UK Data Mixed, Dollar Awaits Delayed NFP For Direction

Sterling is steady in early European trading after UK labor data reinforced a familiar theme of softening employment alongside stubborn wage pressures. Job losses continued, while pay growth remained elevated. The data is unlikely to derail the BoE’s widely expected 25bps rate cut to 3.75% later this week.

While markets remain comfortable with the view that policy easing will continue into 2026, it’s highly uncertain on how much further the BoE can realistically go. Inflation has peaked lower than previously feared, but at 3.6% in October it remains well above target. With estimates of the UK neutral rate clustered around 3.25–3.75%, the scope for aggressive easing appears limited.

Even if the neutral rate proves slightly lower, there may only be room for one or two additional cuts unless inflation falls materially. That constraint is helping anchor Sterling and temper expectations for an extended easing cycle.

Attention now shifts decisively to the US, where markets await the delayed November employment report. The Bureau of Labor Statistics is due to publish the data on Tuesday following the 43-day government shutdown, alongside a partial update for October that will exclude the unemployment rate and several household-based measures.

Nonfarm payrolls are expected to have risen by around 50k in November, while October lacks a formal consensus estimate. One key wildcard is whether September’s 119k gain is revised lower, which would reopen concerns about a sharper deterioration in labor conditions after a weak summer.

With tariff-related inflation pressures proving far milder than worst-case scenarios, Fed officials have increasingly shifted their focus toward labor market health. A January FOMC hold remains the base case and is unlikely to be challenged barring an extreme surprise, but March remains finely balanced and could be swayed by today’s data.

On trade, US Customs and Border Protection reported that more than USD 200bn in tariffs have been collected this year under new duties imposed via over 40 executive orders. That comes as the Supreme Court weighs arguments over the legality of those tariffs, with potential refunds at stake.

In FX markets this week, Yen leads, followed by Euro and Dollar. Kiwi lags, trailed by Aussie and Sterling. Swiss Franc and Loonie sit mid-pack, reflecting a mild risk-off tone, but that could shift quickly on US jobs data.

In Asia, Nikkei fell -1.56%. Hong Kong HSI is down -1.58%. China Shanghai SSE fell -1.11%. Singapore Strait Times is down -0.10%. Japan 10-year JGB yield fell -0.002 to 1.957. Overnight, DOW fell -0.09%. S&P 500 fell -0.16%. NASDAQ fell -0.59%. 10-year yield fell -0.012 to 4.182.

UK payrolls decline deepens even as earnings stay elevated

UK labor market data for November pointed to further cooling in employment conditions. Payrolled employment fell by -38k on the month, a -0.1% mom. Annual drop widened to -171k, or 0.6% yoy. Annual payroll growth has now been negative every month since March.

Wage indicators showed clearer signs of easing at the margin. Median monthly pay growth slowed sharply to 2.7% yoy, down from 3.7% previously and less than half the pace seen in August. At the same time, the claimant count rose by 20.1k.

That said, broader earnings data remains elevated. In the three months to October, unemployment rate edged up from 5.0% to 5.1%. Average earnings growth surprised to the upside, rising 4.7% yoy including bonuses and 4.6% yoy excluding bonuses.

Japan’s PMI composite falls to 51.5, slowing momentum but manufacturing nears expansion

Japan’s December PMI data pointed to a modest cooling in overall momentum, while offering tentative signs of stabilization in manufacturing. PMI Manufacturing rose from 48.7 to 49.7. PMI Services eased from 53.2 to 52.5, while PMI Composite slipped from 52.0 to 51.5, indicating slower but still positive private-sector growth.

According to S&P Global, Japan’s private sector ended the year on a relatively strong footing, with output continuing to expand and new business rising further. Firms responded by stepping up hiring, with employment growth accelerating to its fastest pace in more than a year and a half. Growth remained concentrated in services, though the decline in manufacturing output and sales softened noticeable.

Forward-looking signals were more cautious. Business confidence weakened, particularly among manufacturers, reflecting subdued foreign demand and concerns about the outlook for 2026. At the same time, cost pressures intensified, with input prices rising at the fastest pace since April. Firms responded by raising output charges “at a solid pace”.

Australia PM composite falls to 51.1, growth cooling but persistent price pressures

Australia’s PMI readings for December pointed to moderating growth momentum toward year-end. PMI Manufacturing rose from 51.6 to 52.2, signaling a stronger expansion in factory activity. PMI Services slipped from 52.8 to 51.0. As a result, PMI Composite eased from 52.6 to 51.1, the lowest level in seven months.

The slowdown in overall activity was accompanied by more encouraging details beneath the surface. According to S&P Global, new orders continued to rise at a solid pace, while business confidence improved in December. Employment growth also remained robust, with job creation sustained at faster rates across both manufacturing and services, suggesting firms remain confident enough in demand to continue hiring.

Inflation signals, however, firmed again. Cost pressures intensified for Australian businesses, prompting companies to raise output prices more quickly in an effort to “defend their margins”. As a result, output price inflation returned to its long-run average after two months of subdued increases.

Australia Westpac consumer sentiment falls back to 94.5, bounce proves short-lived

Australian consumer confidence fell sharply in December, reversing November’s brief improvement. The Westpac Consumer Sentiment Index dropped -9.0% mom to 94.5, slipping back toward levels seen prior to last month’s surprise bounce. The pullback leaves sentiment only in “cautiously pessimistic” territory as the year comes to a close.

Westpac noted that while confidence has improved meaningfully from the deep and prolonged pessimism that dominated much of 2024, households remain reluctant to shift into outright optimism. The November rebound marked the first net positive reading since the economy reopened after the pandemic, but the latest data suggests that underlying confidence remains fragile and easily unsettled.

The survey reinforces a cautious backdrop for the RBA ahead of its February 2–3 meeting. While inflation has picked up recently, there are few signs that tight labor markets or strong consumer demand are driving the move. Instead, administered prices outside the reach of monetary policy have been a key factor. As those pressures fade, inflation is expected to resume its path toward the midpoint of the target range, though policymakers have warned that if normalization proves slow, rates may need to stay on hold for longer, with hikes still a live contingency.

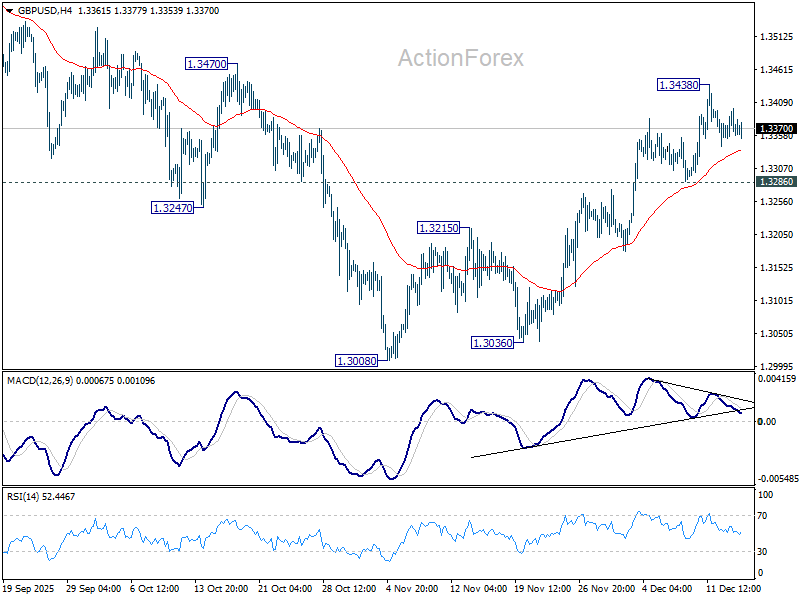

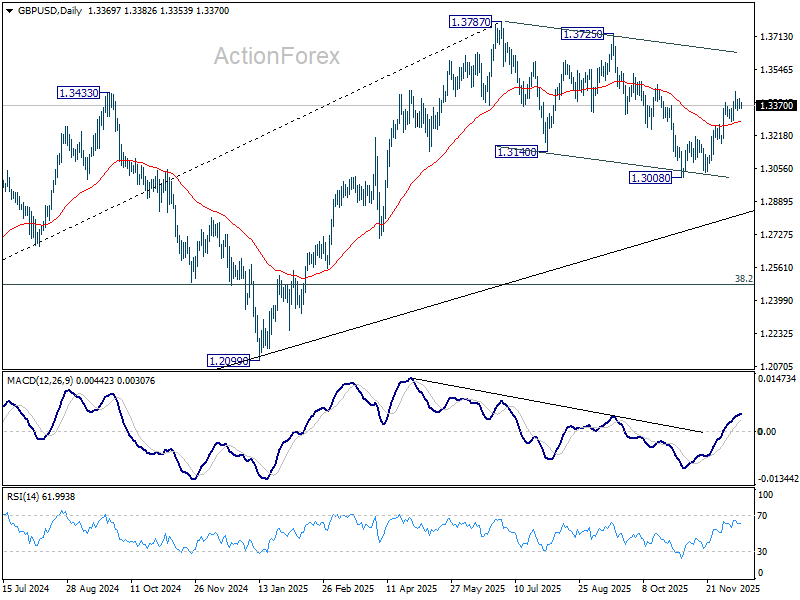

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3354; (P) 1.3378; (R1) 1.3401; More…

Intraday bias in GBP/USD remains neutral as consolidations continue below 1.3438. With 1.3286 support intact, further rally is expected. As noted before, fall from 1.3787 should have completed as a three-wave correction to 1.3008. Above 1.3428 and firm break of 1.3470 resistance will pave the way back to retest 1.3787 high. However, sustained break of 1.3286 support will mix up the near term outlook.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more