at 1.3725. Corrective rebound form 1.3538 should be resuming. Intraday bias is back on the upside for 1.3923 first. Firm break there will target 1.4014 key cluster resistance. On the downside, however, below 1.3841 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more