Split Personality Markets: Stocks Up, Oil Warns, Dollar Torn

Markets are showing a clear “split personality” right now. Equities are pushing higher on the back of the extended US–Iran ceasefire, while oil continues to signal caution and Dollar is caught between opposing forces. The result is a fragmented picture where no single macro narrative is dominating.

US futures are trading higher after President Donald Trump announced an indefinite extension of the ceasefire. Despite stalled talks, the move has removed the immediate threat of escalation for now, allowing equities to lean risk-on. For the S&P 500 and NASDAQ, the extension is effectively a “yellow light”—not a full green signal, but enough to justify holding or adding exposure in the near term.

At the same time, equities are increasingly pivoting back to fundamentals. Strong Q1 earnings and the continued momentum of the AI-driven investment cycle are providing a more compelling narrative than the geopolitical stalemate. There is a clear effort to decouple from daily headlines, with investors focusing on earnings visibility rather than conflict risk.

In contrast, energy markets are not looking through the situation. Brent may have cooled from peaks above $120, but it remains firmly anchored near $100. This suggests traders are pricing in prolonged disruption in the Strait of Hormuz, even without a full escalation scenario. Oil is effectively signaling that supply risks remain embedded in the system.

This divergence is feeding into the broader inflation outlook. Even without further escalation, the surge in energy costs has already reset the inflation floor. Higher fuel and transport costs are filtering through global supply chains, keeping price pressures elevated and complicating the monetary policy outlook.

Bond markets are reflecting this skepticism. Yields remain supported by the view that Fed cannot pivot quickly toward easing. The persistence of inflation risks means policy is likely to stay restrictive for longer than markets might otherwise expect, with some global central banks pivoting towards tightening.

Currency markets are where these conflicting forces are most visible. Dollar is being pulled in opposite directions. On one hand, the ceasefire extension reduces safe-haven demand. On the other, elevated yields continue to attract capital inflows. Commodity currencies such as the Canadian and Australian Dollars are also caught in this crosscurrent. Higher oil and gas prices are supportive, but the risk of a global slowdown linked to energy-driven inflation caps upside. The result is choppy, range-bound trading rather than directional moves.

This week’s FX performance reflects this lack of conviction. Kiwi is leading on domestic rate expectations, followed by Loonie and Dollar. Yen is the weakest, with Euro and Aussie also under pressure. Sterling and Swiss Franc are holding in the middle. There is no coherent global theme driving currencies.

The broader takeaway is that markets are no longer aligned. Equities are pricing stability, oil is pricing disruption, and bonds are pricing inflation persistence. Each asset class is telling a different story.

Until there is clarity on whether US–Iran talks resume or a decisive shift in geopolitical conditions, this split personality is likely to persist. Markets are not ignoring the risks—but they are no longer reacting to them in the same way.

In Europe, at the time of writing, FTSE is down -0.02%. DAX is down -0.01%. CAC is down -0.30%. UK 10-year yield is down -0.011 at 5.128. Germany 10-year yield up 0.002 at 3.006. Earlier in Asia, Nikkei rose 0.40%. Hong Kong HSI fell -1.22%. China Shanghai SSE rose 0.52%. Singapore Strait Times fell -0.24%. Japan 10-year JGB yield rose 0.013 to 2.399.

UK CPI Hits 3.3% as Fuel Costs Drive Inflation Higher, Pipeline Pressures Build

UK CPI rose to 3.3% in March as fuel costs pushed inflation higher. Core inflation eased slightly, but rising PPI and oil prices signal building pipeline pressures. Read more.

Japan’s Exports Rise 11.7% in March, Trade Surplus Misses

Japan posted another solid month for exports, led by semiconductors and China demand. But the trade surplus still missed expectations as imports jumped on energy costs and a weaker Yen. Read More.

Australia Westpac Leading Index Turns Negative, Signals Below-Trend Growth Ahead.

Australia’s growth signal has turned negative. The Westpac Leading Index now points to below-trend growth, but rising energy costs and inflation risks keep RBA rate hikes firmly on the table. Read More.

Gold and Silver Recover as US Extends Iran Ceasefire, But Technical Weakness Emerges

Ceasefire relief helped stabilize Gold and Silver—but technical cracks are forming. The next move depends on whether support levels hold. Read More.

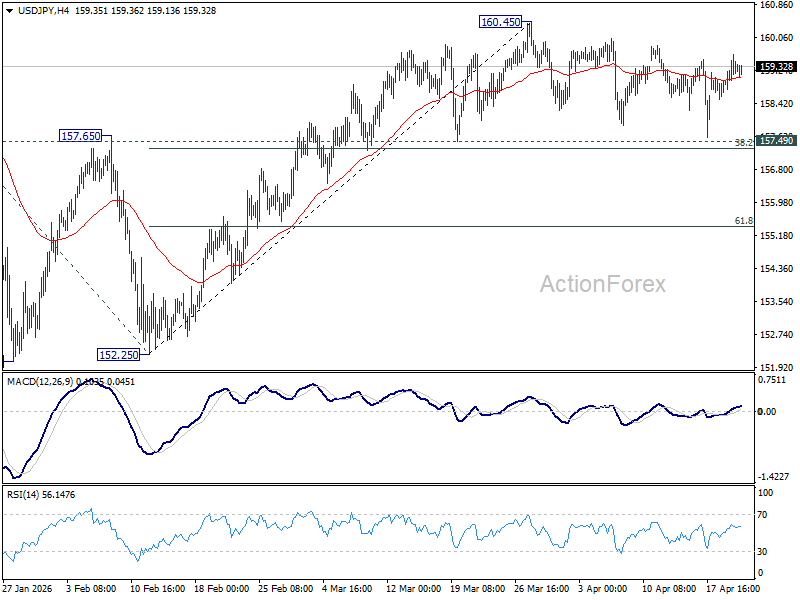

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.80; (P) 159.28; (R1) 159.87; More…

USD/JPY is still gyrating in range below 160.45 as consolidations continues. Intraday bias stays neutral for the moment. Further rise is expected with 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) intact. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

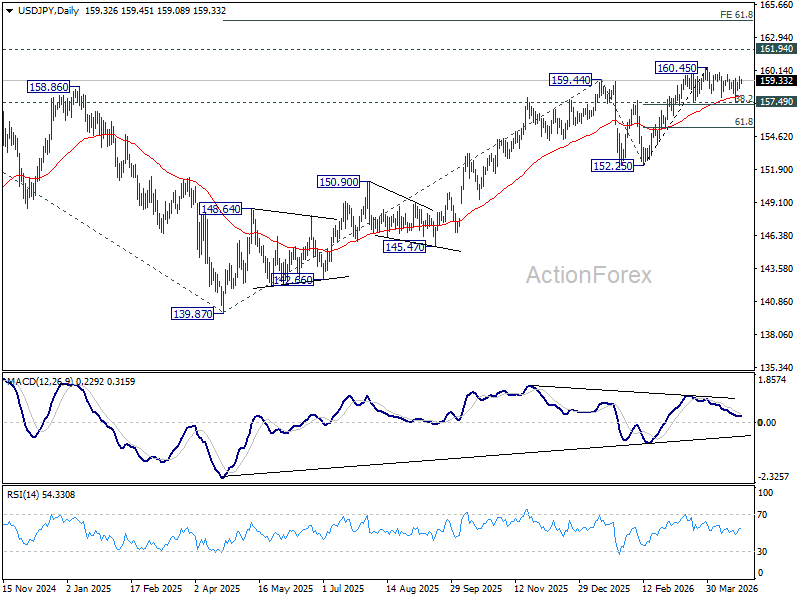

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 153.80) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more