Yen Breaks Away From Quiet Markets As Traders Race The Payroll Clock

The Japanese Yen remained the clear underperformer in otherwise subdued markets, with USD/JPY climbing to a fresh 40-year high as traders continued to exploit what they see as a narrowing intervention window ahead of Thursday’s US Non-Farm Payrolls report. While most major currency pairs remained confined within last week’s ranges, the Yen’s broad-based decline stood out as investors judged Tokyo unlikely to intervene before one of the year’s most important US economic releases.

Japanese officials offered little beyond familiar verbal warnings. Finance Minister Katsunobu Katayama reiterated that authorities stood “ready to take appropriate action,” while Chief Cabinet Secretary Yoshimasa Kihara repeated that “bold actions” remained an option in coordination with the United States. However, the restrained tone and lack of any escalation did little to deter speculative buying of USD/JPY. With the Ministry of Finance widely expected to avoid risking a costly intervention immediately before payrolls, market participants appear willing to test higher levels.

Elsewhere, the Dollar traded with a modestly firmer tone but lacked broad follow-through buying. US equity futures were little changed, while the benchmark 10-year Treasury yield hovered slightly below 4.4% as investors waited for fresh catalysts. Thursday’s payrolls report remains pivotal for determining whether the Federal Reserve is likely to begin a renewed tightening phase in September. Before then, Wednesday’s ADP employment report and ISM Manufacturing survey could influence expectations if they point to continued strength in the US economy.

The Australian Dollar underperformed Dollar, with the Reserve Bank of Australia’s meeting minutes failing to generate broader support. While the minutes maintained a clear tightening bias and left the possibility of an August rate hike open, markets increasingly view the RBA as adopting a wait-and-see approach rather than preparing to move imminently. Cooling domestic data and the sharp decline in oil prices have strengthened expectations that second-quarter inflation could moderate enough to justify another pause.

So far this week, the Yen has been the weakest major currency, followed by the Canadian Dollar and the Australian Dollar. The New Zealand Dollar has led gains, largely reflecting a rebound after last week’s heavy losses, with Sterling and the Euro also outperforming. The Dollar and Swiss Franc have traded closer to the middle of the performance table as broader markets remain in a holding pattern ahead of the week’s key macro events.

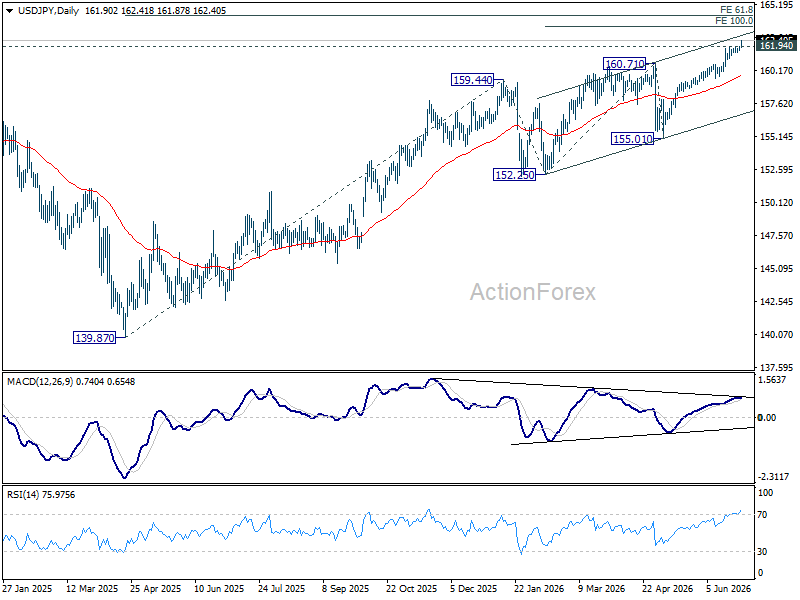

USD/JPY Daily Outlook

USD/JPY’s up trend resumed by breaking through 161.94 and intraday bias is back on the upside. Further rally should be seen to 100% projection of 152.25 to 160.71 from 155.01 at 163.47 next. On the downside, below 161.51 minor support will turn intraday bias neutral again first.

In the bigger picture, rise from 139.87 (2025 low) is seen as another rising leg of the long term up trend. Next target is 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. For now, outlook will remain bullish as long as 155.01 support holds, even in case of deep pullback.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more