In some key ways, the Donald Trump economy, on fire last year but slowing this year, is starting to resemble the one he inherited from his predecessor .

There are the rock-bottom bond yields, plodding economic growth and, not to be understated, the Federal Reserve seemingly pulling all the strings, a role that was only exacerbated in the days since the financial crisis and Great Recession and continues to the present day.

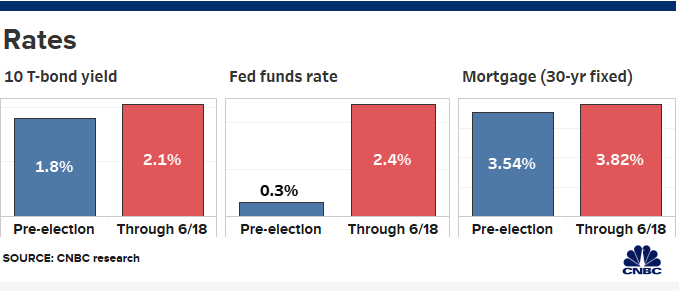

Those similarities came into even sharper focus this week, when the benchmark 10-year Treasury note yield fell below 2% for the first time since Trump became president, and the Fed's indication, if something just short of an outright promise, that it soon will be cutting rates about half a year since its most recent hike.

It wasn't supposed to be this way: The 2017 tax cut and aggressive moves toward deregulation were supposed to pull the U.S. economy out of its glacial move higher. That happened in 2018, but policymakers and Wall Street pros are growing increasingly fearful that a slowdown if not outright recession is on the horizon, and the Fed is being asked again to ride to the rescue.

"You're sort of the same in terms of growth prospects, but not necessarily in the complexion of it," said Peter Boockvar, chief investment officer at Bleakley Advisory Group. "In 2012, 2013, you still had the scars of the great financial crisis. Now those scars have been completely forgotten. Years and years of what the Fed has done I think have brainwashed them to think they can take care of everything."

The Fed may not be able to fix everything, but in Trump's view the central bank is at the core of what's gone wrong.

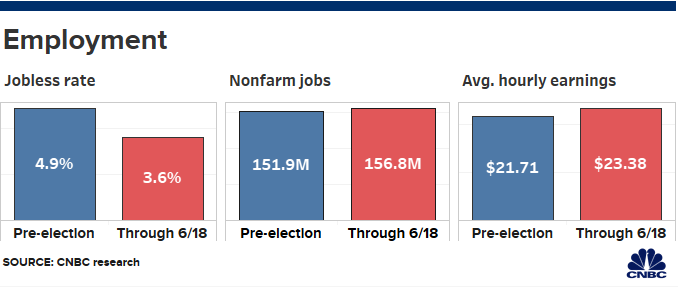

Had the Fed not been so aggressive in raising rates, the president has insisted, the economy would be doing much better. Since Trump took office, the Fed has enacted seven rate hikes, including four in 2018. There were only two increases during Barack Obama's administration, with one coming after the 2016 election.

Different circumstances, similar results

A comparison between the two administrations is difficult considering Obama had the overhang of the financial crisis to deal with but also the benefit of a near-zero fed funds rate plus about $3.5 trillion in stimulus courtesy of the Fed.

Trump's 2.9% GDP growth in 2018 beat any calendar year since the crisis but fell short of his promised 3% or better gain. 2019 appears by all measures to be slowing down, even with the unexpectedly strong 3.1% rate in the first quarter and the unemployment rate at a 50-year low.

What may well be happening is just a simple return to trend, a slow-but-steady environment brought on by an aging workforce and constrained productivity.

"What you're seeing is a reassertion of secular stagnation following the one-time sugar-high associated with the tax cut," said Joseph Brusuelas, chief economist at RSM, citing a term describing the current state of U.S. growth espoused by former Obama advisor Larry Summers and others. "The tax cut did not achieve its intended objective of stimulating capital investment. The economy is moving back to its long-term trend."

At the time the financial crisis hit, the Fed had considerably more wiggle room with policy. The funds rate was at 5.25% when the central bank started cutting in 2007; it is now closer to 2.38%, around the middle of the target range of 2.25% to 2.5%.

The current state of affairs gives the Fed little runway before it reaches what it calls the "zero lower bound," or the lowest point possible before heading into negative nominal rates.

To be sure, all economic cycles are different, and in this one the Fed may not need to go as quickly to zero if it gets ahead of the downturn that the bond market is foreseeing.

In that scenario, one or two cuts might do the same job that the drastic loosening did during the crisis.

"I don't think the Fed is setting the tone here," said Patrick Chovanec, chief strategist at Silvercrest Asset Management and an adjunct professor at Columbia University's School of International and Public Affairs. "It's quite the opposite. There are real economic developments, both positive and negative, that caused growth to accelerate last year and then made the Fed start thinking about tightening and have decelerated this year. There are real economic trends that I don't think the Fed controlled."