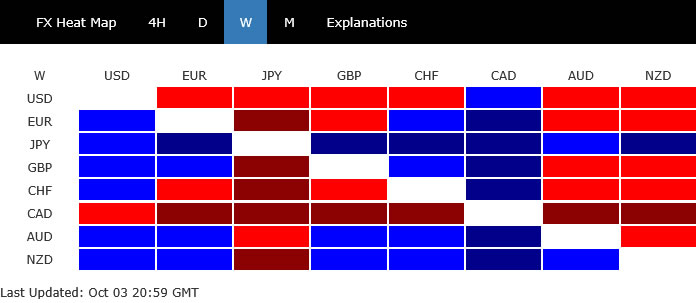

Shutdown Fails To Shake Risk Appetite; Dollar Slips, Not Sinks

A week with political paralysis in Washington ended with record highs on Wall Street — a telling sign of how investors are prioritizing Fed policy over fiscal drama. The U.S. government shutdown, now in effect after Congress failed to pass a funding bill, has frozen major data releases and paralyzed parts of the bureaucracy. Yet for markets, the episode has so far reinforced the belief that the Fed will be compelled to cut rates again this month to cushion a softening economy. Dollar, thus, slipped on the back of falling yields, closing as one of the weakest currencies of the week.

The other laggard was Loonie, dragged lower by tumbling oil prices. WTI crude plunged around 8% as reports surfaced that OPEC+ could drastically raise its planned output increase, potentially flooding the market at a time of weak global demand. That combination — cheaper oil and a dovish BoC — left Canadian Dollar as the week’s worst performer.

In contrast, the Australian Dollar held firm near multi-month highs after the RBA’s hawkish hold. However, by week’s end, the rally began to stall as traders reassessed whether the hawkish tone could still justify more upside.

Meanwhile, Yen led the currency board. The early push came as speculation built over a BoJ rate hike following a hawkish turn from a traditionally dovish board member. But enthusiasm moderated after mixed domestic data and a cautious speech from Governor Kazuo Ueda. Adding a political twist, Sanae Takaichi’s weekend victory in the LDP leadership race made her Japan’s first female prime minister — a milestone that would shape both fiscal and monetary direction.

Taken together, the week captured a global market in transition: U.S. stocks thriving amid fiscal chaos, oil sliding on supply fears, Aussie cooling after a hawkish burst, and Yen strengthening into Japan’s political dawn.

Government Shutdown Boosts Odds of Another Fed Insurance Rate Cut

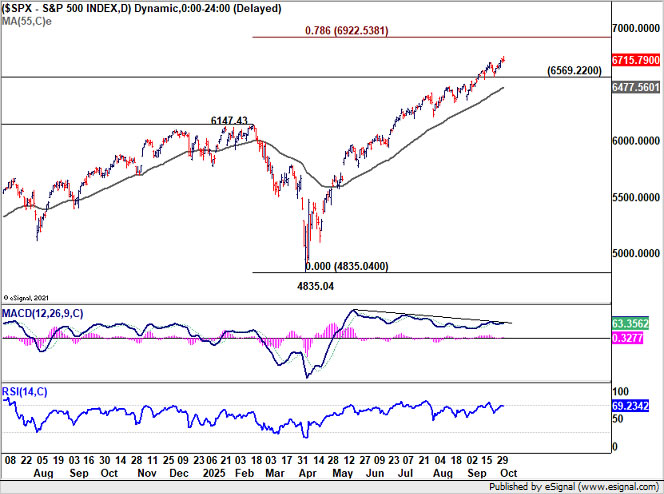

US equities closed another week on a strong note, showing remarkable resilience even as the US federal government entered its latest shutdown. S&P 500 advanced 1.1% over the week, while DOW and NASDAQ each rose 1.3%, extending the post-summer rally. The optimism reflects investors’ continued faith that lower policy rates and AI-related growth can offset mounting signs of a cooling economy.

Historically, US government shutdowns have had little lasting market impact, and this one has proven no different so far. Political gridlock in Washington has delayed some key data releases, most notably the non-farm payroll report. Yet, traders have quickly filled the gap with alternative indicators that suggest the labor market is turning down faster than expected.

Private-sector payrolls contracted by 32,000 in September, the third decline in four months according to ADP data. Both ISM employment sub-indexes remained mired in contraction territory, with manufacturing employment rising modestly to 45.3 and services improving slightly to 47.2. These readings point to a job market that is clearly deteriorating.

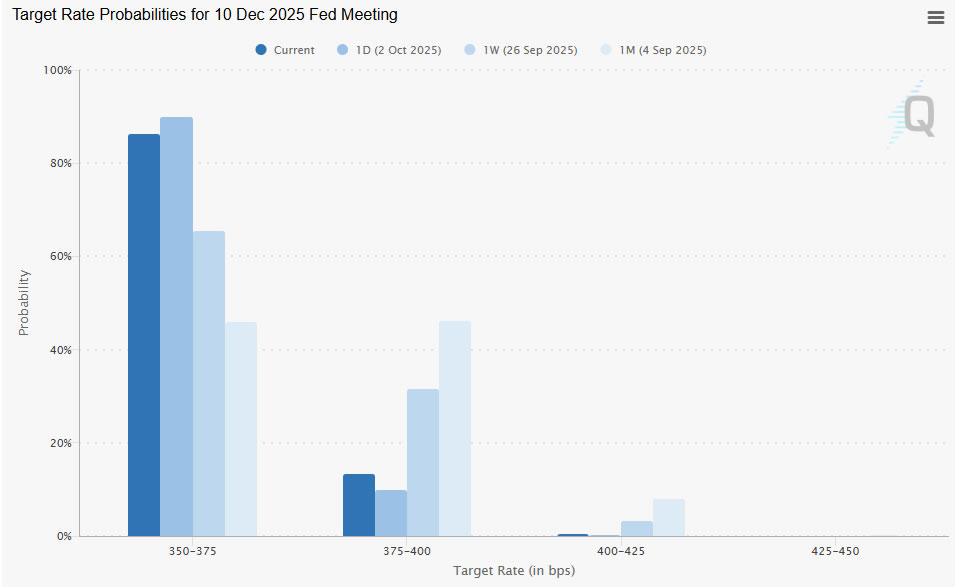

If the shutdown prevents official data from being published before the October 28-29 Fed meeting, these proxy measures may carry unusual weight. Fed will rather err on the side of supporting jobs, and deliver another quarter-point reduction as an “insurance cut”.

Futures markets now assign 96.2% probability to a quarter-point rate cut, taking the target range down to 3.75%–4.00% on October 29. Expectations for another reduction in December have risen back to 86.3%. Nevertheless, it’s still premature to draw a conclusion beyond October.

Equity markets, meanwhile, continue to look through the economic softness. Investors are betting that a dovish Fed will help extend the bull market.

Technically, near term outlook will stay bullish in S&P 500 as long as 6569.22 support holds. Current up trend should target 78.6% projection of 3491.58 to 6147.43 from 4835.04 at 6922.53. Strong resistance would likely be seen around 7000 psychological level to bring pullback, at least on first attempt.

The greenback has softened in tandem with falling yields, as risk appetite improved and traders repositioned for faster Fed easing. Dollar Index’s rebound from 96.21 short term bottom lost momentum and closed back below 55 D EMA (now at 98.01).

Still, further rise would remain mildly in favor as long as 97.22 support holds. Price actions from 96.21 are seen as correcting the whole decline from 110.17. Thus, further rally should be seen to 100.25 resistance. Nevertheless, strong resistance could be seen from the zone between 38.2% retracement of 110.17 to 96.21 at 101.54 and 55 W EMA (now at 100.98) to limit upside. Meanwhile, break of 97.22 will dampen this bullish view, and bring retest of 96.21 low.

Oil Slumps as OPEC+ Eyes Output Hike; Loonie Feels the Heat

Oil prices fell sharply last week, posting their steepest weekly loss in more than three months as supply expectations shifted dramatically. WTI crude tumbled around 8%, breaking key technical levels after reports emerged that OPEC+ members were preparing another round of output increases in November.

According to sources familiar with internal talks, eight OPEC+ producers are likely to back a fresh supply hike at Sunday’s meeting. Saudi Arabia is reportedly leading calls for a sizeable increase to regain market share, while Russia prefers a smaller rise.

The proposed output hike, possibly as large as 500,000 barrels per day, follows a string of production increases this year that have already added more than 2.5 million barrels per day to global supply. Traders fear this could tip the market into surplus in the fourth quarter, particularly as demand indicators in China and Europe remain lackluster.

Geopolitical developments have added further pressure. Hamas has reportedly entered discussions with the Trump administration over a potential peace plan, with Washington giving the group until Sunday night to agree to terms aimed at ending the Gaza conflict. Any progress could remove a geopolitical premium that has lingered over Middle Eastern crude, reinforcing the recent downward momentum.

Technically, the damage is clear. WTI’s decline from June high at 78.87 re-accelerated after breaking 61.90 support. As long as 55 Day EMA (now at 64.33) caps the upside, risk stays skewed to the downside with next target at 100% projection of 71.34 to 61.90 from 66.70 at 57.26. Nevertheless, Strong support should emerge near 55.20 to contain the fall and allow for a rebound.

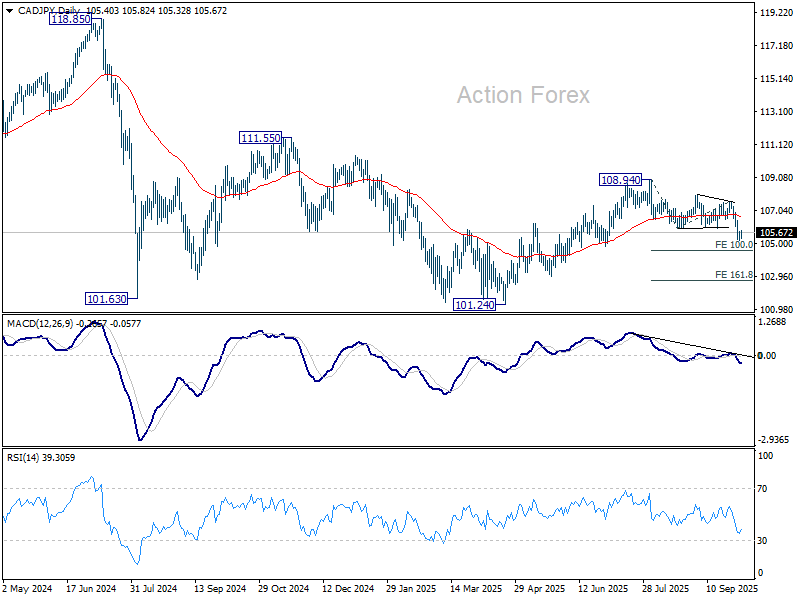

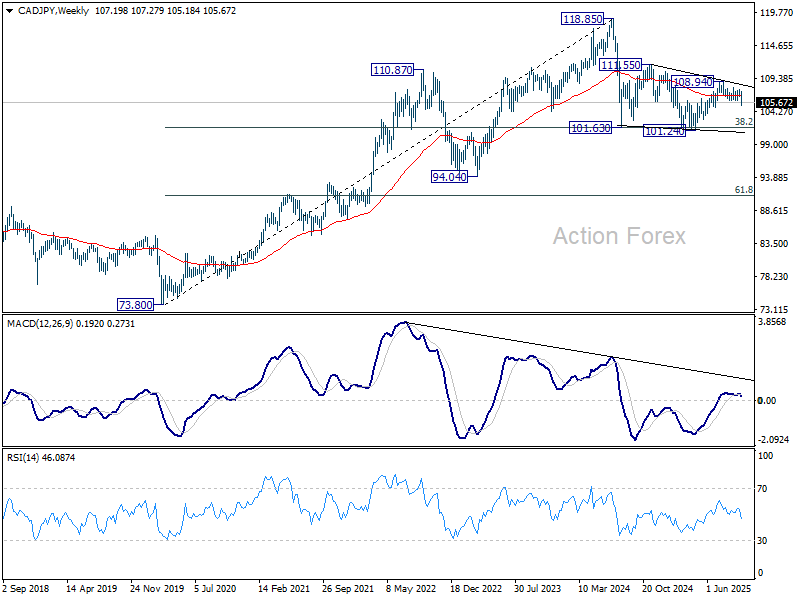

The slide in crude has amplified pressure on Canadian Dollar, which was already undermined by dovish expectations for the BoC. Loonie ended the week as one of the weakest majors, with CAD/JPY leading the losses with a -1.38% drop.

Technically, CAD/JPY’s fall from 108.94 resumed last week. The cross is now targeting 100% projection of 108.94 to 105.93 from 107.61 at 104.60. Decisive break there could prompt downside acceleration to 161.8% projection at 102.73.

More importantly, any near term downside acceleration will raise the chance that whole medium term corrective pattern from 101.63 has already completed. And the decline from 118.85 (2024 high) is ready to resume. This is worth some attention in the next few weeks.

Aussie Rally Fades as RBA Hawkish Tilt Meets Market Fatigue

Australian Dollar started last week on a strong footing, rallying after the RBA kept its cash rate unchanged at 3.60% and leaned slightly hawkish in tone. However, by the end of the week, the momentum faded as Aussie looks exhausted after recent strong rise.

The key takeaway from the RBA’s October meeting was its warning that third-quarter inflation may surprise to the upside. The Bank’s statement noted that recent data—though volatile—suggested price pressures had not cooled as quickly as anticipated. Governor Michele Bullock refrained from committing to a specific policy path, telling reporters she would not “predict what the interest rate is going to be in the next three to six months.” That cautious phrasing was interpreted as a signal that the central bank is more comfortable holding rates steady for longer.

Major banks quickly updated their forecasts. Commonwealth Bank of Australia scrapped expectations of another rate cut this year. It now sees the next easing move pushed back to February 2026, citing a “shift in tone” from the RBA and stronger inflation dynamics. CBA expects Q3 trimmed mean inflation to rise 0.8% quarter-on-quarter, keeping the annual pace steady at 2.7%.

National Australia Bank also turned less dovish. Chief Economist Sally Auld said she now expects the RBA to stay on hold through May 2026, with only one more 25-basis-point cut thereafter. NAB removed its earlier projections for two rate reductions in November and February, aligning with the view that inflation persistence will delay further easing.

Westpac and ANZ are still penciling in a November cut, but both have softened their conviction. Analysts at Westpac noted that while disinflation remains broadly on track, recent strength in household spending and services inflation could force the RBA to wait for more evidence before pulling the trigger.

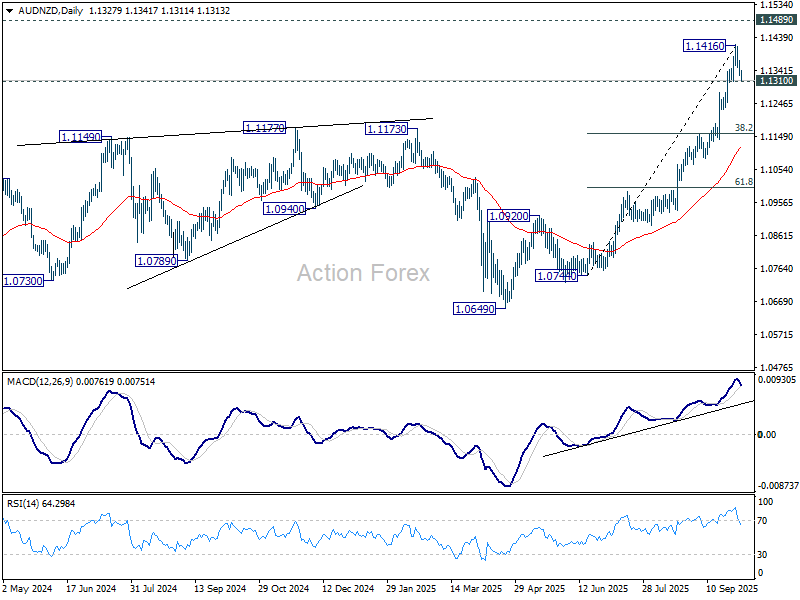

Nevertheless, traders appear reluctant to chase the currency higher, suggesting that the hawkish tilt might have already been well priced in. The fading momentum in AUD/NZD captures this fatigue most clearly, with the cross retreating after peaking at 1.1416.

Technically, the immediate focus is now on 1.1310 support. Decisive break there would confirm short-term top at 1.1416 and set the stage for a correction of the entire rally from 1.0744. In that case, the next target would be 38.2% retracement of 1.0744 to 1.1416 at 1.1159.

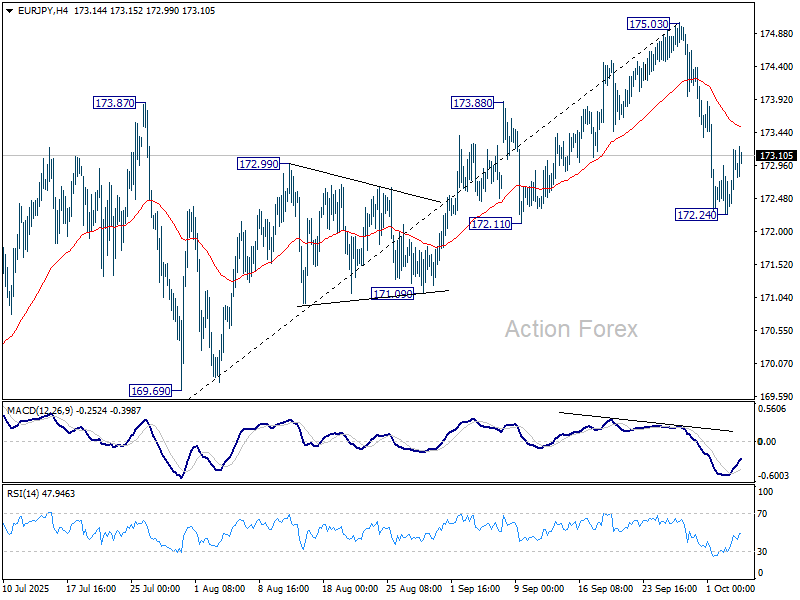

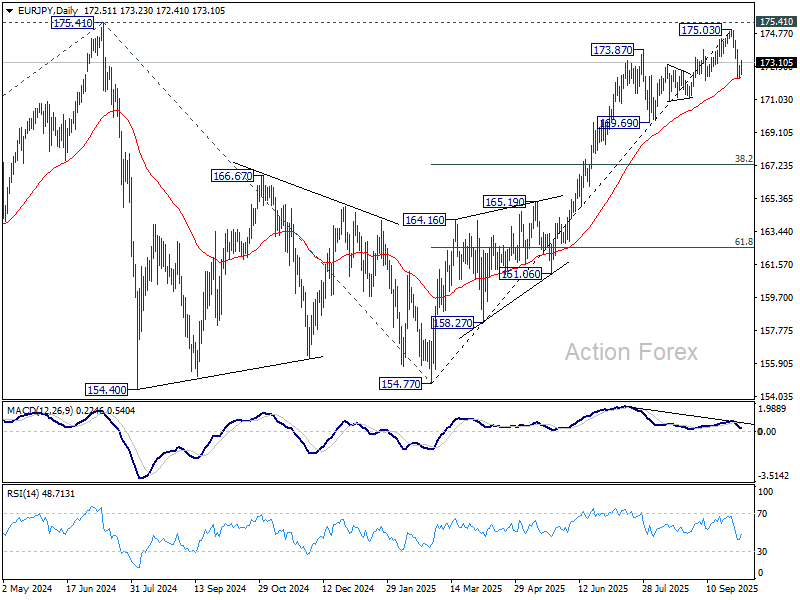

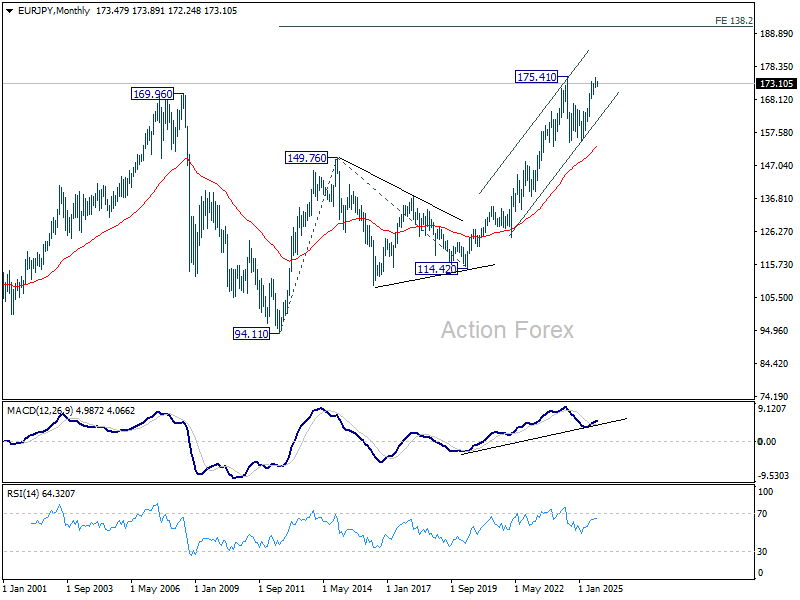

EUR/JPY’s steep pullback last week confirmed short term topping at 175.03, just ahead of 175.41 high. But the cross then recovered after hitting 55 D EMA (now at 172.25). Initial bias remains neutral this week, with risk staying on the downside as long as 175.03 resistance holds. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA will indicate that whole five-wave rise from 154.77 has completed. Deeper decline should then be seen to 169.69 support next, and possibly to 38.2% retracement from 154.77 to 175.03 at 167.29.

In the bigger picture, rise from 154.77 is seen as resuming the larger up trend from 114.42 (2020 low). While initial set back could be seen as it tests 175.41 (2024 high), outlook will stay bullish as long as 55 W EMA (now at 166.48) holds. However, sustained break of the 55 W EMA will dampen this bullish case, and bring deeper fall back to 154.77 to extend the pattern from 175.41.

In the long term picture, up trend from 94.11 (2021 low) is still in progress. On resumption, next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more