Yen, Aussie Lead As Weak Dollar Faces Delayed NFP Test

Yen and Aussie are outperforming today as markets await the delayed US non-farm payroll report, while Dollar remains under pressure. Yen’s advance builds on momentum established after Japan’s election results. Investors believe Prime Minister Sanae Takaichi now has sufficient authority to pursue coherent fiscal strategy without accommodating a broad range of competing stimulus demands from oppositions.

Her pro-market approach is also expected to encourage renewed foreign participation in Japanese equities, strengthening capital inflow prospects. In that sense, Yen strength reflects both domestic political factors and external rate dynamics.

At the same time, Yen gains are being amplified by developments in US bond markets. US 10-year Treasury yields have fallen sharply this week and extended losses overnight, providing a clear tailwind for the currency through narrower yield differentials.

The precise catalyst for the yield decline remains debated. Yet, the technical setup points to scope for further downside in yields. That brings today’s NFP report into sharper focus. A weak print could push yields lower and accelerate downside in USD/JPY.

Meanwhile, Aussie strength reflects hawkish rhetoric from RBA Deputy Governor Andrew Hauser, who reiterated that inflation remains unacceptably high and pledged that policy will stay restrictive if needed. Hauser noted that renewed price pressures may reflect stronger demand meeting supply constraints, warning that persistent inflation cannot be tolerated. Markets now imply roughly a 70% probability of another hike to 4.10% in May, pending first-quarter inflation data.

For the week to date, Yen leads performance, followed by Aussie and Swiss franc. Dollar sits at the bottom of the pack, trailed by Sterling and Kiwi. Euro and Loonie are positioning in the middle.

In Asia, Japan was on holiday. Hong Kong HSI is up 0.30%. China Shanghai SSE is up 0.13%. Singapore Strait Times is up 0.39%. Overnight, DOW rose 0.10%. S&P 500 fell -0.33%. NASDAQ fell -0.59%. 10-year yield fell -0.051 to 4.147.

Low-bar NFP to set up yield-driven USD/JPY reaction

The delayed January US non-farm payroll report finally lands today, but expectations are already deeply tempered. Markets are braced for just 66k job growth, with unemployment seen holding at 4.4%. While hiring is seen slow, wage pressure is expected to remain firm. Average hourly earnings are forecast to rise 0.3% mom. Labor demand may be cooling, but without translating into meaningful disinflation pressure.

Meanwhile, officials from the US administration appeared keen to talk down expectations around job creation. National Economic Council Director Kevin Hassett said this week that tighter immigration enforcement and rapid productivity gains driven by artificial intelligence are suppressing demand for new workers. Those dynamics, he argued, could keep payroll growth low even as output remains strong.

Despite that, Hassett struck an upbeat tone, suggesting the economy could still deliver a powerful mix of lagging job creation alongside surging productivity, profits, and GDP. That framing implies that slower hiring should not automatically be read as economic stress.

Markets, however, are unlikely to to put too much attention on rhetoric. The more immediate focus remains on Treasuries. US 10-year yields have fallen sharply this week, extending losses after yesterday’s retail sales miss. The question now is whether bonds are genuinely front-running a more aggressive Fed easing path, or whether investors are simply reassessing “Sell America” narrative as overstated once hard data failed to confirm it. Today’s reaction to payrolls release could help resolve that ambiguity.

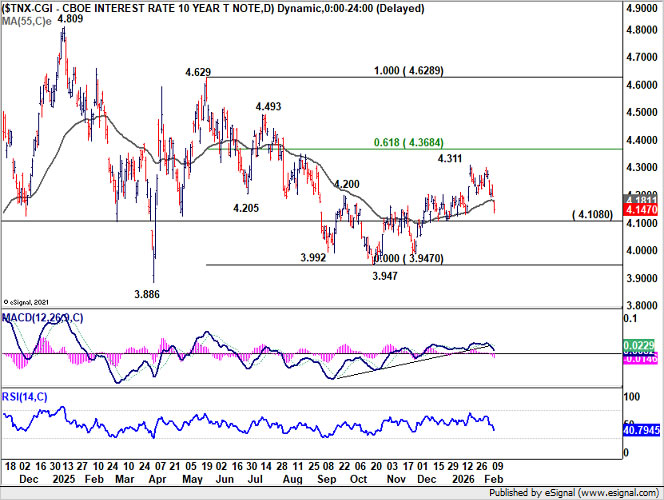

Technically, 10-year yield’s strong break below 55 D EMA suggests the rebound from the 3.947 low may already have completed at 4.311 as a corrective bounce. Decisive break below 4.108 support would solidify that view and reopen downside toward the 3.947 area.

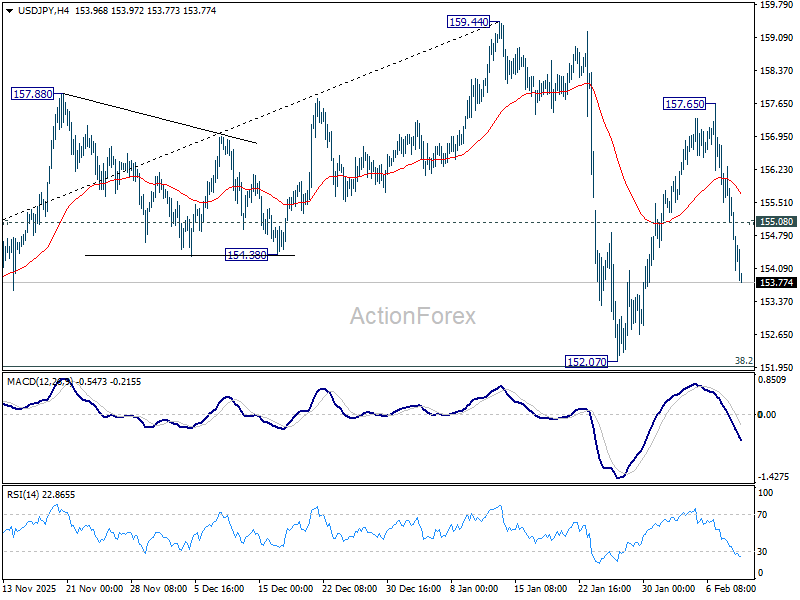

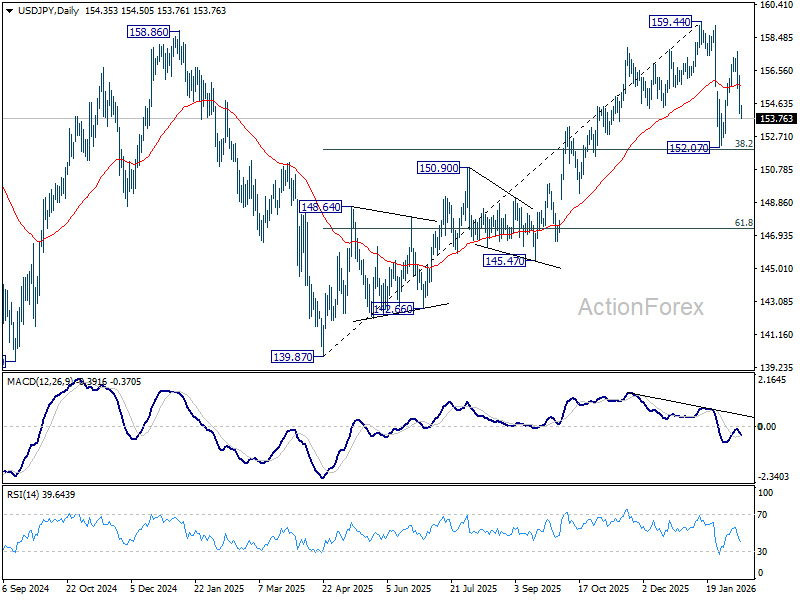

In the currency markets, the corresponding pair to watch is USD/JPY. The pair initially dives this week as reaction to Japan’s election results. But the last leg was clearly driven by the fall in US yields. Decline from 157.65 is seen as part of the corrective pattern from 159.44. While deeper fall could be seen to 152.07, strong support is expected from 38.2% retracement of 139.87 to 159.44 at 151.96 to bring rebound. However, decisive break of 151.96 would argue that USD/JPY is already in bearish trend reversal.

Fed’s Logan says inflation, not jobs, now bigger risk

Dallas Fed President Lorie Logan struck a cautious tone on further easing, arguing that downside risks to the US labor market “appear to have meaningfully dissipated” following last year’s three interest-rate cuts. Speaking overnight, Logan said those moves had helped stabilize employment conditions but had also introduced fresh risks on the inflation side.

While she expects inflation to make progress this year, Logan laid out a series of concerns that argue against complacency. She pointed to pending tariff effects, supportive fiscal policy, buoyant financial conditions, and the possibility that deregulation and new technologies could add to price pressures rather than dampen them.

Against that backdrop, Logan said she is “cautiously optimistic” that the Fed’s current policy stance can steer inflation back toward its 2% target without destabilizing the labor market. The next few months of data, she stressed, will be critical in determining whether that balance is being achieved.

For now, her bias is clearly toward holding steady. If inflation slows while the labor market weakens materially, further cuts could become appropriate. But as things stand, Logan said, “I am more worried about inflation remaining stubbornly high.”

Fed’s Hammack signals extended hold, favors patience

Cleveland Fed President Beth Hammack signalled little urgency to adjust policy, saying the Fed is in a good position to hold rates steady and let recent easing work through the economy. “we could be on hold for quite some time”, she added.

Hammack said she prefers to “err on the side of patience” rather than attempt to fine-tune the funds rate, noting that a steady policy stance would itself reflect a healthy economic backdrop. With rates close to a neutral level, she argued that holding steady allows policymakers to better judge how growth and inflation evolve.

She expects economic activity to pick up modestly this year, supported by easier financial conditions, recent interest rate reductions, and fiscal support, among other factors.” Labour market conditions also appear broadly stable. Hammack described current dynamics as “low-hire, low-fire,” with businesses reluctant to expand payrolls aggressively but also avoiding large-scale layoffs.

China CPI at 0.2% misses, but CNH breaks higher on Dollar weakness

The offshore Chinese yuan surged to its strongest level against Dollar in more than 33 months, with upside momentum showing signs of acceleration. However, the move has been driven far more by broad-based Dollar weakness than by any material improvement in China’s domestic fundamentals.

Today’s Chinese data continue to highlight persistent deflationary pressure. January inflation slowed sharply from a three-year high of 0.8% yoy to just 0.2%, undershooting expectations of 0.4% and reinforcing doubts that the economy has decisively turned the corner on pricing power. Underlying details offered little reassurance. Core CPI rose 0.8% from a year earlier, easing from 1.2% in December.

At the producer level, prices remained firmly in deflation, with PPI improving from -1.9% to -1.4% yoy, extending a factory-gate deflation streak that has now lasted more than three years.

Despite efforts to curb destructive price wars across industries plagued by overcapacity, excess supply continues to weigh on margins and pricing.

Policy signals offer little near-term support for the currency. The PBoC reiterated this week that it will maintain a moderately loose monetary stance, prioritizing growth support and gradual price recovery. That guidance reinforces the view that Yuan strength is unlikely to be domestic policy-driven.

Technically, the break below the medium-term falling channel floor suggests USD/CNH’s decline from the 2025 high at 7.4287 is entering a renewed acceleration phase. Near-term outlook remains bearish as long as 6.9956 resistance caps rebounds, with the next downside target seen at 138.2% projection of 7.4287 to 7.1608 from 7.2224 at 6.8522.

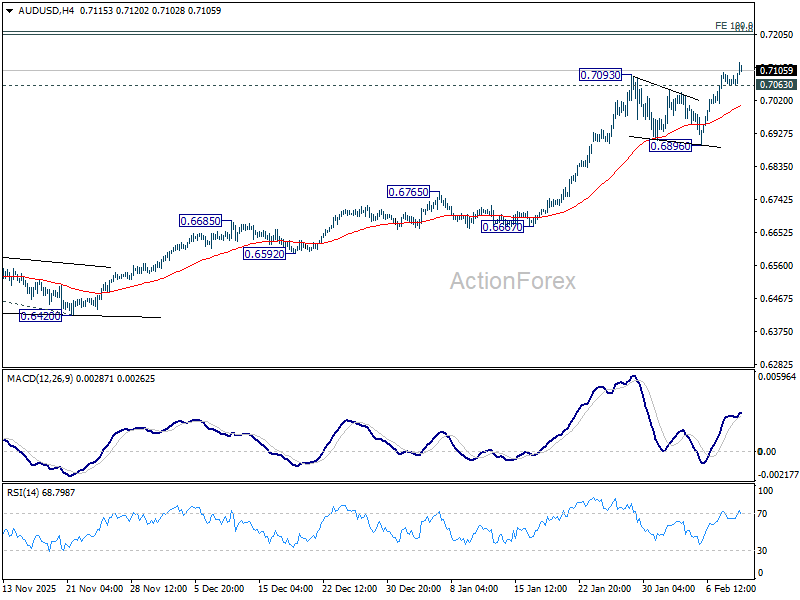

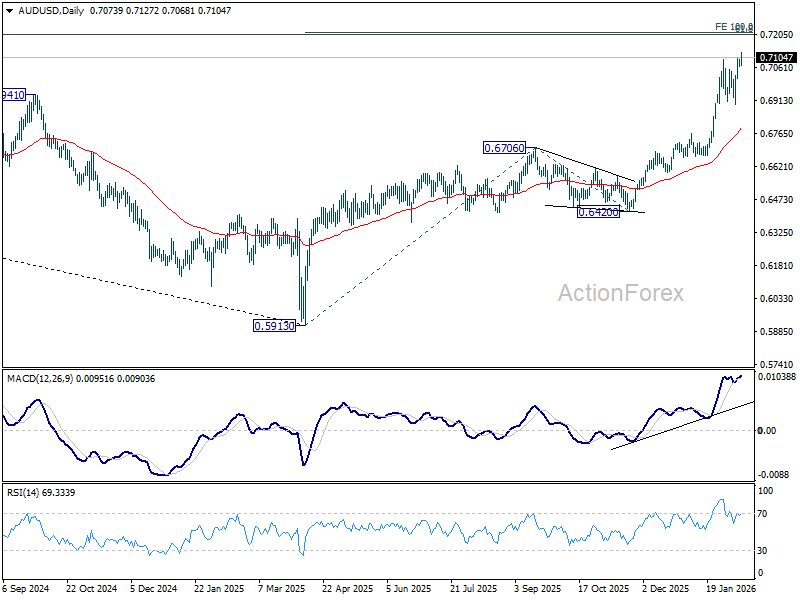

AUD/USD Daily Report

Daily Pivots: (S1) 0.7062; (P) 0.7079; (R1) 0.7093; More...

AUD/USD’s up trend resumed by breaking through 0.7093 resistance. Intraday bias is now on the upside for 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213. On the downside, below 0.7063 minor support will turn intraday bias neutral again. But retreat should be contained above 0.6896 support to bring another rally.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more