Risk Appetite Holds Firm Near Highs As ECB Pushback Caps Euro, Aussie Outperforms

Risk sentiment remains firm, but momentum is no longer accelerating. Markets are holding near recent highs as optimism over Middle East de-escalation continues to underpin sentiment, with US futures pointing to another strong open and the potential for fresh record highs in the S&P 500. At the same time, the tone is measured rather than euphoric, suggesting that much of the positive news is already priced in.

Across asset classes, price action reflects this consolidation phase. Oil prices are trading in a tight range just above this week’s spike lows, indicating that the war premium has largely stabilized rather than unwound further. Precious metals are also struggling to extend gains, with Gold struggling to build momentum above 4800, and Silver failing to sustain moves above 80. The lack of follow-through highlights a market that is comfortable, but not chasing risk aggressively.

In currency markets, Dollar has staged a modest recovery but remains the worst performer for the week, reflecting the broader unwind of safe-haven demand. Yen is not far behind, while Euro is also lagging. In contrast, Aussie continues to lead, followed by Kiwi and Loonie, reinforcing the view that risk-sensitive currencies remain favored in the current environment.

Euro’s underperformance is being driven by clear pushback from ECB officials against near-term tightening expectations. The March policy accounts emphasized that temporary deviations from the inflation target “could be tolerated” as long as they are “short-lived and limited in size” and do not risk de-anchoring expectations. This signals a willingness to look through the current energy-driven inflation spike.

That stance has been reinforced by recent comments from policymakers. Executive Board member Isabel Schnabel noted that the ECB is in a “relatively favorable” position and stressed that “we do not need to rush into action.” President Christine Lagarde echoed this cautious tone, emphasizing that the current uncertainty “does not determine a rate path,” effectively ruling out any pre-commitment to tightening.

Market pricing reflects this shift. Odds of a rate hike at the April meeting fell to around 20%, while expectations are increasingly shifting toward June, where probabilities rise to around 80%. Goldman Sachs has also pushed back its forecast for the start of the ECB’s tightening cycle to June.

In contrast, Australian Dollar continues to benefit from both global and domestic drivers. Strong employment data has reinforced the case for further tightening by the Reserve Bank of Australia, with the labor market showing little sign of loosening. The steady unemployment rate at 4.3% suggests the economy remains near full employment.

Markets have responded by increasing expectations for a May rate hike, with swaps now pricing around a 67% probability, up from about 60% a week ago. This repricing underscores the divergence in policy outlooks, with the RBA seen as moving closer to further tightening while the ECB remains cautious.

Overall, the current market environment is defined by stability rather than acceleration. Risk appetite is holding firm, but gains are consolidating as investors await the second round of US-Iran talks.

In Europe, at the time of writing, FTSE is up 0.72%. DAX is up 0.68%. CAC is up 0.54%. UK 10-year yield is down -0.018 at 4.740. Germany 10-year yield is down -0.039 at 3.008. Earlier in Asia, Nikkei rose 2.38%. Hong Kong HSI rose 1.72%. China Shanghai SSE rose 0.70%. Singapore Strait Times fell -0.27%. Japan 10-year JGB yield rose 0.002 to 2.406.

US Initial Unemployment Claims Fall to 207k as Labor Market Remains Tight

US jobless claims fell again, highlighting low layoffs, but rising continuing claims suggest workers are taking longer to find new jobs. Read more.

ECB Minutes Signal Willingness to Tolerate Temporary Inflation Deviations

ECB minutes show policymakers are willing to tolerate temporary inflation spikes, focusing instead on whether pressures become persistent and feed into wages and expectations. Read more.

Eurozone Inflation Jumps to 2.6%, Energy and Services Drive

Eurozone inflation rose sharply in March, driven by energy and services, but core CPI eased slightly—highlighting rising external pressures with stable underlying inflation. Read more.

UK GDP Beats Expectations at 0.5% mom with Broad-Based February Growth

UK economic growth surprised to the upside in February, with GDP rising well above expectations on broad-based gains across key sectors. But beneath the headline strength, underlying trends remain uneven, with construction still dragging on the three-month outlook. Read More.

SNB Minutes Stress Intervention as Franc Surge Threatens Price Stability

SNB minutes show policymakers are ready to intervene as safe-haven flows push the Swiss franc higher, raising risks to price stability. Read more.

Australia’s 17.9k Job Growth Driven by Full-Time Gains, Unemployment Rate Steady at 4.3%.

Australia’s labor market held steady in March, with employment rising in line with expectations and full-time jobs surging. Strong gains in hours worked point to resilient labor demand. Read more.

China’s 5% GDP Growth Tops Forecasts as Supply Holds Firm, Demand Lags

China’s economy beat expectations in Q1, but weak retail sales and falling investment highlight an uneven recovery driven by supply, not demand. Read more.

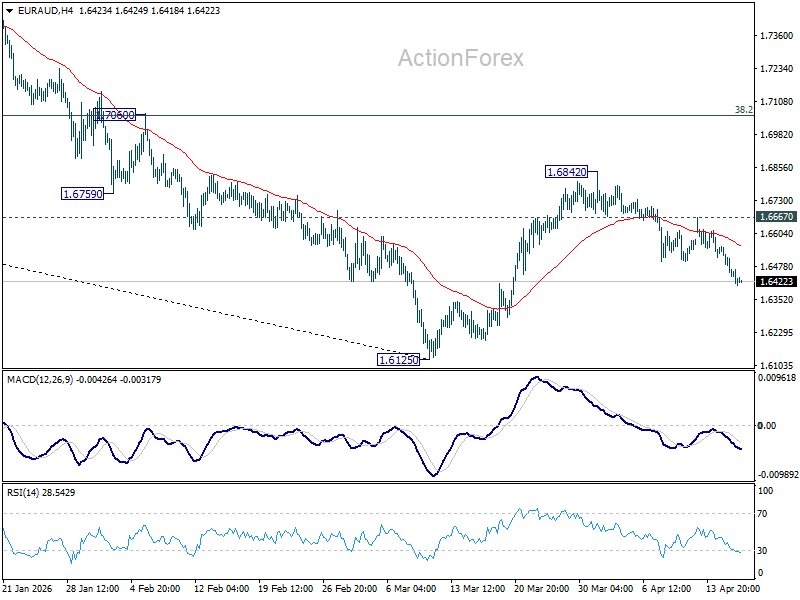

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.6405; (P) 1.6493; (R1) 1.6544; More…

EUR/AUD’s fall from 1.6842 continues today and intraday bias stays on the downside for retesting 1.6125 low. Firm break there will resume whole down trend from 1.8554 to 1.5913 fibonacci level next. For now, risk will stay on the downside as long as 1.6667 resistance holds, in case of recovery.

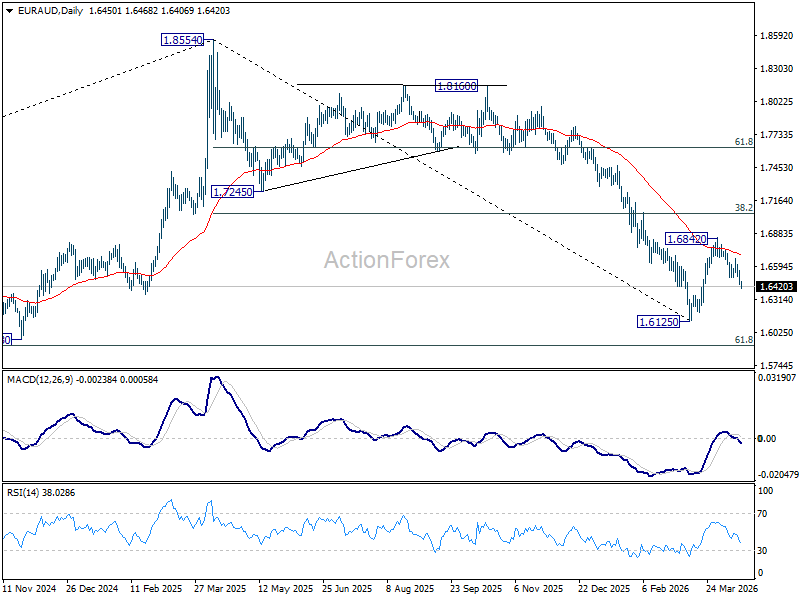

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7163) holds, even in case of strong rebound.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more