Yen Steady After Brief Ripples From BoJ, Dollar Softens Mildly

Yen weakened momentarily after BoJ left monetary policy unchanged as widely expected, but swiftly regained stability. This quick recovery underscores the market’s assessment that the conditions for a BoJ rate hike in April remain intact. This viewpoint is bolstered by unchanged CPI core-core forecast, which holds steady at 1.9% for the upcoming two fiscal years. However, BoJ refrained from offering any immediate signals for such a policy shift. The decision on whether to raise interest rates will depend heavily on the outcomes of the Spring wages negotiations, especially in terms of the breadth of wage growth. Given these circumstances, Yen still faces potential downside risks in the near term.

Meanwhile, Dollar softened mildly in Asian session, correlating with recovery in Hong Kong stock markets. After enduring a prolonged downturn, HSI is showing early signs of stabilization. News that China is mulling a USD 278B stock market rescue package is lifting sentiment mildly. However, it’s still too soon to declare a definitive reversal of the down trend. Risk-off sentiment in Hong Kong and China would continue to support the greenback, and pressure commodity currencies.

The broader currency market remains relatively inactive, with most major pairs and crosses are stuck inside yesterday’s range. Dollar is the worst performer, followed by Canadian and then Yen. Aussie and Kiwi are the stronger ones with Swiss Franc. Euro and Sterling are mixed. The market is likely to experience a lull in volatility today, given the light economic calendar. However, activity is expected to pick up with tomorrow’s release of New Zealand’s CPI and global PMI data, which could trigger more pronounced movements.

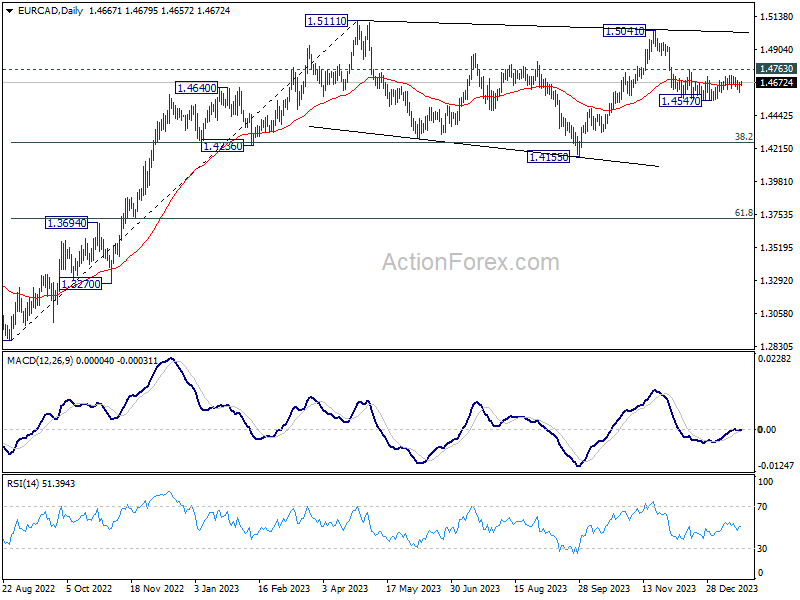

Technically, EUR/CAD is extending the consolidation from 1.4547 at this point. Further decline is in favor as long as 1.4763 minor resistance holds. Below 1.4547 will resume the fall from 1.5041. However, as price actions from 1.5111 are seen as a sideway pattern only, strong support should emerge around 1.4155 to bring rebound. Meanwhile, break of 1.4763 will bring retest of 1.5041 resistance instead. Given that both BoC (Wednesday) and ECB (Thursday) will announce interest rate decision this week, EUR/CAD is a pair that’s worth some attention.

In Asia, at the time of writing, Nikkei is up 0.09%. Hong Kong HSI is up 2.92%. China Shanghai SSE is up 0.36%. Singapore Strait Times is up 0.03%. Japan 10-year JGB yield is down -0.0089 at 0.645. Overnight, DOW rose 0.36%. S&P 500 rose 0.22%. NASDAQ rose 0.32%. 10-year yield fell -0.052 to 4.094.

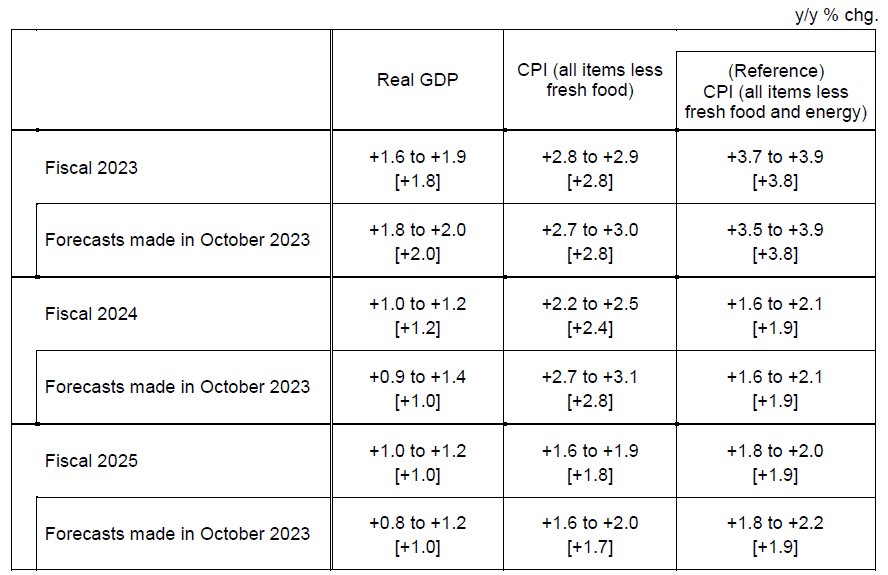

BoJ holds steady, with CPI core-core projected at 1.9% in next two fiscal years

BoJ let monetary policy unchanged as widely expected. The forecast for fiscal 2024 CPI core was downgraded, whereas fiscal 2025 CPI core forecast saw a slight upgrade. Notably, CPI core-core forecasts for fiscal 2024 and 2025 were left unchanged at 1.9%, indicating a steady path towards achieving Japan’s 2% inflation target sustainably.

Under Yield Curve Control, BoJ kept short-term policy interest rate unchanged at -0.1%. Additionally, target for 10-year JGB yield remains around 0%, with an allowance for fluctuation below 1.0% upper bound. These decisions were made by unanimous vote.

BoJ noted, “Consumer inflation is likely to increase gradually toward the BoJ’s target as the output gap turns positive, and as medium- to long-term inflation expectations and wage growth heighten.” The central bank also acknowledged the growing “likelihood” of realizing this outlook, albeit with an emphasis on the continued “high uncertainties” surrounding future developments.

In the median economic projections:

- Fiscal 2023 GDP growth at 1.8% (down from October’s 2.0%).

- Fiscal 2024 GDP growth at 1.2% (up from 1.0%).

- Fiscal 2025 GDP growth at 1.0% (unchanged).

On the inflation front:

- Fiscal 2023 CPI core at 2.8% (unchanged).

- Fiscal 2024 CPI core at 2.4% (down from 2.8%).

- Fiscal 2025 CPI core at 1.8% (up from 1.7%).

- Fiscal 2023 CPI core-core at 3.8% (unchanged).

- Fiscal 2024 CPI core-core at 1.9% (unchanged).

- Fiscal 2025 CPI core-core at 1.9% (unchanged).

Australia’s NAB business confidence rises to -1 amidst slowing price growth

Australia NAB Business Confidence fell rose from -8 to -1 in December. However, Business Conditions fell from 9 to 7. The decline was observed across several key areas: Trading conditions dropped from 13 to 10, while Employment conditions also decreased slightly from 8 to 7. Profitability conditions remained steady at 6.

NAB Chief Economist Alan Oster noted that “confidence and conditions are softest in manufacturing, retail and wholesale,” attributing this to consumers cutting back on spending over time. Although there was a pickup in confidence within the retail sector in December, Oster expressed caution, stating that “it remains to be seen if this will be maintained.”

Another significant development was the sharp decline in price and cost growth. Labor cost growth eased to 1.8% in quarterly equivalent terms, down from 2.3%. Purchase cost growth also declined from 2.5% to 1.6%. Overall price growth slowed from 1.2% to 0.9%, with notable decrease in retail price growth from 1.8% to 0.6%.

Oster highlighted the significance of this decline in retail price growth, attributing it in part to the sales periods around Black Friday and Christmas. He remarked, “The marked fall in retail price growth in December… is nonetheless an encouraging sign that inflation may have eased at the end of the quarter.”

New Zealand BNZ services falls to 48.8, back in contraction

New Zealand BusinessNZ Performance of Services Index fell from 51.1 to 48.8 in December, back into contraction territory. This downturn also brings the index below long-term average of 53.4. The increase in negative sentiment is evident, with the proportion of negative comments rising from 54.0% to 58.7%. The primary concerns expressed by businesses revolve around seasonal factors, increasing costs of living, and an overall economic slowdown.

Breaking down the PSI, several key components showed declines. Activity and sales dropped from 48.7 to 47.1, employment fell from 50.6 to 47.5, and new orders/business dipped from 52.2 to 51.2. Additionally, stocks and inventories decreased from 55.0 to 51.5, while supplier deliveries also saw a reduction from 52.8 to 50.5.

Stephen Toplis, BNZ’s Head of Research noted that the softening in PSI, combined with the previously reported weakness in Performance of Manufacturing Index, paints a concerning picture for New Zealand’s near-term economic growth and employment. While tourism has been a critical driver for the services sector and is expected to continue supporting the economy, Toplis emphasized that it cannot solely bear the burden of economic revitalization.

Looking ahead

UK public sector net borrowing, Eurozone consumer, and Canada new housing prices are the only features in the calendar today.

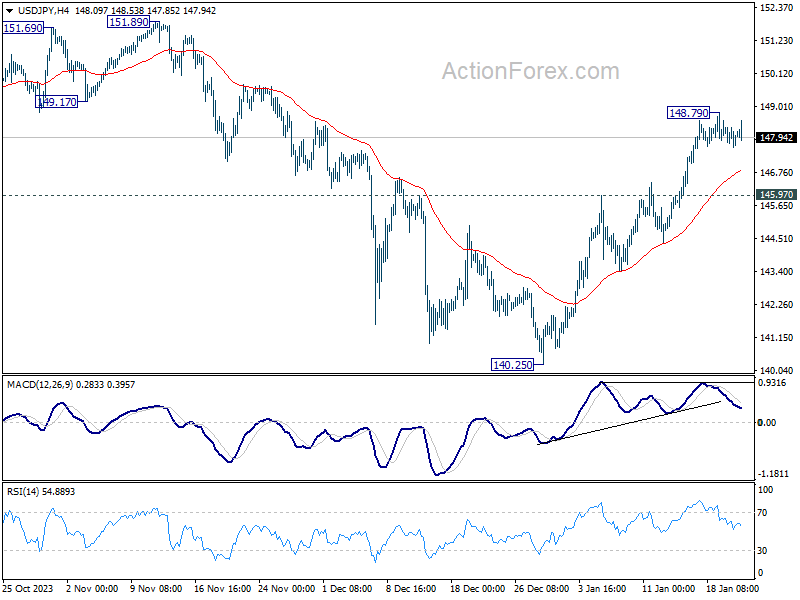

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.71; (P) 148.03; (R1) 148.44; More…

Intraday bias in USD/JPY remains neutral for the moment. Consolidation from 148.79 temporary top could extend further, and deeper retreat cannot be ruled out. But further rally is expected as long as 145.97 resistance turned support holds. Corrective fall from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone.

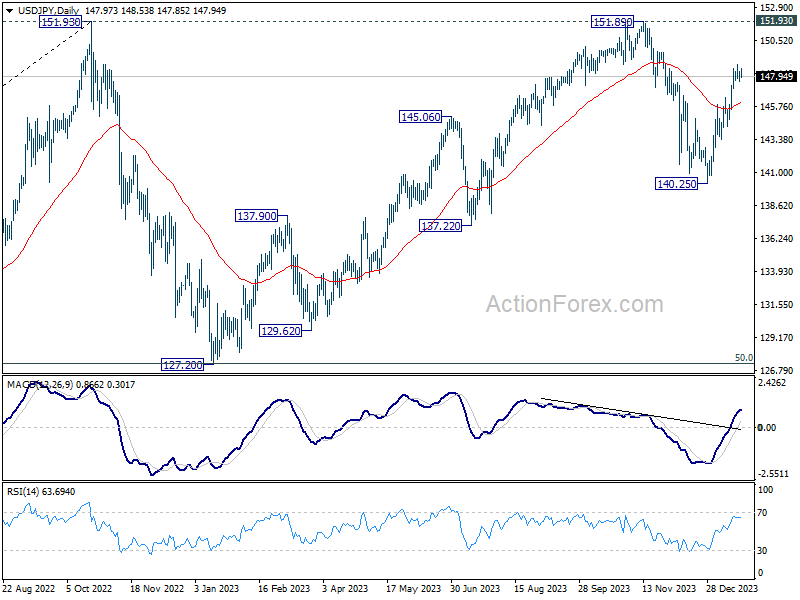

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 141.89) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Dec | 48.8 | 51.2 | 51.1 | |

| 00:30 | AUD | NAB Business Conditions Dec | 7 | 9 | ||

| 00:30 | AUD | NAB Business Confidence Dec | -1 | -9 | ||

| 03:09 | JPY | BoJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Dec | 11.2B | 13.4B | ||

| 13:30 | CAD | New Housing Price Index M/M Dec | 0.00% | -0.20% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Jan P | -14 | -15 |

When The Wave Turns

Why Retirement Investing Is Moving Towards Resilience Jeremy Grantham’s latest market warnings have revived an old tru... Read more

Gyrostat Capital Management: July Retirement Portfolio Resilience Assessment

The Market Is Currently Presenting an Opportunity to Strengthen Retirement Portfolio Resilienc... Read more

The Invisible Risk That Decides Your Retirement

Why how investors behave matters more than what markets do and what disciplined port... Read more

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more