Yen Falls As Inverse Risk Correlation Back In Play

Risk appetite was strong in Asian markets today, with several centers returning from Lunar New Year holidays and equities advancing. South Korea led the gains, with the Kospi hitting a fresh record high, driven by strength in technology heavyweights like Samsung Electronics and SK Hynix. Japan’s Nikkei also posted notable gains, although it remains below its historic peak.

Against this backdrop, Yen trades broadly lower, and the selloff appears to be gathering momentum. For the Japanese currency, the immediate question is whether the post-election rally has fully run its course and the cross-asset relationship with risk sentiment — traditionally inverse — is reasserting itself.

Meanwhile, Dollar jumped broadly higher overnight and remains generally firm this morning. Minutes from the January FOMC meeting indicated that another rate cut in the first half of the year is far from warranted. The fact that some Fed officials even brought up the idea of a rate hike on the table — albeit prematurely — was enough to perk up USD sentiment.

Aussie is also firmer today, buoyed by solid Australian job data that moves RBA one step closer to another hike in May. The firm labor prints reinforce the case that domestic monetary tightening may continue if inflation doesn’t ease materially.

Geopolitically, peace talks in Geneva appeared stuck without a major breakthrough. U.S.–Iran nuclear talks showed only modest progress, and Iran has not fully addressed U.S. red lines, according to Vice President JD Vance, prompting warnings that military options remain an option. Meanwhile, two days of Ukraine-Russia peace talks concluded without a breakthrough, and Ukrainian President Zelenskiy expressed dissatisfaction with the outcome. That uncertainty helped keep oil prices elevated and supported haven assets like Gold, even as markets remain cautiously positioned.

On the FX leaderboard this week, Dollar remains the strongest so far, followed by Kiwi and Loonie. Yen is the weakest, trailed by Sterling and then Kiwi. Euro and Swiss Franc sit in the middle.

In Asia, Nikkei rose 0.55%. Hong Kong and China were still on holiday. Singapore Strait Times is up 1.22%. Japan 10-year JGB yield is up 0.006 at 2.146. Overnight, DOW rose 0.26%. S&P 500 rose 0.56%. NASDAQ rose 0.78%. 10-year yield rose 0.027 to 4.079.

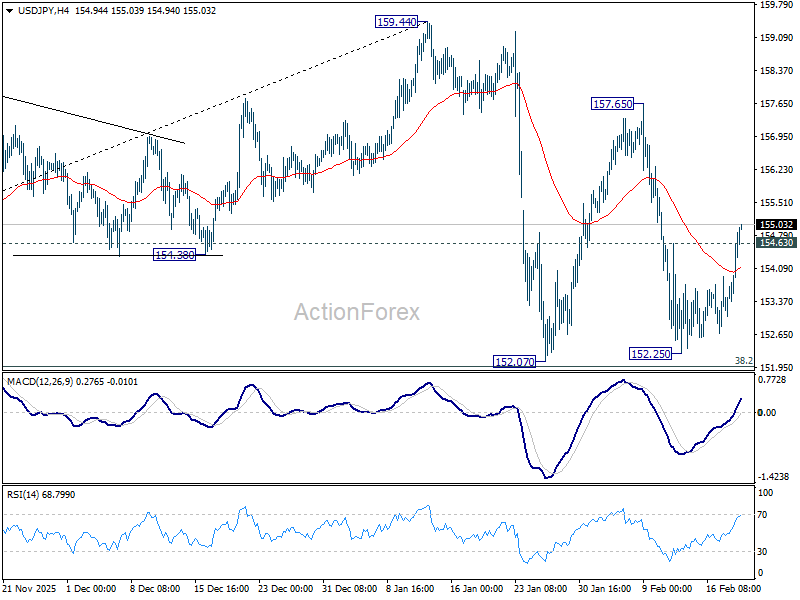

Rate hike mention in Fed minutes boosts dollar, USD/JPY back at 155

Dollar rallied across the board after release of FOMC minutes that were interpreted as more hawkish than markets anticipated. Strength was most visible against Yen, with USD/JPY back at around 155.

The key takeaway is not that the Fed is turning hawkish, but that uncertainty around future cuts is greater than previously assumed. While easing remains the base case, the minutes make clear that it is far from guaranteed. Risks to Fed’s dual mandate appear to have shifted. “Vast majority” of policymakers judged that downside risks to employment have “moderated”, while risks of persistent inflation “remained”. Some participants even commented that the balance of risks had moved back toward inflation.

One striking detail was that “several” officials floated the possibility of rate hikes if inflation fails to recede. The minutes noted that a two-sided description of future policy — including potential upward adjustments — could be appropriate under certain conditions. At the same time, “some” participants argued for holding rates steady for an extended period until disinflation progress is firmly back on track. Others reiterated that further easing would be appropriate if inflation declines as expected. The debate highlights the tilt against imminent cuts.

Market reaction was restrained but notable. March hold probability rose toward 94%, and June cut odds hover near 61%. The shift is incremental rather than dramatic But for Dollar, nuance mattered. The suggestion that hikes are back on table — even if unlikely — shifts perceived policy asymmetry. That underpins USD strength, particularly against low-yielders such as Yen.

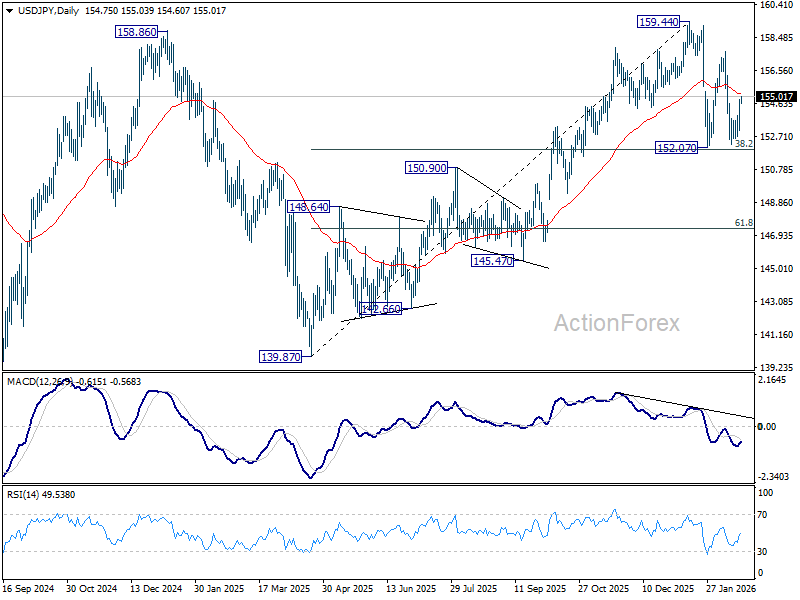

Technically, USD/JPY’s extended rebound and break of 154.63 minor resistance suggests that fall from 157.65 has completed at 152.25 already. 38.2% retracement of 139.87 to 159.44 at 151.96 is well defended. That keeps the price structure from 159.44 corrective, and also keeps the up trend from 139.87 (2025 low) intact. More upside would now likely be seen back to 157.65/159.44 resistance zone, even though a break above 159.44 to resume the up trend still looks premature.

Australia unemployment rate unchanged at 4.1%, jobs solid enough to keep RBA May hike in play

Australia added 17.8k jobs in January, slightly below expectations of 20.3k, but the details were firm. Full-time employment rose a strong 50.5k, while part-time positions fell -32.7k. Unemployment rate held steady at 4.1%, undershooting forecasts for a rise to 4.2%, with participation unchanged at 66.7%. Monthly hours worked increased 0.6% mom, reinforcing signs of steady labor demand.

The composition matters. The shift toward full-time employment and higher hours worked suggests underlying strength rather than softening. Taken together, the data indicate the labor market remains relatively tight, with the economy still operating close to capacity.

From the RBA’s perspective, the failure of employment conditions to weaken keeps inflation risks front and center. A cooling labor market would have allowed policymakers to shift focus toward growth risks. Instead, today’s figures reinforce the view that wage pressures may remain sticky.

The base case remains for another 25bps rate hike in May, pending Q1 CPI confirmation. Whether further tightening is needed beyond that remains an open question. But for now, the labor market is not providing the RBA with any comfort that inflation pressures will fade on their own.

RBNZ’s Silk: Growth and disinflation can coexist amid spare capacity

Following the RBNZ’s decision to keep the OCR at 2.25% yesterday, Assistant Governor Karen Silk emphasized that the economy can grow even as inflation moderates.

She acknowledged that the idea may appear counterintuitive but argued that the output gap provides room for above-trend growth without reigniting price pressures. But, according to Silk, the presence of spare capacity allows output to grow above potential temporarily without reigniting inflation.

Silk described risks around the projected cash-rate path as balanced. While some sectors are showing signs of recovery, consumption remains subdued. At the same time, she warned of upside inflation risks if firms facing squeezed margins begin raising prices more aggressively.

The RBNZ estimates the neutral cash rate at around 3%, suggesting policy is still accommodative. Current projections show only a gradual move toward that neutral level by late 2027. “That’s a reflection of that spare capacity that exists within the economy and the time it will take for that to be absorbed,” Silk said.

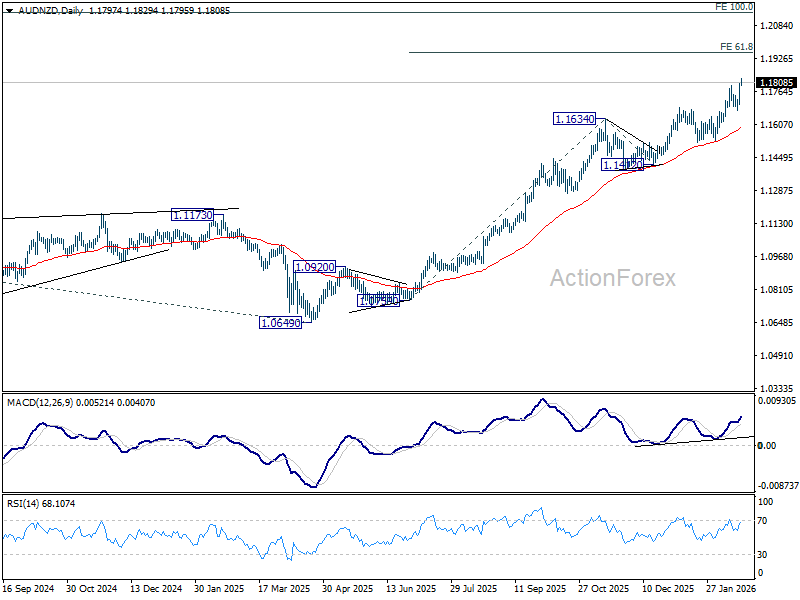

AUD/NZD eyes 1.20 after break to 13 year high

AUD/NZD’s medium-term uptrend resumed this week, lifting the cross to its highest level since 2013. The move extends a rally that began in mid-2025 and reflects widening policy divergence between the RBA and RBNZ.

The initial leg higher was driven by aggressive rate cuts from RBNZ, which pushed the OCR down to 2.25% and weakened Kiwi across the board. Momentum then re-accelerated earlier this month after RBA reversed course and resumed tightening, lifting the cash rate to 3.85%.

Fresh upside impetus came from disappointment over RBNZ’s policy hold this week. While projections showed a slightly higher future rate path, markets had hoped for a clearer hawkish signal.

Realistically, RBNZ may deliver at most one hike by year-end from current levels, with the OCR only slowly moving toward the estimated neutral rate near 3.00% by late 2027. That path contrasts sharply with Australia’s more immediate tightening bias.

Today’s robust Australian jobs data strengthened the divergence narrative. RBA remains on track for another hike in May. If inflation proves sticky and labor conditions fail to ease, risk of further tightening beyond May cannot be ruled out.

Technically, AUD/NZD is now targeting the 61.8% projection of 1.0795 to 1.1634 from 1.1412 at 1.1931. In any case, outlook will remain bullish as long as 1.1634 resistance turned support holds.

Momentum could carry the pair through the 1.20 handle, but upside may begin to fade as positioning becomes stretched. The broader medium-term hurdle sits at the 100% projection of 0.9992 (2020 low) to 1.1489 (2022 high) from 1.0649 (2025 low) at 1.2146.

Even with another RBA hike, clearing that barrier at 1.2146 decisively would require a more material shift in central bank outlooks, which is unlikely for now. On the other hand, a topping formation between 1.2000 and 1.2146 would be likely, in particular, if RBNZ’s tightening timeline accelerates unexpectedly or if Australian data begin to soften materially.

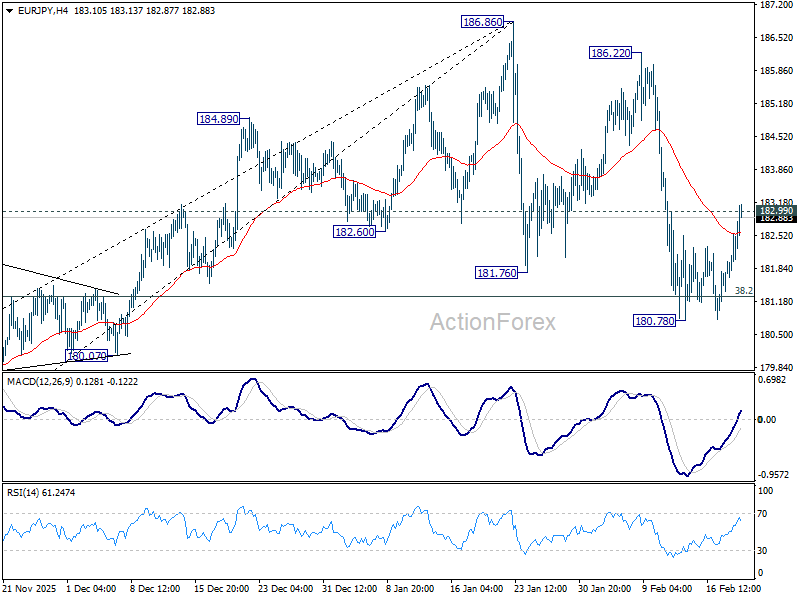

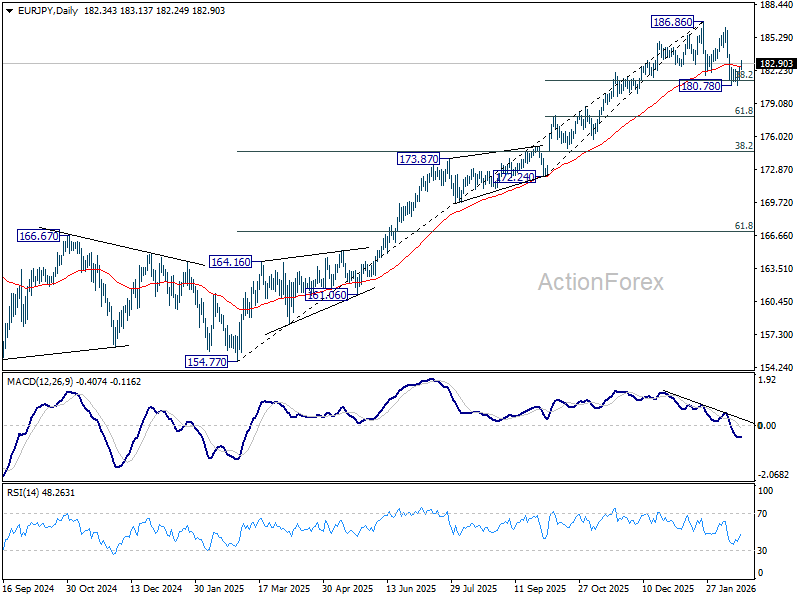

EUR/JPY Daily Outlook

Daily Pivots: (S1) 181.67; (P) 182.10; (R1) 182.89; More…

EUR/JPY’s break of 182.99 minor resistance argues that a short term bottom was formed at 180.78, after drawing support from 38.2% retracement of 172.24 to 186.86 at 181.27. Intraday bias is back on the upside for retesting 186.22/186.86 resistance zone first. One the downside, however, sustained break of 181.27 will argue that fall from 186.86 is correcting whole up trend from 154.77.

In the bigger picture, considering bearish divergence condition in D MACD and break of 55 D EMA, a medium term top could be formed at 186.86 already. Deeper correction would be seen but downside should be contained by 38.2% retracement of 154.77 to 186.86 at 174.60 to bring rebound. Meanwhile, firm break of 186.86 will resume larger up trend to 78.6% projection of 124.37 to 175.41 from 154.77 at 194.88 next.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more