Trade War Shock Roils Markets In A Politically Charged Week

It was a week dominated by politics — both domestic and international — as shifting power dynamics and fresh policy risks rippled through global markets. In Japan, optimism surged after Sanae Takaichi’s victory in the ruling LDP leadership race, clearing the way for her to become the country’s first female prime minister. Investors welcomed her Abenomics-style agenda of fiscal stimulus and pro-growth policies, propelling the Nikkei to record highs. At same time, Yen plunged sharply, prompting verbal intervention from officials worried about “one-sided” market moves.

Takaichi’s early momentum was tested as the LDP’s long-time coalition partner, Komeito, abruptly withdrew support after failed negotiations, citing unresolved issues over a political funding scandal. Still, Komeito’s move should be seen as a tactical standoff rather than a lasting rupture. Given the backing for Takaichi from senior LDP figures such as former Prime Minister Taro Aso, the expectation remains that she will secure parliamentary approval later this month.

Across Europe, France’s political crisis deepened. President Emmanuel Macron reappointed Sébastien Lecornu as prime minister—just days after his resignation—hoping the loyalist can rally enough support to pass a 2026 budget through a fractured legislature. Markets remain skeptical, however: another failure could trigger snap elections, heightening fiscal uncertainty and weighing on the Euro.

Meanwhile in the Middle East, the long-awaited ceasefire in Gaza was finally implemented after Israel approved the first phase of a peace deal involving the withdrawal of troops and a hostage-prisoner exchange. The agreement sent WTI crude below 60, its lowest since May, as geopolitical risk premiums unwound.

Yet all of these developments were ultimately overshadowed by a late-week shock from Washington. US President Donald Trump reignited the U.S.–China trade war, announcing plans for 100% tariffs on all Chinese imports starting Nov 1 and threatening to impose sweeping export controls. The escalation triggered a sharp sell-off in U.S. equities and a flight into Treasuries, erasing weeks of calm.

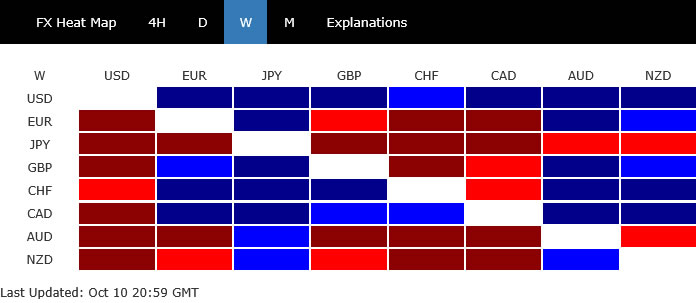

By week’s end, Dollar reigned as the strongest major currency, followed by the Loonie—lifted by robust Canadian jobs data, and Swiss Franc. At the bottom, Yen’s collapse left it the weakest performer, though the worst may be over after recent intervention talk, and risk-off bounce. Aussie and Kiwi lagged amid risk aversion, while Euro and Sterling held mid-table.

Trump’s 100% Tariff Threat Reignites Full-Scale US–China Trade War Fears

The week’s closing hours were dominated by sharp escalation in U.S.–China tensions. In a surprise announcement late Friday, Trump said the U.S. will impose 100% tariffs on all Chinese imports starting November 1, “over and above any tariff that they are currently paying.” Trump further declared that export controls will be applied on “any and all critical software” from the same date, signaling a widening scope of decoupling beyond physical goods.

The move marks a return to hardline trade policy, undoing months of tentative diplomatic progress and rattling financial markets already uneasy over the ongoing U.S. government shutdown.

The escalation came after Beijing introduced new controls on rare earth exports earlier in the week, requiring foreign entities to obtain licenses to export goods containing even trace amounts of strategic minerals. Trump accused China of holding the world “captive” through its dominance in these materials and said the U.S. would no longer tolerate this economic blackmail.

The shift was abrupt. Earlier in the week, Trump had been expected to meet Chinese President Xi Jinping at the upcoming APEC summit in South Korea, but he later suggested the meeting would be canceled. The announcement effectively swept away expectations for a trade deal, sparking heavy risk aversion across global markets.

Wall Street responded violently. The DOW dropped nearly 2%, the S&P 500 lost 2.7%, and the NASDAQ plunged 3.6%—its steepest decline since early summer. Treasury yields tumbled as investors rushed into safe-haven assets, with the 10-year yield breaking below 4.1%.

The renewed confrontation came against a backdrop of growing domestic dysfunction. The U.S. government shutdown, now stretching into its 10th day, showed no signs of resolution after repeated failed Senate votes. Reports that federal worker layoffs had begun added to investor unease about near-term economic disruption.

By the week’s end, markets were again on full alert: the risk of a full-blown trade and fiscal crisis is now back on the table, and its impact will likely dictate global market direction in the days ahead

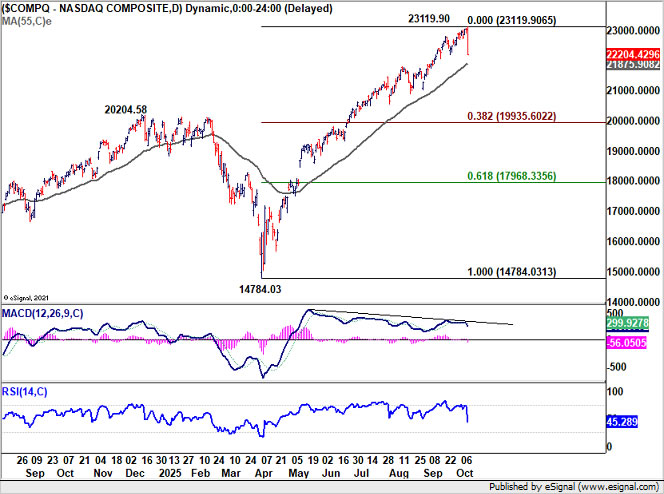

NASDAQ Hit Hard by Tariff Shock, 55-Day EMA Crucial to Keeping Uptrend Intact

NASDAQ’s record-setting rally came to an abrupt pause on Friday as the index tumbled -3.56% from its all-time high of 23,119.90, hit earlier in the session. While the magnitude of the drop was striking, the broader structure remains bullish—no decisive break of key trend levels has occurred yet.

For now, 55 D EMA at 21,875.90 serves as the immediate line of defense. Strong bounce from that region would preserve the index’s near term bullishness, suggesting that Friday’s selloff was a temporary reaction to geopolitical shocks rather than the start of a prolonged downturn.

However, considering bearish divergence condition in D MACD, sustained break of 55 D EMA will indicate that a medium term top has already formed. Fall from 23,119.90 would then be seen as correcting whole rise from 14,784.03. Deeper decline would be seen back to 20k psychological level, which is close to both 20,204.58 resistance turned support and 38.2% retracement of 14,784.03 to 23,119.90 at 19,935.60.

U.S. 10-Year Yield Slides as Safe-Haven Demand Surges

The recovery in U.S. 10-year yields proved short-lived, with the benchmark ending the week sharply lower at 4.051, as investors rushed back into bonds amid renewed trade tensions and equity market turbulence. The move erased nearly all of last week’s recovery and reaffirmed that the downtrend remains firmly intact.

Technically, the yield continues to trade well below falling 55 D EMA (now at 4.186%) and comfortably within the descending channel that has guided the decline since May. Further fall should be seen to retest 3.992 low first, and break there will target 61.8% projection of 4.493 to 3.992 from 4.200 at 3.891 next.

Dollar Index Extends Rebound as EUR/USD Struggles Below 1.20 Barrier

Dollar Index extended the rebound from 96.21 last week, climbing to 98.97. Technically, current rise is still viewed as correcting the five wave decline from 110.17 (2025 high). As long as support holds at 97.47, further upside is expected toward 100.25 resistance and possibly above.

Though, significant hurdles remain higher up at 38.2% retracement of 110.17 to 96.21 at 101.54. Strong resistance could emerge there to limit upside to complete the corrective bounce.

However, it should be emphasized that Dollar Index continues to draw background support from its long-term rising trend channel that defines the multi-decade rise from 2008 low at 70.69. Hence, it cannot be ruled out that Dollar Index is at the onset of medium-term bullish reversal.

The strength of the current rally in Dollar Index would ultimately depending on whether EUR/USD’s current rejection by 1.2000 psychological level will turn into a medium term bearish trend reversal, or just a corrective pullback.

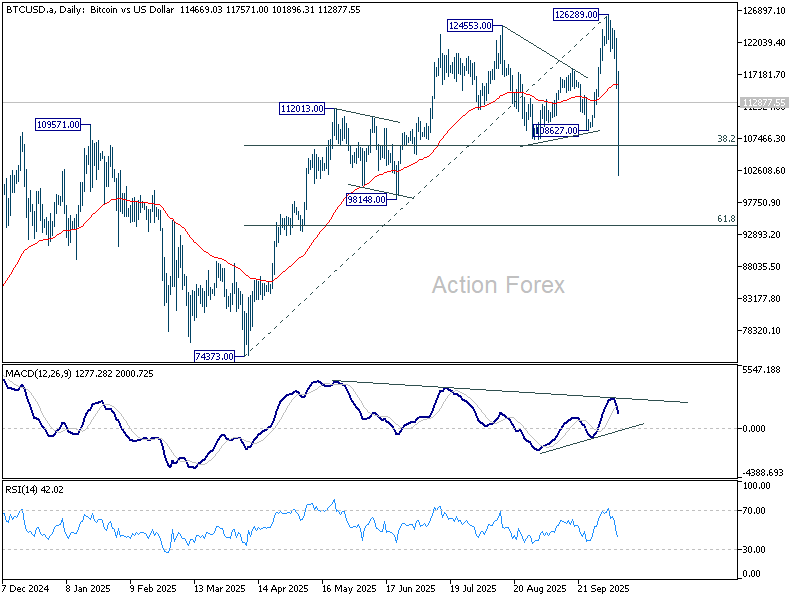

Bitcoin Hit Hard, 100K Level Becomes Crucial Battle Line

The late development also sparked violent moves in the cryptocurrencies markets. Bitcoin was no exception. Bitcoin extended the plunge from its recent record high of 126,289 to as low as 101,896, before stabilizing into the weekend.

So far, the selloff is seen as a correction within to the broader five-wave uptrend that started from 74,373 (March low). There should be some support around 100k psychological level to contain downside to set the range for consolidations.

However, it should be emphasized that sustained break of 55 W EMA (now at 96831) will argue that Bitcoin is indeed correcting the whole up trend from 15452 (2022 low). In this bearish case, Bitcoin could dive further to 74373 support before finding a bottom.

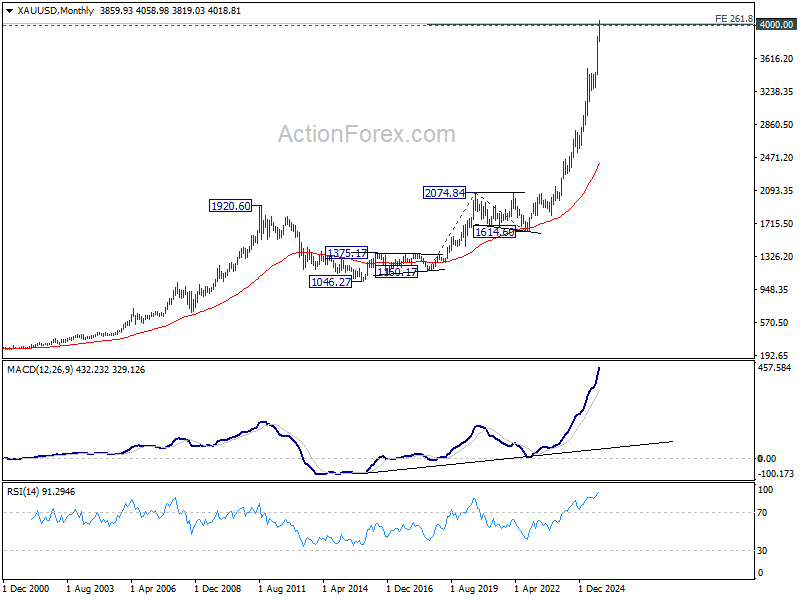

Gold Pauses at 4000 in Calm Despite Heightened Market Turmoil

Gold’s record-breaking surge above 4,000 has given way to a quieter tone, with the precious metal showing little reaction to Friday’s sharp risk-off wave. The lack of follow-through suggests that bids may have run its course, at least temporarily, as traders lock in profits.

Technically, Gold has met a major target zone, reaching 261.8% projection of 1160.17 to 2074.84 from 1614.60 at 4009.20. The rally’s parabolic nature leaves it vulnerable to profit-taking, and the immediate focus now turns to 3819.03, where a break would confirm that a short-term top is in place. Deeper pullback could then follow toward 55 D EMA (now at 3625.49).

Another brief extension higher cannot be totally ruled out. But stiff resistance is expected below 100% projection of 2584.24 to 3499.79 from 3267.90 at 4183.45 to limit upside and bring the overdue correction.

Focus will remain emergence of topping signals ahead.

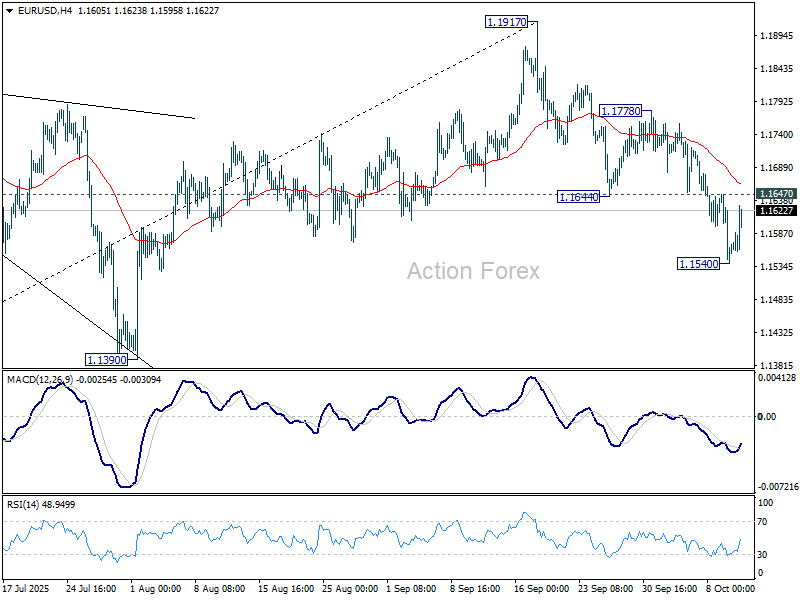

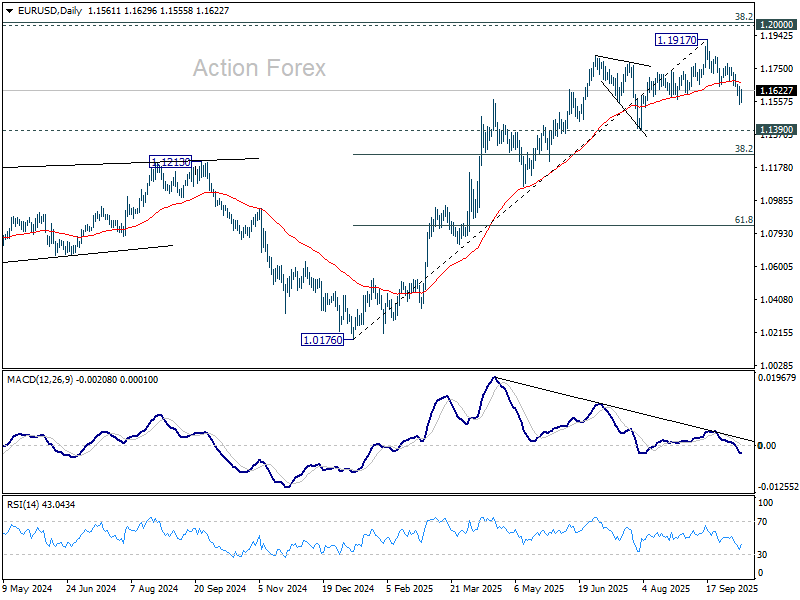

EUR/USD’s fall from 1.1917 resumed last week, but recovered after hitting 1.1540. Initial bias is turned neutral this week for consolidations. Deeper decline is expected as long as 1.1778 resistance holds. Below 1.1540 will target 1.1390 support or further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1247) holds, the up trend from 0.9534 (2022 low) is still extended to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

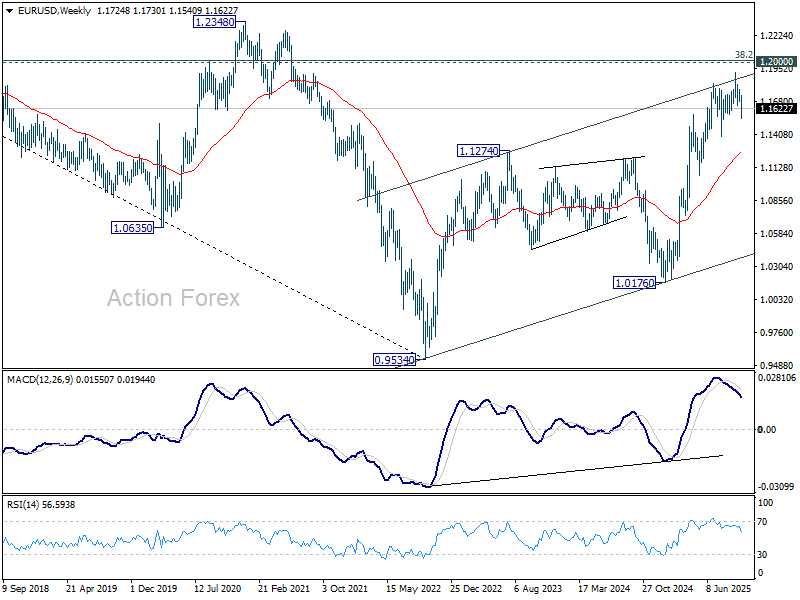

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more