Subdued Currency Movements, Cautious Stocks, Range Trading Gold

Mild risk-off mood is seen in the global financial markets today, starting from the the noticeable retreat in Japan’s Nikkei, then the marginal declines across European stock indices, alongside soft US futures. However, this sense of caution has not significantly rippled through the currency markets, where activity remains largely subdued. Notably, most major currency pairs and crosses have maintained tight ranges, except for a few Sterling crosses which have shown more activity.

British Pound is currently the stronger one, alongside Australian Dollar and New Zealand Dollar, Conversely, Swiss Franc, Dollar, and Japanese Yen are registering softer performances. This paints a picture typically associated with risk-on market behavior, rather than risk-off. Euro and Canadian Dollar find themselves positioned in the the middle. Market activity is expected to remain muted throughout the session, particularly given the sparse US economic calendar.

Technically, a short term top has likely formed at 2222.66 in Gold, with D MACD crossed below signal line. Some consolidations would be seen first. But downside should be contained by 38.2% retracement of 1984.05 to 2222.66 at 2131.51 to bring another rally. Above 2222.66 will resume the long term up trend to 100% projection of 1614.60 to 2062.95 from 1810.26 at 2259.15. However, sustained break of 2131.51 fibonacci support will bring deeper pull back to 55 D EMA (now at 2085.37).

In Europe at the time of writing, FTSE is down -0.42%. DAX is up 0.02%. CAC is down -0.38%. UK 10-year yield is down -0.0747 at 3.962. Germany 10-year yield is up 0.025 at 2.350. Earlier in Asia, Nikkei fell -1.16%. Hong Kong HSI fell -0.16%. China Shanghai SSE fell -0.71%. Singapore Strait Times fell -0.62%. Japan 10-year JGB yield fell -0.0078 to 0.736.

ECB’s Lane confident that wages growth is on track to normalize

ECB Chief Economist Philip Lane, in a podcast published today, conveyed a sense of confidence among policymakers regarding wage growth trends. Lane articulated that policymakers are “confident” that wages growth is “on track” to return to normal.

“If this assessment is confirmed, then we will start looking more closely at reversing some of the rate increases we’ve made,” he added.

Adding to the conversation, Governing Council member Fabio Panetta addressed an audience at a separate event, underscoring the feasibility of a rate cut given the current inflation trend.

“The consensus emerging – especially in recent weeks – within the ECB governing council points in this direction,” Panetta noted.

BoJ Jan minutes: No need for aggressive tightening like Western counterparts

BoJ’s minutes from January meeting, ahead of the landmark March decision to end negative interest rates, reveal a cautious approach towards monetary policy adjustments. Members highlighted the Japan’s economic conditions “differed significantly” to those of US and Europe when they initiated interest rate hikes a few years ago. The consensus was clear: it was “not required in Japan to conduct rapid monetary tightening” as seen in Western economies.

Further discussions underscored three primary risks to Japan’s economic activity: shifts in global economic performance and financial markets, fluctuations in commodity and grain import prices, and future growth expectations of firms and households.

Members agreed these factors could significantly influence economic outcomes and emphasized the need for vigilance towards price-setting behaviors within the economy, as well as the impact of currency and commodity price movements on domestic inflation.

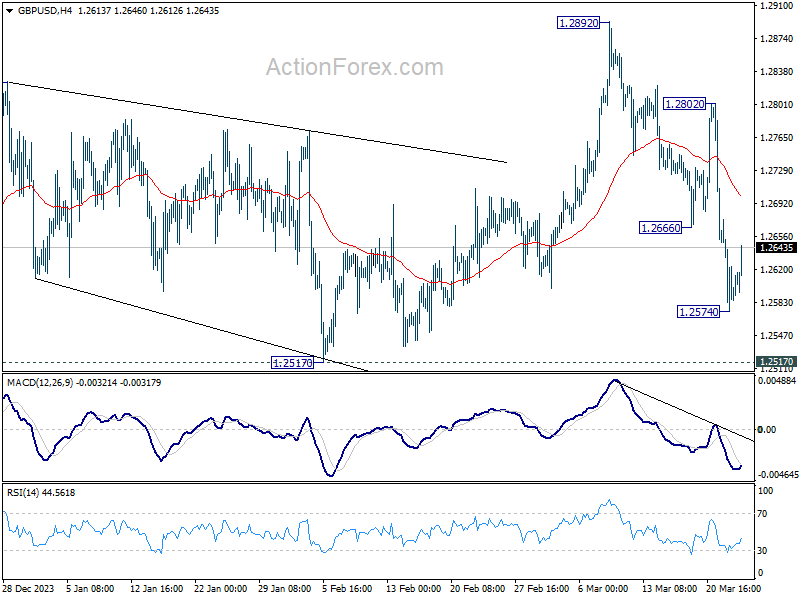

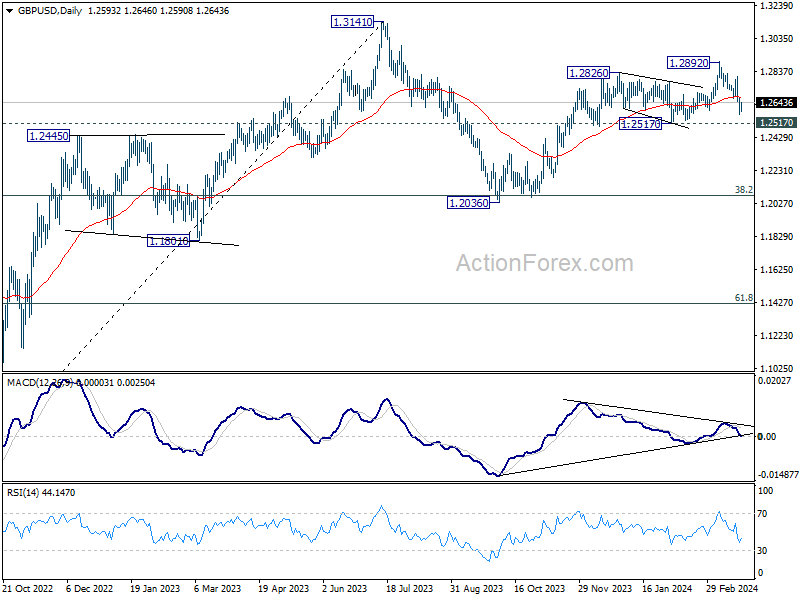

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2558; (P) 1.2617; (R1) 1.2658; More…

Intraday bias in GBP/USD is turned neutral with current recovery and some consolidations would be seen first. But risk will stay on the downside as long as 55 4H EMA (now at 1.2700) holds. Below 1.2574 will resume the fall from 1.2892 to 1.2517 structural support first. Decisive break there will suggest that rise from 1.2036 has completed at 1.2892 already, and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which might still be in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | ||||

| 14:00 | USD | New Home Sales Feb | 675K | 661K |

When The Wave Turns

Why Retirement Investing Is Moving Towards Resilience Jeremy Grantham’s latest market warnings have revived an old tru... Read more

Gyrostat Capital Management: July Retirement Portfolio Resilience Assessment

The Market Is Currently Presenting an Opportunity to Strengthen Retirement Portfolio Resilienc... Read more

The Invisible Risk That Decides Your Retirement

Why how investors behave matters more than what markets do and what disciplined port... Read more

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more