Yen Down On Japan Wage Data; China Trade Figures Sends Aussie Lower

Today’s Asian session witnessed a revitalized forex market, triggered largely by pivotal economic data releases. Japan’s weaker-than-anticipated wage growth data placed Yen under notable pressure, reinforcing BoJ’s commitment to persist with its ultra-loose monetary policy. Simultaneously, unexpectedly poor trade figures from China exerted downward force on Hong Kong stocks, as well as on Australian and New Zealand dollars.

Conversely, Dollar is showing signs of a near-term rally resurgence. An imminent breakout from its recent range seems likely, especially when pitted against Yen and commodity-linked currencies. For the time being, European majors are holding steady, oscillating in their respective ranges both against Dollar and amongst themselves.

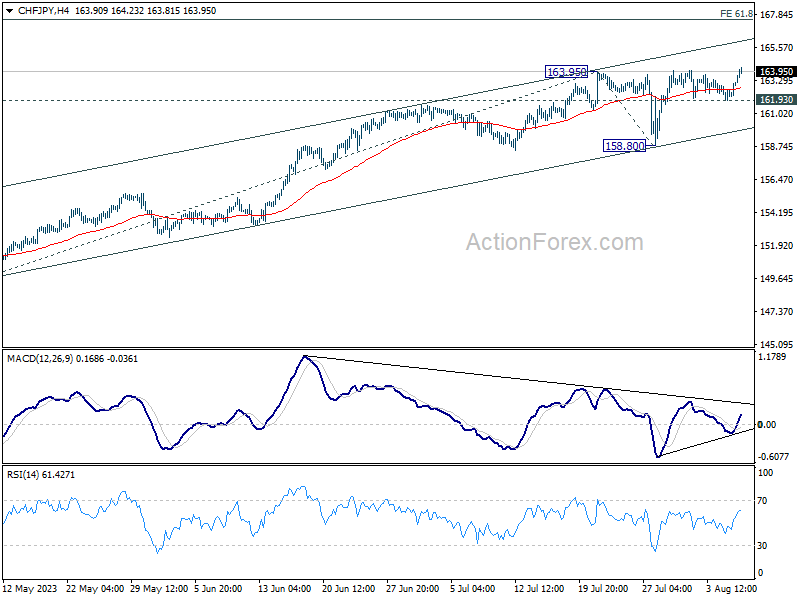

Technically, CHF/JPY looks ready to resume its record run with today’s strong rally. For now, outlook will stay bullish as long as 161.93 support holds, even in case of retreat. Next target is 61.8% of 149.77 to 163.95 from 158.80 at 167.56. A point of attention will be on whether 4H MACD could break above its falling trend line to signal a new phase of upside acceleration.

In Asia, at the time of writing, Nikkei is up 0.50%. Hong Kong HSI is down -1.46%. China Shanghai SSE is down-0.16%. Singapore Strait Times is up 0.12%. Japan 10-year JGB yield is down -0.016 to 0.612. Overnight, DOW rose 1.16%. S&P 500 ro se0.90%. NASDAQ rose 0.6%. 10-year yield rose 0.018 to 4.078.

Japan’s wages growth and household spending miss expectations, supports ultra-loose BoJ

Today’s wage growth data out of Japan came in softer than anticipated, reinforcing BoJ’s position towards maintaining its ultra-loose monetary strategy. Furthermore, the consistent decline in real wages continues to weigh down consumer spending.

Nominal cash earnings for workers in June grew by only 2.3% yoy, missing the projected 3.0% yoy rise. This marks a deceleration from previous month’s impressive 2.9% yoy – the most robust growth observed in nearly 30 years. Delving deeper, June’s base salary advance was logged at 1.4% yoy, , also under May’s 1.7% yoy .

Economists have previously estimated that wage increases of 3% or more are crucial to sustain consumer inflation above BoJ’s 2% target.

Compounding concerns, real cash earnings continued their downward trajectory, recording a decline of -1.6% yoy, faring worse than the anticipated stasis at -0.9% yoy. This represents the 15th consecutive month of negative readings in this domain.

Furthermore, overall household spending for June saw a contraction of -4.2% yoy, veering further off the expected -3.5% yoy decline. This marks the fourth consecutive month of shrinking household spending.

These lackluster wage figures pose a challenge for the BoJ. As Governor Kazuo Ueda remarked, the trajectory of income trends is pivotal in determining the realistic prospects of accomplishing lasting inflation. Today’s data lends credence to the BoJ’s recent evaluation that consistently achieving price increments beyond 2% remains a distant goal. Consequently, the need to uphold its ultra-accommodative monetary parameters becomes ever more evident.

Australia’s Consumer Sentiment down -0.4%, no lift from RBA pause

Australia’s Westpac Consumer Sentiment Index for August indicated a slight decline, registering at 81, a drop of -0.4% mom from July’s reading of 81.3. Westpac’s analysis suggests that this decrease cements the prevailing pessimistic mood among consumers. Interestingly, RBA’s decision to pause rate hikes did not notably influence this sentiment. The prevailing concerns about inflation continue to overshadow, although confidence in the job market did see a marginal improvement.

Regarding RBA’s upcoming meeting on September 5, Westpac anticipates the central bank will maintain its current stance, leaving rates untouched at 4.1%. This cash rate is expected to be the zenith of this financial cycle. It is now up to incoming data and unfolding economic scenarios to present a compelling argument for further monetary tightening.

Westpac emphasized that for RBA to be prompted into action, any economic developments would need to be not just surprising, but also substantial, essentially posing a challenge to the bank’s medium-term outlook.

Australia NAB business confidence rose to 2, inflationary pressures on the rise

Australia’s NAB Business Confidence Index for July revealed an upward tick, moving from -1 in June to 2. However, Business Conditions saw a slight dip from 11 to 10. Delving into specific metrics, readings for trading conditions, profitability, and employment remained unchanged with the previous month, all settling at 16, 10, and 6 respectively.

Notably, the month saw a pronounced rise in price and cost growth. Labour cost growth surged to 3.7% in quarterly equivalent terms, up from June’s 2.3%, and purchase cost growth escalated to 2.6%, a jump from the previous month’s 2.2%. Furthermore, final price growth climbed to 2%, doubling June’s 1%.

Commenting on the findings, NAB Chief Economist, Alan Oster, remarked, “Business conditions in July remained resilient and have largely held steady at above-average levels over the past few months.”

He added, “While business confidence rebounded to positive territory, overall confidence remains muted.”

Oster further noted the inflationary pressures highlighted by the survey, noting, “Despite the Q2 CPI release indicating an improvement, the survey underscores that the upward pressure on inflation remains significant.”

China’s exports down -14.5% yoy in Jul, shipments to ASEAN down -21.4% yoy

July saw a sharper-than-expected contraction in China’s exports, with decline of -14.5% yoy to USD 281.76B. This marked the steepest drop since February 2020 and exceeded market expectations, which had forecasted a decline of -12.5% yoy. Concurrently, imports also took a hit, plunging by -12.4% yoy to USD 201.16B, much steeper than anticipated -5% yoy drop.

With these declines, China’s trade surplus unexpectedly widened. July’s figures show surplus expanding from USD 70.6B to USD 80.6B, surpassing the market forecast of USD 67.8B.

A key observation was the sharp decline in shipments to ASEAN – one of China’s primary trade partners. Exports to ASEAN dropped by a significant -21.43% yoy in July, marking its second straight monthly decline. This is noteworthy as ASEAN had played a pivotal role in bolstering China’s export sector earlier in the year.

In addition, exports to EU and US followed suit with declines of -20.62% yoy and -23.12% yoy, respectively. The dip in shipments to US represents a continued trend, with July marking the twelfth consecutive month of decline.

Looking ahead

Trade balance data from France, US and Canada will be the main focuses in a rather light day.

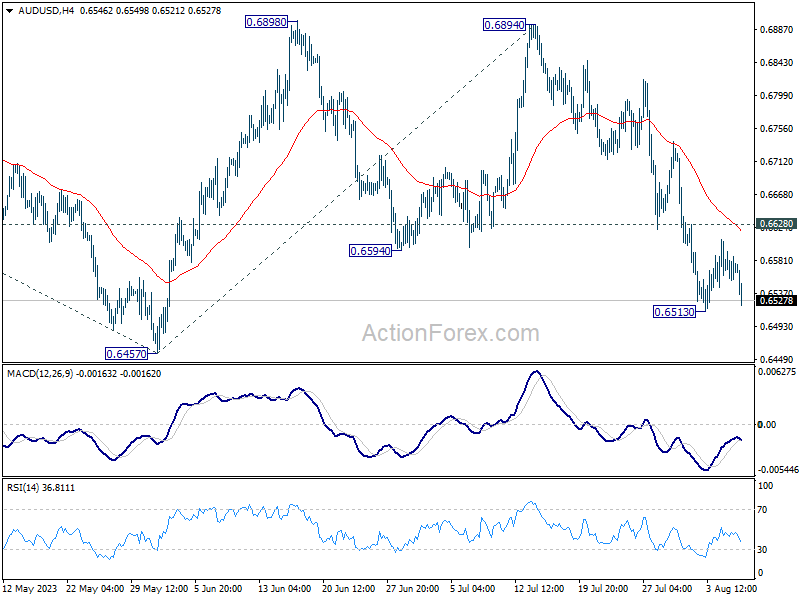

AUD/USD Daily Report

Daily Pivots: (S1) 0.6555; (P) 0.6574; (R1) 0.6593; More…

AUD/USD dips notably today but stays above 0.6513 temporary low. Intraday bias stays neutral first, and outlook remains bearish. Current development argues that larger fall from 0.7156 is still in progress. Below 0.6513 will bring retest of 0.6457 support first. Firm break there will confirm this case and target 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195. Nevertheless, on the upside, above 0.6628 minor resistance will mix up the outlook and turn bias back to the upside for stronger rebound.

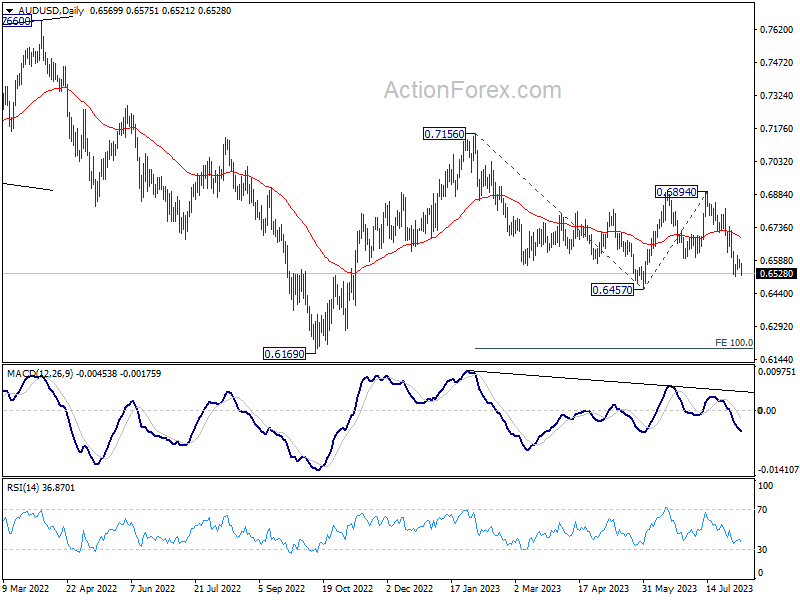

In the bigger picture, outlook is mixed for now as AUD/USD failed to sustain above both 55 D EMA (now at 0.6686) and 55 W EMA (now at 0.6769). On the upside, break of 0.6894 resistance will solidify the case that down trend from 0.8006 (2021 high) has already completed, and target 0.7156 resistance for confirmation. However, break of 0.6457 will likely resume the down trend through 0.6169 (2022 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Jul | 1.80% | 3.00% | 4.20% | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Jun | 2.30% | 3.00% | 2.50% | 2.90% |

| 23:30 | JPY | Overall Household Spending Y/Y Jun | -4.20% | -3.50% | -4.00% | |

| 23:50 | JPY | Bank Lending Y/Y Jul | 2.90% | 3.10% | 3.20% | |

| 23:50 | JPY | Current Account (JPY) Jun | 2.35T | 2.24T | 1.70T | |

| 00:30 | AUD | Westpac Consumer Confidence Aug | -0.40% | 2.70% | ||

| 01:30 | AUD | NAB Business Conditions Jul | 10 | 9 | 11 | |

| 01:30 | AUD | NAB Business Confidence Jul | 2 | 0 | -1 | |

| 03:00 | CNY | Trade Balance (USD) Jul | 80.6B | 67.8B | 70.6B | |

| 03:00 | CNY | Trade Balance (CNY) Jul | 576B | 470B | 491B | |

| 05:00 | JPY | Eco Watchers Survey: Outlook Jul | 54.4 | 54.5 | 53.6 | |

| 06:00 | EUR | Germany CPI M/M Jul F | 0.30% | 0.30% | ||

| 06:00 | EUR | Germany CPI Y/Y Jul F | 6.20% | 6.20% | ||

| 06:45 | EUR | France Trade Balance (EUR) Jun | -8.0B | -8.4B | ||

| 10:00 | USD | NFIB Business Optimism Index Jul | 90.6 | 91 | ||

| 12:30 | USD | Trade Balance (USD) Jun | -65.2B | -69.0B | ||

| 12:30 | CAD | Trade Balance (CAD) Jun | -1.7B | -3.4B | ||

| 14:00 | USD | Wholesale Inventories Jun F | -0.30% | -0.30% |

When The Wave Turns

Why Retirement Investing Is Moving Towards Resilience Jeremy Grantham’s latest market warnings have revived an old tru... Read more

Gyrostat Capital Management: July Retirement Portfolio Resilience Assessment

The Market Is Currently Presenting an Opportunity to Strengthen Retirement Portfolio Resilienc... Read more

The Invisible Risk That Decides Your Retirement

Why how investors behave matters more than what markets do and what disciplined port... Read more

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more