Wallers Shift Helps Dollar Recover From Early Losses

Dollar stabilized and recovered notably in early US trading after an initial selloff, supported by remarks from Fed Governor Christopher Waller. Waller, widely regarded as one of the more dovish voices on the Federal Reserve Board, signaled that the case for holding rates in March has strengthened following robust January employment data.

Waller was one of the two dovish dissenters at the January FOMC meeting. His openness to a March hold marks a shift in tone and suggests that the balance within the FOMC may be adjusting after the stronger-than-expected non-farm payroll report. The data appeared to reduce concerns over labor market deterioration, reshaping the near-term policy debate.

Admittedly, a March hold has long been the market’s base case, with probabilities already near fully priced. Waller’s comments did not dramatically alter immediate expectations. However, the symbolic importance of a prominent dove aligning with the hold narrative carries weight for forward guidance.

Indeed, markets have nudged up the probability of a June hold to around 50%, reflecting the view that easing may be delayed if labor conditions remain firm. Waller’s shift reinforces the perception that rate cuts are not imminent and that policy may remain restrictive longer than previously anticipated.

Meanwhile, global markets continue to weather US tariff uncertainty with relative composure. Major European indices are largely treading water, with only modest losses in Germany’s DAX. US equity futures are softer but far from disorderly.

In a social media post Monday, US President Donald Trump renewed criticism of the Supreme Court following its ruling against his tariff program. He vowed to pursue alternative trade authorities but offered no specifics. For now, markets appear to be waiting for clarity rather than reacting aggressively.

Currency performance reflects selective positioning rather than panic. Yen leads gains, followed by Sterling and Euro, while Dollar and Swiss Franc sit mid-pack. Australian Dollar is the weakest performer, trailed by Kiwi and Loonie, though moves remain measured.

In Europe, at the time of writing, FTSE is up 0.09%. DAX is down -0.54%. CAC is down -0.02%. UK 10-year yield is down -0.015 at 4.341. Germany 10-year yield is down -0.005 at 2.736. Earlier in Asia, Japan and China were on holidays. Hong Kong HSI rose 2.53%. Singapore Strait Times rose 0.47%.

Fed’s Waller: Strong payrolls could tilt his stance towards March hold

Fed Governor Christopher Waller said in a speech that recent economic data, particularly January’s employment report, came in “substantially stronger” than expected, suggesting labor market risks may have “diminished”. He noted that the initial estimate showed the US economy created more jobs in January than in the previous nine months combined, a development that surprised both policymakers and market participants.

Despite the upbeat signal, Waller cautioned that one strong month does not establish a trend. He emphasized that the Fed will receive additional employment and inflation data before the March 17–18 FOMC meeting, along with updates on job openings and retail sales. Only if February data confirm continued labor market strength alongside progress toward the 2% inflation target would his outlook turn “a bit more positive.”

In that scenario, Waller said his policy preference could “tilt toward a pause” at the upcoming meeting. However, he stressed the need for confirmation before adjusting his stance.

Addressing the recent Supreme Court ruling on tariffs, Waller downplayed its policy implications. He reiterated that tariffs tend to have only temporary effects on inflation and said he focuses on underlying price trends. Following traditional central bank practice, he intends to “look through” tariff-driven price moves, suggesting the ruling is unlikely to significantly alter his view on the appropriate stance of monetary policy.

BoE’s Taylor signals 2–3 cuts may be needed to reach neutral

Alan Taylor reinforced his dovish stance in remarks at a Deutsche Bank event in London today, arguing that inflation risks are shifting away from stickiness and toward undershooting the 2% target. He suggested weakening demand and softening labor market now pose greater downside risks to price pressures than previously feared.

While acknowledging that services CPI remains “slightly concerning” at around 4.4%, Taylor described the persistence as a temporary lag rather than a structural issue. He said the broader disinflation trend remains intact, even if services inflation has not cooled as quickly as hoped.

Pointing to what he called a “pessimistic outlook” for the UK job market, Taylor argued that policy remains too restrictive and justified a faster pace of easing. He sees scope for two to three additional rate cuts before the Bank Rate approaches a theoretical neutral level.

Germany Ifo improves to 88.6 in February, recovery signals emerge

Germany’s business sentiment improved in February, with the Ifo Institute Business Climate Index rising from 87.6 to 88.6, slightly above expectations of 88.4. Current Assessment Index climbed notably from 85.6 to 87.6, beating forecasts of 86.1. Expectations Index edged up from 89.6 to 90.5, in line with consensus.

Sector breakdown shows broad-based improvement. Manufacturing sentiment rose from -12.3 to -11.3, while services moved back into positive territory at 0.1 from -2.6. Construction also improved, narrowing losses from -14.3 to -11.5. Trade as the weakest component, slipping further to -21.8 from -21.1.

The institute noted companies were more satisfied with current conditions and increasingly optimistic about the outlook, describing the data as “first signs of recovery.” While levels remain subdued by historical standards, February’s improvement reinforces the view that Germany may be emerging from stagnation, offering cautious support to broader Eurozone growth expectations.

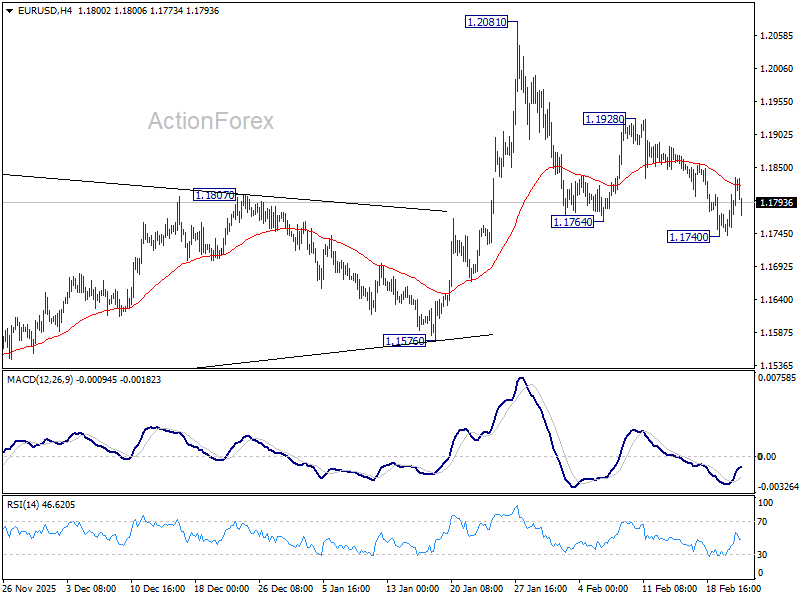

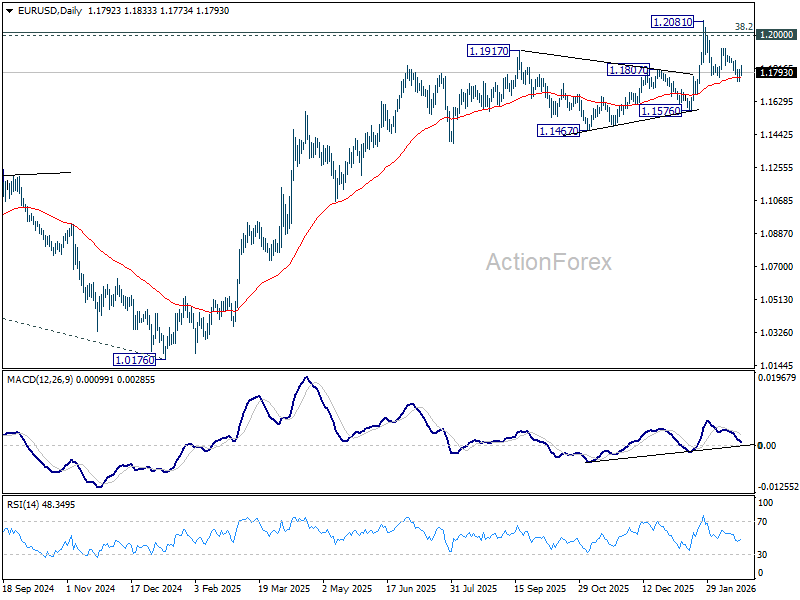

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1747; (P) 1.1778; (R1) 1.1811; More….

EUR/USD retreated mildly after hitting 55 4H EMA but stays above 1.1740 temporary low. Intraday bias stays neutral for the moment. Near term risk will remain on the downside as long as 1.1928 resistance holds. Below 1.1740 will target 1.1576 support next. Firm break there should confirm rejection by 1.2 key psychological level and turn near term outlook bearish.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more