USD/JPY Nears 160 Red Line: Will Traders Or Japan Blink First?

USD/JPY is once again approaching the 160 level, putting markets on alert for potential Japanese intervention. The pair’s steady climb, driven by rising oil prices and widening rate differentials, is turning this level into a key flashpoint for global FX markets.

Yen’s weakness is not occurring in isolation. Oil prices have surged, with Brent breaking above $114 and WTI above $106, reinforcing inflation pressures globally. For Japan, a major energy importer, higher oil prices translate directly into currency weakness through deteriorating trade dynamics.

At the same time, higher energy costs are pushing yields up in major economies, widening the already significant rate gap with Japan. Even with the Bank of Japan’s recent hawkish shift, its policy rate remains far below global peers, leaving the Yen structurally disadvantaged.

This combination is driving USD/JPY higher toward the 160 threshold—a level widely seen as a “red line” for intervention. The key question now is whether markets will test that level aggressively or hesitate in anticipation of official action.

Japanese authorities have already stepped up rhetoric. Finance Minister Katayama warned again this week that the government is ready to take “bold action” against excessive currency moves. However, past experience shows that verbal intervention alone has limited impact without concrete follow-through.

The uncertainty lies in whether authorities will act decisively this time. Intervention at or near 160 could trigger a sharp reversal, particularly if markets are heavily positioned. But hesitation or delayed action could embolden traders to push the pair beyond the threshold.

Complicating the picture is the broader macro backdrop. Markets are currently in a holding pattern ahead of the FOMC decision, with traders reluctant to take strong positions. The Fed is widely expected to keep rates unchanged, and the lack of new projections suggests limited policy signals.

This has effectively delayed broader market reactions, including those to oil’s surge. Once the FOMC event risk is cleared, the focus could quickly shift back to yield differentials and oil-driven inflation pressures, reinforcing upward momentum in USD/JPY. In that scenario, the absence of intervention could accelerate gains.

For now, USD/JPY sits at a critical juncture. Whether it becomes a turning point or a launchpad for further gains will depend on a simple question—who blinks first: traders or Japan.

In the currency markets, for the week so far, Aussie is the strongest one, followed by Dollar, and then Loonie. Swiss Franc is the worst, followed by Kiwi, and then Yen. Euro and Sterling are positioning in the middle.

Fed–Market Disconnect Takes Center Stage as Powell’s Final FOMC Faces Oil-Driven Inflation Test

The Fed sees inflation as temporary—but markets are not convinced. As oil prices surge again, Powell’s final FOMC faces a critical test between sticking to the script or signaling a policy shift. Read More.

Eurozone Economic Sentiment Slumps as Confidence Drops Across Key Sectors

European sentiment is deteriorating fast. Consumer confidence is plunging, employment expectations are weakening, and growth outlook is turning softer across major economies. Read More.

Australia CPI Jumps to 4.6% as Fuel Surge Drives Headline Higher, Core Inflation Steady

Headline inflation is rising again in Australia, but stable core and easing services inflation suggest the shock remains concentrated rather than broad-based. Read More.

RBNZ’s Breman: Ready to Act Decisively If Inflation Persists

RBNZ’s Breman said if inflation persists, action will follow decisively. With fuel driving prices higher and core inflation still contained, policymakers are staying cautious but ready to tighten. Read More.

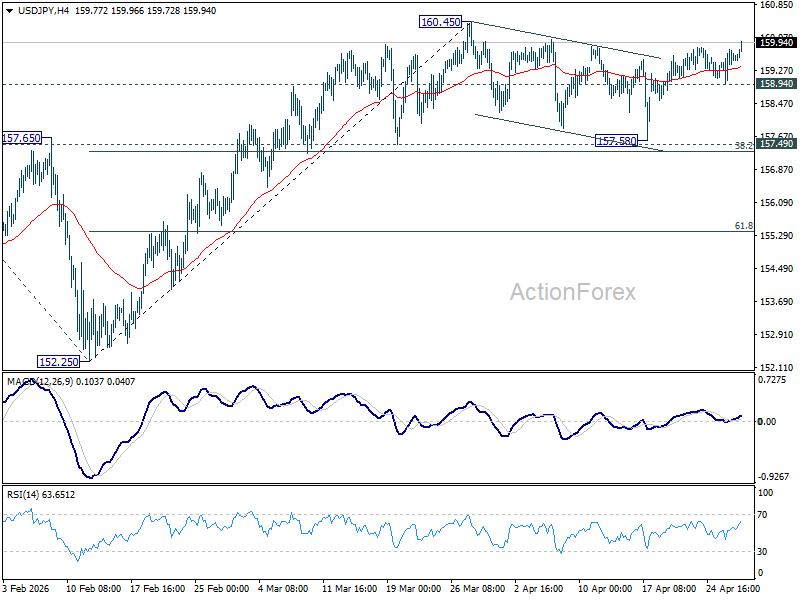

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.12; (P) 159.45; (R1) 159.95; More…

USD/JPY’s rally continues today and focus is now on 160.45 resistance. Firm break there will confirm larger rally resumption for 161.94 high next. On the downside, below 158.94 minor support will indicate that consolidation pattern from 160.45 is starting another down leg. But still, overall outlook will remain bullish as long as 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) holds. Upside breakout is just delayed in this case.

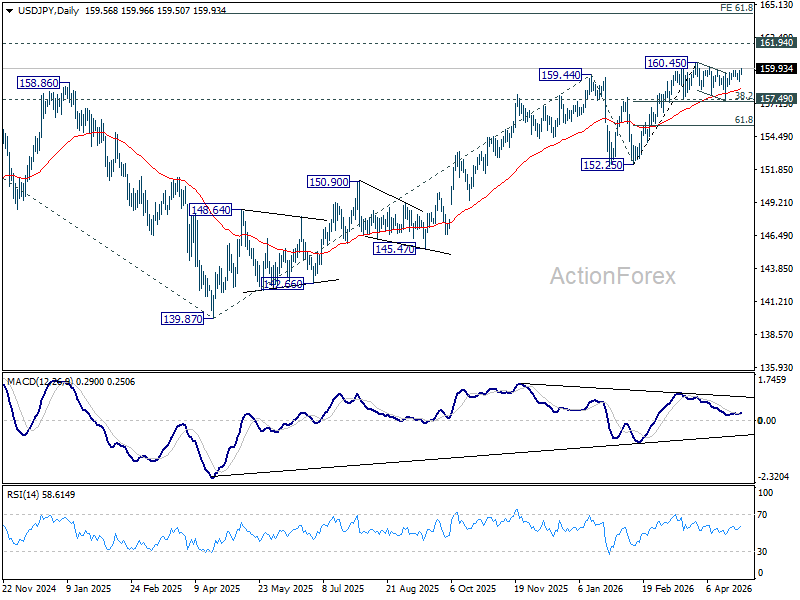

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 153.81) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more