Yens Sharp Rebound Amid Global Yield Dip: Central Bank Rate Cut Bets In Focus

Japanese Yen surged sharply in European session, bolstered by significant dips in Germany’s 10-year government bond yield, which reached its lowest level since early September. Concurrently, US 10-year yield also briefly fell below 4.4% mark.

This movement in the bond markets reflects an aggressive stance by traders betting on rate cuts by major central banks in the upcoming year. Traders had been speculating about a full percentage point cut in interest rates by both ECB and Fed by the end of 2024. However, as the market regained its composure and yields recovered, Yen’s rally also lost some of its initial momentum.

Despite the market’s anticipatory stance, it seems premature to heavily bet on rate cuts just yet. Central bankers are still leaving the door open for further rate hikes. For instance, Bundesbank President Joachim Nagel stated today, “Are we there yet? Have we seen the peak in interest rates? That is not clear yet.” Similarly, ECB Governing Council member Robert Holzmann suggested that it might be “somewhat early” for a rate cut in the second quarter .

In the broader forex markets, most major pairs and crosses are trading within the ranges set yesterday. Dollar is showing some softness alongside Sterling and New Zealand Dollar. Australian Dollar and Canadian Dollar are faring better, though Yen currently overshadows them.

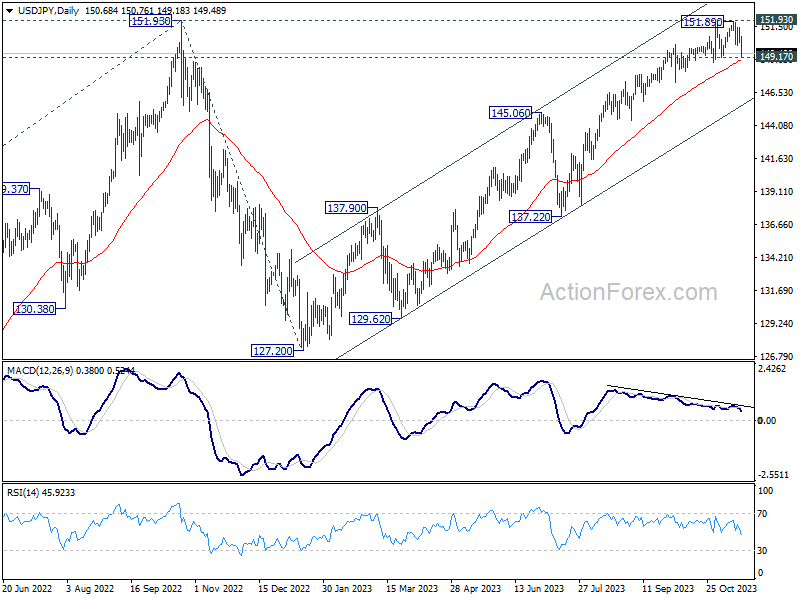

From a technical standpoint, USD/JPY is now pressing 149.17 support with today’s steep fall. Firm break there should confirm rejection by 151.93 key resistance, and bring deeper decline towards medium term channel support (now at around 145.71). As the week draws to a close, it remains to be seen whether Yen can achieve this significant breakthrough.

In Europe, at the time of writing, FTSE is up 1.00%. DAX is up 0.86%. CAC is up 0.92%. Germany 10-year yield is down -0.015 at 2.583. Earlier in Asia, Nikkei rose 0.48%. Hong Kong HSI dropped -2.12%. China Shanghai SSE rose 0.11%. Singapore Strait Times dropped -0.27%. Japan 10-year JGB yield dropped -0.043 to 0.748.

Eurozone CPI finalized at 2.9% yoy in Oct, core at 4.2% yoy

Eurozone CPI was finalized at 2.9% yoy in October, down from September’s 4.3% yoy. CPI core (excluding energy, food, alcohol & tobacco) was finalized at 4.2% yoy, down from previous reading of 4.5% yoy. The highest contribution came from services (+1.97%), followed by food, alcohol & tobacco (+1.48%), non-energy industrial goods (+0.90%) and energy (-1.45%).

EU CPI was finalized at 3.6% yoy, down from prior month’s 4.9% yoy. The lowest annual rates were registered in Belgium (-1.7%), the Netherlands (-1.0%) and Denmark (-0.4%). The highest annual rates were recorded in Hungary (9.6%), Czechia (9.5%) and Romania (8.3%). Compared with September, annual inflation fell in twenty-two Member States and rose in five.

UK retail sales volume down -0.3% mom in Sep, sales value down up 0.1% mom

UK retail sales volume fell -0.3% mom in September, much worse than expectation of 0.3 mom rise. Ex-automotive fuel sales volume fell -0.1% mom. Looking broader, sales volumes (include and excluding fuel) fell by -1.1% in the three months to October 2023 when compared with the previous three months.

In value term, retail sales rose 0.1% mom while ex-fuel sales was flat 0.0% mom.

BoJ’s Ueda reiterates patience in maintaining ultra-loose policy

BoJ Governor Kazuo Ueda has once again underscored the central bank’s commitment to maintaining its ultra-loose monetary policy, emphasizing the need for patience in the face of uncertain inflation dynamics.

Speaking to the parliament, Ueda noted, “Trend inflation is likely to gradually accelerate toward our 2% inflation target through fiscal 2025. But this needs to be accompanied by a positive wage-inflation cycle.”

“Uncertainty on whether Japan will see such a positive wage-inflation cycle is high,” he added.

Addressing the behavior of 10-year JGB yields, Ueda expressed that he does not foresee a sharp rise above the 1% reference level, even under upward pressure.

Looking ahead, Ueda clarified the bank’s position on potentially ending its Yield Curve Control and negative interest rate policies, stating, “We will consider ending YCC, negative rate if we can expect inflation to stably, and sustainably hit the price target.”

He added that the order of adjustments to the policy would be contingent on various factors, including economic conditions, price movements, and market developments.

EUR/USD Mid-Day Outlook

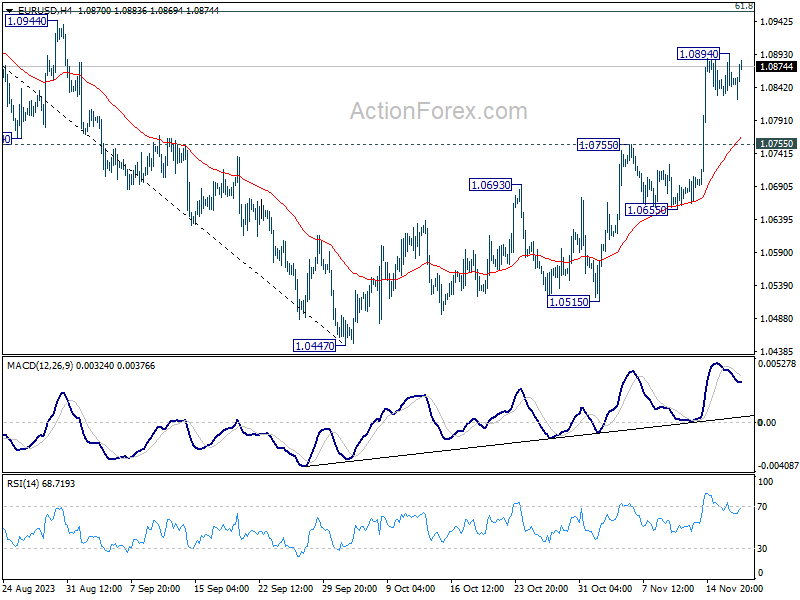

Daily Pivots: (S1) 1.0823; (P) 1.0860; (R1) 1.0889; More…

Intraday bias in EUR/USD stays neutral at this point, as consolidation continues below 1.0984. In case of deeper retreat, downside should be contained by 1.0755 resistance turned support to bring another rally. On the upside, above 1.0894 will resume the rebound from 1.0447 to 61.8% retracement of 1.1274 to 1.0447 at 1.0958 next.

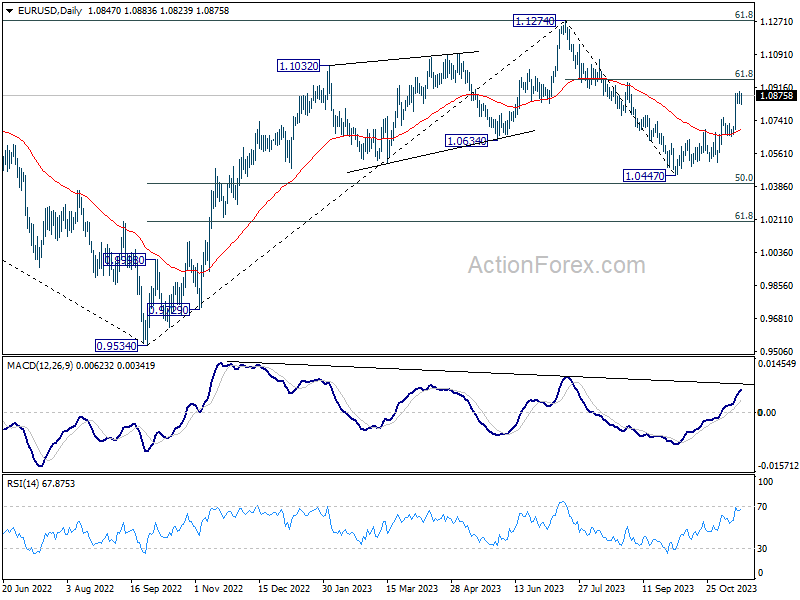

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. However, break of 1.0447 will resume the fall to 61.8% retracement of 0.9543 to 1.1274 at 1.0199.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | PPI Input Q/Q Q3 | 1.20% | 0.20% | -0.20% | |

| 21:45 | NZD | PPI Output Q/Q Q3 | 0.80% | 0.40% | 0.20% | |

| 07:00 | GBP | Retail Sales M/M Oct | -0.30% | 0.30% | -0.90% | -1.10% |

| 09:00 | EUR | Eurozone Current Account (EUR) Sep | 31.2B | 20.3B | 27.7B | 30.8B |

| 10:00 | EUR | Eurozone CPI Y/Y Oct F | 2.90% | 2.90% | 2.90% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct F | 4.20% | 4.20% | 4.20% | |

| 13:30 | CAD | Industrial Product Price M/M Oct | -1.00% | 0.20% | 0.40% | |

| 13:30 | CAD | Raw Material Price Index Oct | -2.50% | -2.00% | 3.50% | 3.90% |

| 13:30 | USD | Building Permits Oct | 1.49M | 1.45M | 1.47M | |

| 13:30 | USD | Housing Starts Oct | 1.37M | 1.36M | 1.36M |

When The Wave Turns

Why Retirement Investing Is Moving Towards Resilience Jeremy Grantham’s latest market warnings have revived an old tru... Read more

Gyrostat Capital Management: July Retirement Portfolio Resilience Assessment

The Market Is Currently Presenting an Opportunity to Strengthen Retirement Portfolio Resilienc... Read more

The Invisible Risk That Decides Your Retirement

Why how investors behave matters more than what markets do and what disciplined port... Read more

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more