Quarter-End Calm Masks High-Stakes Week For Fed, ECB, BoJ And RBA

Financial markets began the week on a subdued note, with quarter-end positioning and caution ahead of a packed economic calendar keeping most major assets confined to familiar ranges. Geopolitical headlines surrounding the US-Iran conflict attracted little attention, while Brent crude held steady around USD 73 a barrel, suggesting investors are increasingly viewing Middle East tensions as a manageable risk rather than an immediate market driver.

Price action across asset classes reflected the lack of conviction. Asian equities ended mixed, with Japanese and South Korean shares little changed, while major European indices traded modestly lower. US futures pointed to a slightly firmer open. Currency markets were similarly directionless. New Zealand Dollar, Pound Sterling and Euro outperformed modestly, while Canadian Dollar, Japanese Yen and US Dollar lagged. Australian Dollar and Swiss Franc traded near the middle of the pack, with most major pairs and crosses remaining comfortably within last week’s trading ranges.

The restrained tone is understandable given an unusually compressed trading week. US markets will close early ahead of the Independence Day holiday, leaving investors with less time to reposition before several major economic releases. Rather than responding to incremental headlines, markets appear content to wait for data capable of reshaping monetary policy expectations.

The centerpiece will be Thursday’s US Non-Farm Payrolls report. Markets have scaled back expectations for aggressive Federal Reserve tightening after June’s PCE inflation data eased concerns over a second wave of price pressures. One additional rate hike this year is now the prevailing expectation. However, another resilient employment report could quickly revive speculation that the Fed may need to tighten more aggressively, setting the tone for the Dollar, Treasury yields and broader risk sentiment heading into the third quarter.

The US data calendar also includes Wednesday’s ISM Manufacturing survey. Beyond the headline index, investors will closely examine the relationship between new orders and inventories. Manufacturing activity has benefited in recent months from precautionary stockpiling during the disruption to Middle East shipping routes. If inventories remain elevated while new orders begin to soften, it could signal that manufacturers are entering an inventory adjustment phase that weighs on production later this year.

Elsewhere, Wednesday’s Eurozone flash CPI will be critical for expectations surrounding the European Central Bank’s August meeting. Recent survey data suggest inflation pressures continue to moderate, but another upside surprise could strengthen the case for additional policy tightening. In Japan, the Bank of Japan’s Tankan survey will be scrutinized for evidence that stronger business conditions and price dynamics are providing further support for policymakers advocating a faster pace of normalization.

Attention will also turn to Tuesday’s Reserve Bank of Australia meeting minutes. Policymakers have maintained a distinctly hawkish tone despite leaving rates unchanged, leaving markets divided over whether the tightening cycle has ended or whether another increase in August remains possible. Investors will be looking for clues on how high the hurdle has become for another rate hike.

The absence of strong market moves today should therefore not be mistaken for complacency. Instead, investors appear to have reached a temporary equilibrium, with quarter-end positioning giving way to a series of economic releases that will test expectations for the Fed, ECB, BoJ and RBA in quick succession.

USD/JPY Enters High-Stakes Game of Chicken Ahead of Non-Farm Payrolls

USD/JPY’s climb toward 162.00 has become a high-stakes game of chicken. Japan appears reluctant to intervene before US Non-Farm Payrolls, but that patience may create an even greater intervention risk once the data is released and holiday-thinned liquidity takes over. Read More.

Gold’s Rebound Lacks Conviction as Jobs Report Could Reopen Fed Hike Debate

Gold’s recovery above $4000 looks more like hesitation than a genuine turnaround. With markets already pricing one Fed hike this year, Thursday’s US jobs report could determine whether that consensus holds or shifts back toward more aggressive tightening. We examine how each payroll scenario could reshape the Dollar, Fed expectations, and Gold’s technical outlook. Read More.

Eurozone Economic Sentiment Improves Further, But Hiring Expectations Weaken

Confidence is returning to the euro area, yet employers are turning more cautious. Discover why stronger sentiment has not translated into stronger hiring and what that says about the region’s economic recovery. Read More.

BoE’s Pill: Structural Changes Leave UK Inflation More Persistent

Why has UK inflation proved so difficult to bring back to target? BoE Chief Economist Huw Pill argues the answer lies in structural changes that have made price pressures more persistent, strengthening the case for interest rates to stay higher for longer. Read More.

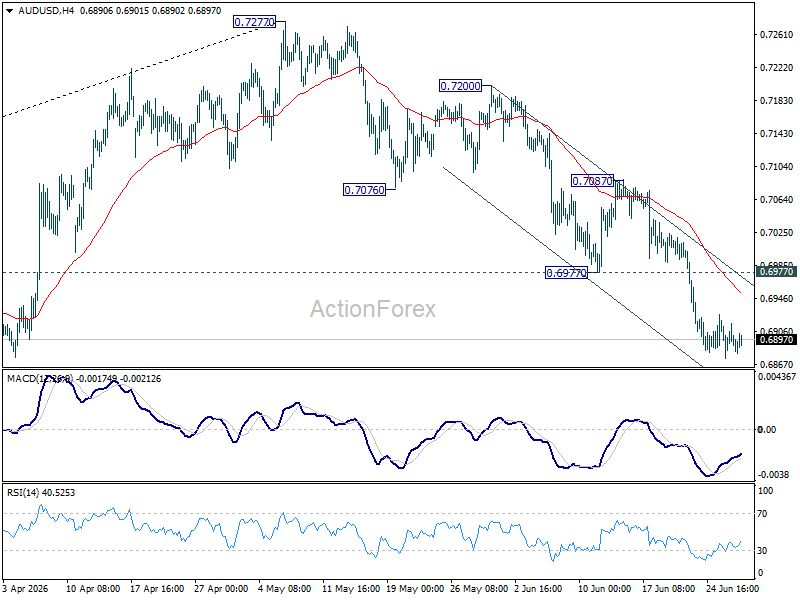

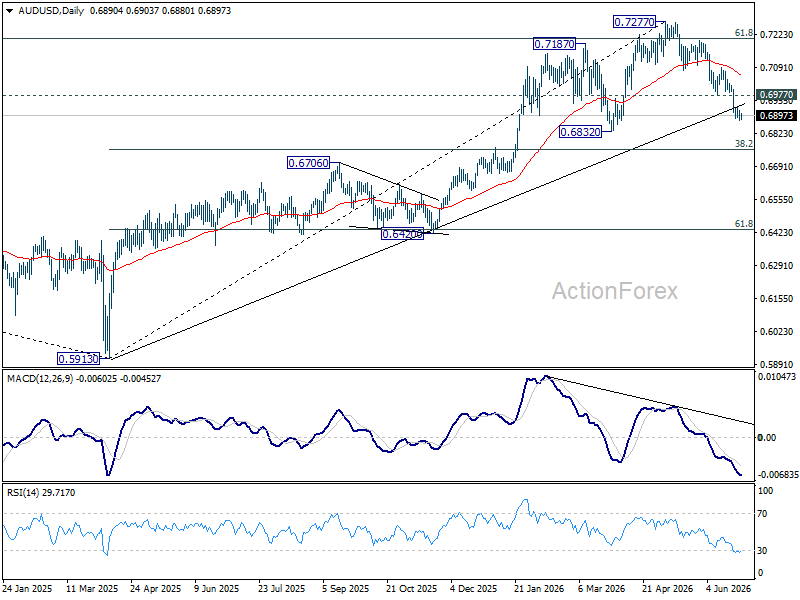

AUD/USD Daily Report

Further decline is expected in AUD/USD with 0.6977 support turned resistance intact. Current fall from 0.7277 should extend to 0.6832 support. Firm break there will target 0.6756 fibonacci level.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top could be formed at 0.7277 after failing to sustain above 61.8% retracement of 0.8006 (2021 high) to 0.5913 (2024 low) at 0.7206. Deeper fall could be seen to 38.2% retracement of 0.5913 to 0.7277 at 0.6756 as a correction. But strong support should be seen there to bring rebound. Consolidations would continue below 0.7277 for a while.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more