Sterling Takes A Hard Hit Following CPI; FOMC Dot Plot Awaited

Sterling finds itself under tremendous selling pressure following release of lower-than-anticipated headline and core CPI readings from the UK. This development is seen as a favorable turn of events for BoE policymakers, solidifying the anticipation that the rate hike expected to be announced tomorrow may be the last in the current cycle.

On the heels of the Pound, Canadian Dollar emerged as the second weakest, failing to sustain the momentum gained from yesterday’s surge, which was propelled by robust Canadian inflation data. Meanwhile, Yen trails closely as the third weakest, with traders maintaining a cautious stance in the lead-up to BoJ decision slated for Friday. In contrast, Dollar, Euro, Swiss Franc, and Australian Dollar are exhibiting stability, with their trading ranges tightly bound against one another.

Market attention is shifting towards Fed’s rate decision due later today. The new economic projections and the dot plot are expected to be the focal points of this announcement, giving investors critical insights into Fed policymakers’ perspective on economic conditions and potential policy actions. Moreover, there has been a notable surge in US Treasury yields on the long end overnight, signalling the potential for further rallies should there be any hawkish surprises from Fed today.

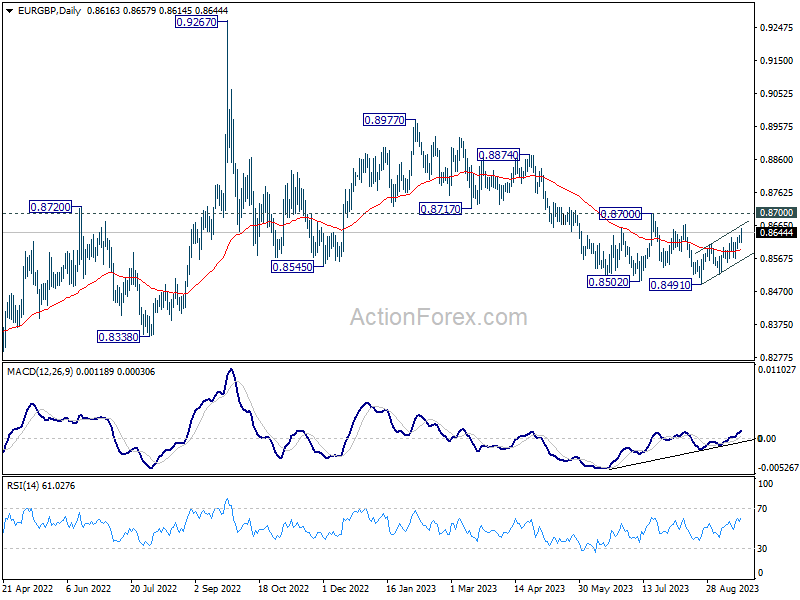

From a technical standpoint, Sterling’s downturn today does not spell disaster yet. Despite the day’s rally, EUR/GBP is still capped well below near-term resistance of 0.8700, maintaining neutral outlook at best for now. However, decisive break of 0.8700 will be a strong sign of medium bullish reversal, which would set up rally back towards 0.8977 resistance later in the rest of the year. BoE’s decision tomorrow stands as a pivotal moment in determining the forthcoming trends.

In Asia, Nikkei closed down -0.66%. Hong Kong HSI is down -0.51%. China Shanghai SSE is down -0.51%. Singapore Strait Times is down -0.10%. Japan 10-year JGB yield rose 0.0054 to 0.724. Overnight, DOW dropped -0.31%. S&P 500 dropped -0.22%. NASDAQ dropped -0.23%. 10-year yield rose 0.046 to 4.365.

UK CPI slowed to 6.7%, BoE’s hike tomorrow could be the last

Sterling is facing headwinds after release of UK’s CPI inflation data, which came in lower than market forecasts. This development strengthens the speculation that BoE might be drawing curtains on its tightening cycle, with the one more hike expected tomorrow potentially being the concluding move.

The reported data illustrated deceleration in CPI from of 6.8% yoy to 6.7% yoy in August, a result that fell short of the projected escalation to 7.1% yoy. This is the lowest rate witnessed since February 2022.

A deeper dive into the components reveals that this softening of annual CPI into August 2023 emerged from six out of the 12 sectors. Notably, restaurants and hotels, along with food and non-alcoholic beverages, played a pivotal role in pulling down the numbers. However, the motor fuels category within the transport sector exerted upward pressure, somewhat counterbalancing the decline.

Furthermore, core CPI, which is calculated by excluding variables such as energy, food, alcohol, and tobacco, followed suit, decelerating from 6.9% yoy to 6.2% yoy. This stands significantly below anticipated rate of 6.8% yoy.

Breaking it down further, while CPI goods noted a slight acceleration from 6.1% yoy to 6.3% yoy, CPI services delineated a slowdown from 7.4% yoy to 6.8% yoy.

For the month. CPI rose 0.3% mom, below expectation of 0.7% mom.

Japan’s exports to China tumble further, trade with US flourishes

Japan’s economic data shows a dwindling momentum in the country’s export sector, registering a decline of -0.8% yoy to JPY 7994B in August, with a particularly notable decrease in its trading activities with China.

The continued dip in exports is largely attributed to diminishing overseas demand and the trade restrictions imposed by China, which have significantly impacted Japan’s trade balance.

A striking example is seen in the sharp -11.0% yoy decline in exports to China, to a total of JPY 1.44T. This downturn marks the third consecutive month of double-digit drops in export activities to China, severely affected by the -41.2% yoy plunge in food exports due to China’s ban on Japanese seafood.

However, a beacon of positivity trading rapport with US, which saw a growth spurt of 5.1% yoy, aggregating to a record JPY 1.62T for the month of August. This surge has been primarily fueled by a heightened demand for Japanese cars, mining, and construction machinery.

On the import front, Japan noted a considerable -17.8% yoy reduction to JPY 8925B, with imports from China dipping -12.1% to JPY 1.93T, and those from US falling -9.5% yoy to JPY 967.39B. The nation’s trade balance has consequently been reported at a deficit of JPY -930.5B.

When analyzed in seasonally adjusted terms, both exports and imports showcase a month-on-month decrease, registering -1.7% mom to JPY 8267.8B and -2.1% mom to JPY 8823.6B, respectively. Thankfully, there is a silver lining as the trade deficit has slightly narrowed compared to the previous month, standing at JPY -555.7B.

Australia Westpac leading index edged up to -0.5%, growth struggles despite population boom

Westpac Leading Index for Australia indicates that the nation’s growth outlook remains subdued. The index inched up marginally from -0.56% to -0.50% in August, marking a year since it began registering negative readings. These figures suggest that the prospect of per capita GDP advancing in the coming 3–9 months appears bleak.

Westpac’s forecasts for the next year resonate with the index’s gloomy narrative, anticipating an economic growth of less than 1% for the year leading up to June 2024. Interestingly, there’s a potential silver lining: with predictions pointing to population growth surpassing 2% in 2023, this could introduce some upside risks to the otherwise somber economic projections.

However, despite this population surge, the economy is projected to trail behind, as evident from the March and June quarter results. Both quarters witnessed a contraction of -0.3% in GDP per capita, a pattern that’s predicted to persist in the forthcoming year.

Regarding next RBA rate decision on October 3, Westpac said it’s “almost certain to hold rates steady for another month”. The crucial data for the next move would be September quarter inflation report, which will not be available until the November RBA meeting.

BoC Kozicki speaks on recent swings in inflation

BoC Deputy Governor Sharon Kozicki acknowledged in a speech that CPI inflation has seen “ups and downs of the size we’ve seen in the past couple of months,” highlighting a decrease from a high of 8.1% in June 2022 to 2.8% in June this year. However, this decrease was followed by a surge to 3.3% in July and 4.0% in August (as released yesterday). Despite this decrease and subsequent rise, she affirmed that such fluctuations are “not that unusual.”

She emphasized the Bank’s approach to monitoring inflation, which includes a focus on measures of core inflation that exclude more volatile price movement components to get a true sense of underlying inflation.

“Measures of core inflation have eased,” she noted, yet underlined that “inflationary pressures are still broad-based.” She continued to express concern over the number of CPI components with price increases exceeding 5%, which, despite being lower than before, remains “much higher than it usually is when inflation is stable and close to 2%.”

Acknowledging that “underlying inflation is still well above the level that would be consistent with achieving our target of 2% CPI inflation,” Kozicki emphasized the Bank’s commitment to continuous evaluation of several factors such as “the evolution of excess demand, inflation expectations, wage growth and corporate price-setting behaviour” to ensure alignment with the 2% inflation target.

To maintain economic stability amidst the dynamic inflationary environment, Kozicki emphasized that the Bank is “prepared to raise the policy interest rate further if needed.”

US treasury yields hit 16-Year peaks as markets await Fed’s insights

As anticipation builds around Fed impending monetary policy decision today, US 5- and 10-year Treasury yields surged to levels not seen in 16 years. With market expectations firming around a hold in the range of 5.25-5.50% – a forecast that has been in place for over a month – the possibility of any shock moves by the Fed is remote.

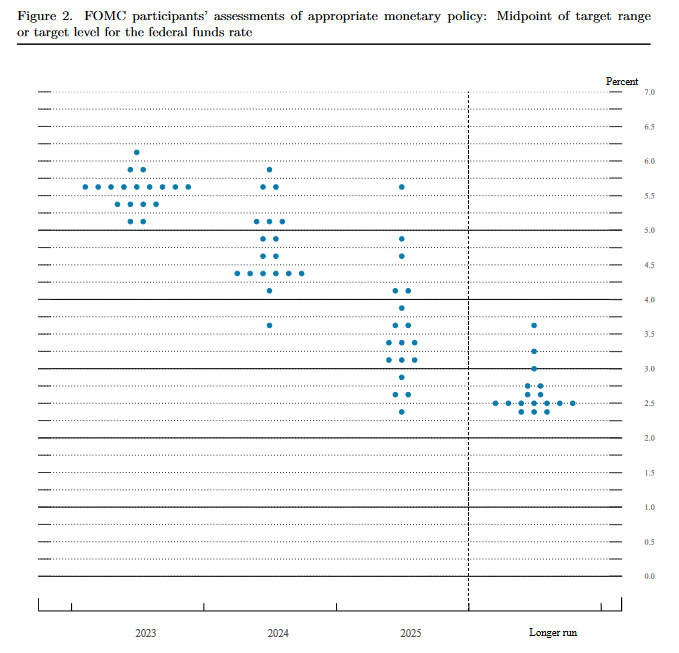

Nevertheless, investors will keenly dissect any subtle hints from Fed that might suggest another rate hike this year, or provide clues about the timing and speed of monetary easing in 2024. The forthcoming “dot plot” will be of particular significance.

To recall, in their June meeting, 12 out of 18 policymakers envisioned at least one more rate hike in the calendar year. 10 anticipated interest rates to fall back to 4.50-4.75% by the close of 2024. The evolving position of these dots is bound to sculpt market sentiments for the forthcoming months.

Five-year yield exhibited a strong close overnight, at an unmatched zenith since 2007, recording a 4.521. This surge found an ally in the WTI crude oil, which leaped, touching the 93-mark.

On the technical front, FVX looks ready to resume is long term up trend to finally get rid of resistance zone at around 4.5. The next hurdle is 38.2% projection of 3.205 to 4.495 from 4.165 at 4.657.

Any upside surprises in today’s Fed inflation projections could potentially steer FVX towards the 4.657 projection level. Yet, surpassing this level might necessitate a sustained WTI oil rally, breaking the 95 mark and advancing towards 100.

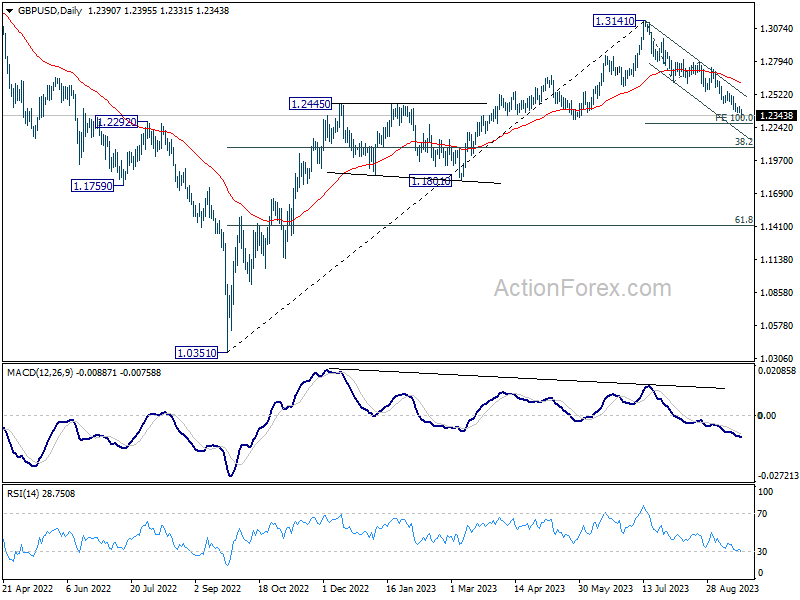

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2366; (P) 1.2396; (R1) 1.2421; More…

GBP/USD’s fall resumed after brief consolidations and intraday bias is back on the downside. Current fall from 1.3141 should target 1.3141 to 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276. Decisive break there will target 1.2075 fibonacci level next. On the upside, above above 1.2423 minor resistance will turn intraday bias neutral again. But near term outlook will stay bearish as long as 1.2618 support turned resistance holds, in case of strong recovery.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. However, sustained break of 1.2075 will raise the chance of bearish trend reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account (NZD) Q2 | -4.21B | -4.40B | -5.22B | -4.66B |

| 23:50 | JPY | Trade Balance (JPY) Aug | -0.56T | -0.44T | -0.56T | -0.60T |

| 00:30 | AUD | Westpac Leading Index M/M Aug | 0.00% | 0.00% | ||

| 06:00 | EUR | Germany PPI M/M Aug | 0.30% | 0.20% | -1.10% | |

| 06:00 | EUR | Germany PPI Y/Y Aug | -12.60% | -12.80% | -6.00% | |

| 06:00 | GBP | CPI M/M Aug | 0.30% | 0.70% | -0.40% | |

| 06:00 | GBP | CPI Y/Y Aug | 6.70% | 7.10% | 6.80% | |

| 06:00 | GBP | Core CPI Y/Y Aug | 6.20% | 6.80% | 6.90% | |

| 06:00 | GBP | RPI M/M Aug | 0.60% | 0.90% | -0.60% | |

| 06:00 | GBP | RPI Y/Y Aug | 9.10% | 9.30% | 9.00% | |

| 06:00 | GBP | PPI Input M/M Aug | 0.40% | 0.20% | -0.40% | |

| 06:00 | GBP | PPI Input Y/Y Aug | -2.30% | -2.70% | -3.30% | -3.20% |

| 06:00 | GBP | PPI Output M/M Aug | 0.20% | 0.20% | 0.10% | 0.20% |

| 06:00 | GBP | PPI Output Y/Y Aug | -0.40% | -0.80% | -0.70% | |

| 06:00 | GBP | PPI Core Output M/M Aug | -0.10% | 0.10% | ||

| 06:00 | GBP | PPI Core Output Y/Y Aug | 1.60% | 2.30% | 2.20% | |

| 07:00 | CHF | SECO Economic Forecasts | ||||

| 14:30 | USD | Crude Oil Inventories | -1.3M | 4.0M | ||

| 18:00 | USD | Fed Rate Decision | 5.50% | 5.50% | ||

| 18:30 | USD | FOMC Press Conference |

When The Wave Turns

Why Retirement Investing Is Moving Towards Resilience Jeremy Grantham’s latest market warnings have revived an old tru... Read more

Gyrostat Capital Management: July Retirement Portfolio Resilience Assessment

The Market Is Currently Presenting an Opportunity to Strengthen Retirement Portfolio Resilienc... Read more

The Invisible Risk That Decides Your Retirement

Why how investors behave matters more than what markets do and what disciplined port... Read more

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more