Waiting Game: Markets Stall Ahead Of Fed Powells Finale

Despite the renewed surge in oil prices, there has been little shift in overall sentiment. Brent’s move higher would typically trigger a broader risk-off reaction, yet price action across asset classes remains contained. The lack of urgency suggests that traders are unwilling to commit ahead of today’s FOMC decision.

The Federal Reserve is widely expected to leave rates unchanged at 3.50–3.75%, but the real focus is on tone rather than action. This meeting is likely Jerome Powell’s final one as Chair, and expectations are firmly anchored around a “steady as she goes” message rather than any attempt to reshape the policy outlook.

There are also structural reasons why the meeting may deliver little. As an interim gathering without updated economic projections, it offers limited scope for meaningful guidance changes. Any adjustment to the Fed’s outlook is more likely to be deferred to June, when new forecasts are released. This reinforces the view that today’s meeting could turn out to be a non-event.

At the same time, the macro backdrop is becoming more complex. Oil prices have surged as the US–Iran conflict drags on, but the situation remains a stalemate rather than a breakdown. Markets are not yet pricing a return to full-scale conflict, which explains why the move in oil has not translated into broader panic.

This leaves markets in a delicate balance. On one hand, elevated oil prices are feeding into inflation concerns and supporting safe haven demand. On the other, the absence of escalation is preventing a more aggressive repricing of risk. As a result, traders are holding positions light and waiting for clearer signals.

In FX markets, Australian Dollar continues to stand out as the strongest performer for the week so far. The Q1 inflation report reinforced expectations for an RBA rate hike in May, effectively locking in near-term tightening. However, the softer-than-expected details have introduced uncertainty over the path beyond that move.

This nuance matters. While headline inflation surged, underlying pressures were more contained, suggesting that the RBA may not need to accelerate tightening after May. That has led to some pullback in Aussie, even as it retains a relative yield advantage.

Dollar is currently the second strongest currency, supported by the combination of higher oil prices and modest safe haven flows. However, without a clear escalation in geopolitics or a hawkish shift from the Fed, the move lacks strong momentum.

Canadian Dollar is also benefiting from the oil rally, but the domestic policy outlook is far more cautious. The Bank of Canada is widely expected to hold rates steady today, and many economists see little need for further tightening given ongoing weakness in parts of the economy.

Governor Tiff Macklem has already downplayed the significance of recent inflation expectations, viewing them as largely transitory as driven by external shocks. The focus remains on supporting growth, suggesting that policy will remain on hold even as oil prices rise.

At the other end of the spectrum, Swiss Franc is underperforming despite elevated geopolitical risks. Traditionally, CHF would attract inflows during periods of uncertainty, but this time the dominant driver is interest rate differentials rather than risk sentiment.

With oil prices rising, markets are increasingly expecting other central banks—particularly the ECB and BoE—to maintain or even strengthen their tightening bias to counter inflation pressures. By contrast, the Swiss National Bank is expected to stay on hold, with its primary concern still centered on preventing excessive Franc strength that could trigger deflationary forces.

Kiwi and Sterling are also underperforming, while Euro and Yen are trading in the middle of the pack.

Fed–Market Disconnect Takes Center Stage as Powell’s Final FOMC Faces Oil-Driven Inflation Test

The Fed sees inflation as temporary—but markets are not convinced. As oil prices surge again, Powell’s final FOMC faces a critical test between sticking to the script or signaling a policy shift. Read More.

Australia CPI Jumps to 4.6% as Fuel Surge Drives Headline Higher, Core Inflation Steady

Headline inflation is rising again in Australia, but stable core and easing services inflation suggest the shock remains concentrated rather than broad-based. Read More.

RBNZ’s Breman: Ready to Act Decisively If Inflation Persists

RBNZ’s Breman said if inflation persists, action will follow decisively. With fuel driving prices higher and core inflation still contained, policymakers are staying cautious but ready to tighten. Read More.

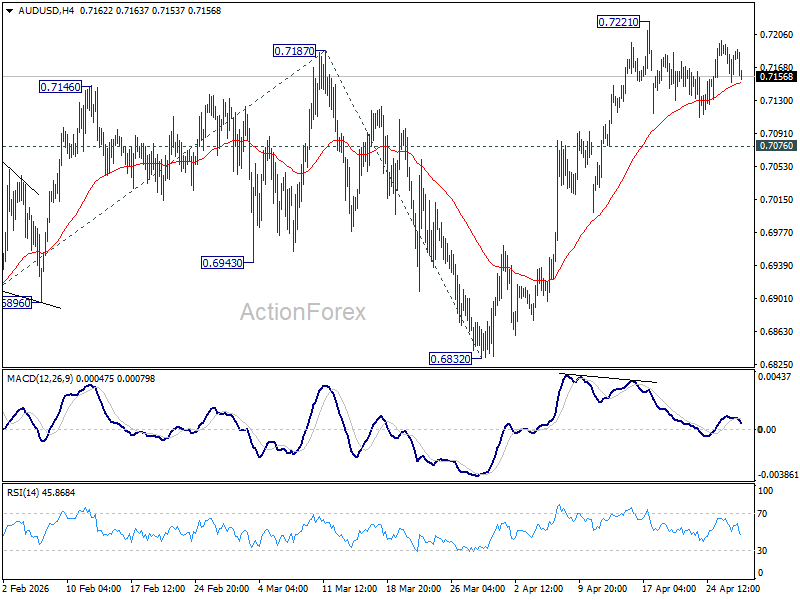

AUD/USD Daily Report

Daily Pivots: (S1) 0.7157; (P) 0.7176; (R1) 0.7202; More…

AUD/USD dips mildly today but stays in established range below 0.7221. Intraday bias remains neutral and more sideway trading could be seen. Further rise is expected as long as 0.7076 support holds. On the upside, firm break of 0.7221 will extend larger up trend to 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306. On the downside, break of 0.7076 minor support will turn bias back to the downside for deeper pullback.

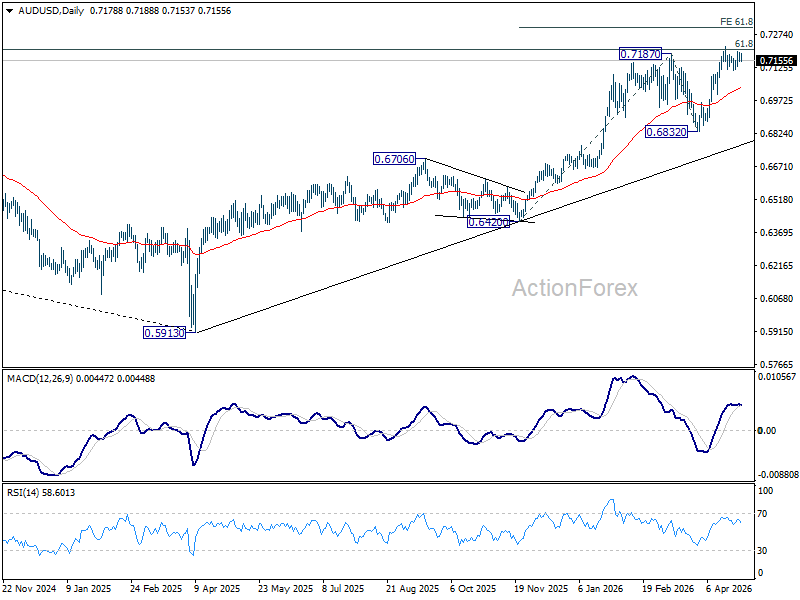

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it’s already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more