Powell Dovish Tilt Keeps Dollar In Consolidation, AUD Outperforms

Aussie is leading the performance board today, supported by stronger-than-expected CPI data and t risk-on tone across the region. Headline inflation ticked up to 3.0%, reinforcing the view that the RBA will remain on hold at 3.60% next week. Next week’s statement and press conference could emphasize vigilance on inflation, while deferring major decisions until the more comprehensive quarterly CPI report is released in October.

Risk sentiment in Asia added to AUD’s bid. Hong Kong equities jumped despite the city being under a No. 10 typhoon signal, the highest warning level. Investor confidence was boosted by news that American fund manager Cathie Wood had increased her stake in Alibaba, helping the Hang Seng shrug off storm-related disruption and fueling broader regional risk appetite.

Dollar, meanwhile, remains in consolidation. Fed Chair Jerome Powell’s remarks were read as slightly dovish, highlighting that job creation is now likely below the breakeven rate for unemployment rate, while characterizing tariff-driven inflation as a one-off effect. His comments reinforced the case for gradual easing, though not an aggressive path.

Still, Fed officials remain divided. While some emphasize preemptive support for the labor market, others stress the need to guard against entrenched inflation. This debate is unlikely to be settled before the next set of employment and inflation data, leaving the Dollar without a clear driver in the near term.

For the week so far, Euro is currently the top performer, followed by Aussie and Swiss Franc. Loonie is the weakest, ahead of Dollar and Kiwi, while Sterling and Yen sit in the middle.

In Asia, at the time of writing, Nikkei is up 0.27%. Hong Kong HSI is up 1.29%. China Shanghai SSE is up 0.78%. Singapore Strait Times is down -0.31%. Japan 10-year JGB yield is down -0.014 at 1.646. Overnight, DOW fell -0.19%. S&P 500 fell -0.55%. NASDAQ fell -0.95%. 10-year yield fell -0.023 to 4.120.

Fed’s Powell: Job creation below breakeven, tariff effect a one-time shock

Fed Chair Jerome Powell said in a speech overnight that the U.S. labor market is showing a “marked slowing” in both supply and demand, calling it an unusual and challenging development. He noted that job creation now appears to be running below the “breakeven” rate needed to keep unemployment rate stable, though other indicators such as job openings and claims remain broadly steady.

On inflation, Powell stressed that recent price pressures are largely tariff-driven rather than evidence of broad-based overheating. Disinflation in services, including housing, continues, and most longer-term inflation expectations remain anchored around the Fed’s 2% goal. Near-term expectations have edged higher on tariff headlines, but Powell argued these effects are likely to be transitory.

He described the tariff shock as a “one-time shift in the price level” that will be “spread over several quarters” as supply chains absorb higher costs.

Powell reaffirmed that Fed policy is “not on a preset course”. Decisions will continue to depend on incoming data and the balance of risks, with the FOMC seeking to manage both slowing job growth and temporary tariff-related inflation without overreacting.

Japan’s PMI composite falls to 51.1, services resilient as factories struggle

Japan’s private sector lost momentum in September, with the flash PMI Composite slipping from 52.0 to 51.1, the weakest in four months. Manufacturing was the clear drag, with the headline index down from 49.7 to 48.4 and output falling from 49.8 to 47.3. Services held broadly steady at 53.0, down from 53.1.

S&P Global’s Annabel Fiddes said services remain the “key growth engine,” offsetting a “deepening downturn” in manufacturing. Demand trends diverged sharply, with services seeing another solid rise in sales, but factories reporting the fastest drop in new orders since April.

Cost pressures also remain high. Input price inflation has eased from earlier in the year but is still consistent with a sharp rate overall, prompting firms to raise selling prices to protect margins. Companies were more cautious on hiring, with employment growth slowing to the weakest pace in two years.

Australia CPI surprises at 3.0% in August, RBA caution ahead

Australia’s monthly CPI accelerated from 2.8% yoy to 3.0% yoy in August, above expectations of 2.8% yoy and the highest reading since July 2024. The rise was driven by housing (+4.5%), food and non-alcoholic beverages (+3.0%), and alcohol and tobacco (+6.0%).

Core inflation showed stickier trends. CPI excluding volatile items and holiday travel rose from 3.2% yoy to 3.4% yoy. Trimmed mean edged down slightly to 2.6% from 2.7%, but remain well above June’s 2.1% yoy.

RBA is widely expected to hold interest rate unchanged next week. But the stronger core reading will keep November’s meeting live, with rate cut expectations now tempered by concerns that inflation may not be easing as quickly as hoped.

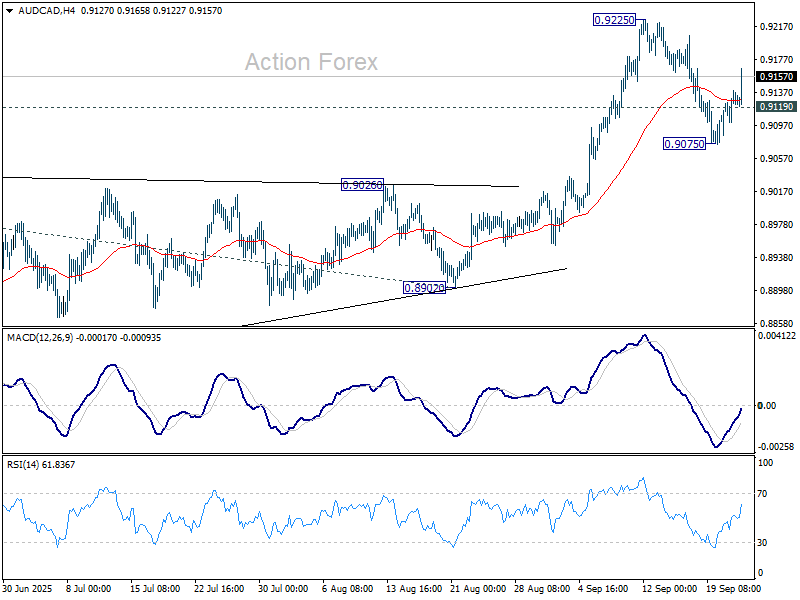

Aussie jumps on strong CPI; AUD/NZD extends rally, AUD/CAD to follow

Aussie strengthened broadly in Asian session after inflation came in hotter than expected. Headline CPI rose to 3.0%, putting price growth back at the top of the RBA’s 2–3% target band.

For next week’s RBA meeting, the outcome makes little difference — a hold at 3.60% was already priced in. But for November, markets will have to reassess. With headline and core measures still sticky, the RBA may decide that it is premature to deliver another rate cut.

Governor Michele Bullock’s comments earlier this month resonate more strongly after today’s release. She highlighted that households are beginning to spend again after a period of restraint, warning that momentum could limit how far and fast the RBA can ease. The CPI data reinforces her message. And, even if a November cut is delivered, the broader policy path is unlikely to accelerate.

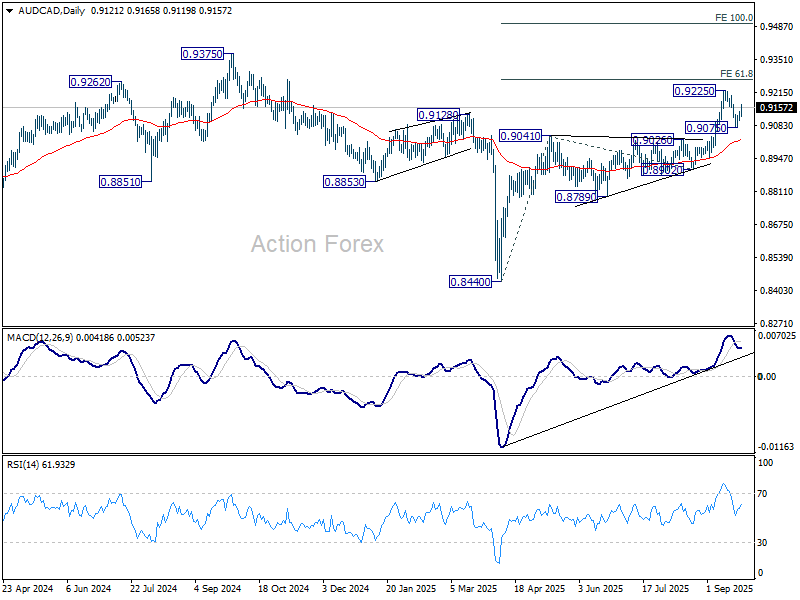

Technically, AUD/CAD’s strong rebound today suggests that corrective pullback from 0.9225 could have completed at 0.9075 already. Break of 0.9225 will resume the whole rally from 0.8440 to 61.8% projection of 0.8440 to 0.9041 from 0.8902 at 0.8273. Firm break there will pave the way to 100% projection at 0.9503.

Nevertheless, below 0.9119 minor support will delay the bullish case, and bring more consolidations in the near term.

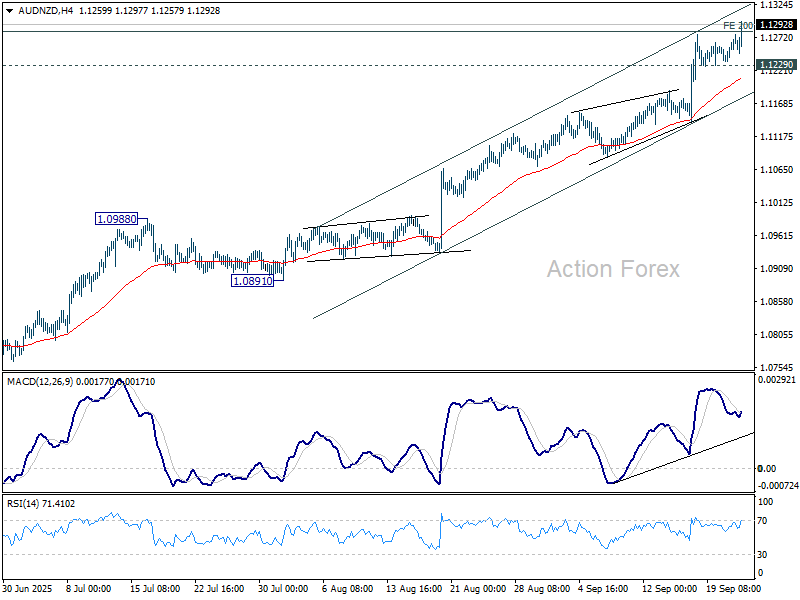

AUD/NZD is also extending its advance, aided by speculation of a 50bps RBNZ cut at the next meeting. Sustained trading above 200% projection of 1.0649 to 1.0920 from 1.0744 at 1.1286 will pave the way to 261.8% projection at 1.1453.

However, below 1.1229 minor support will bring consolidations first.

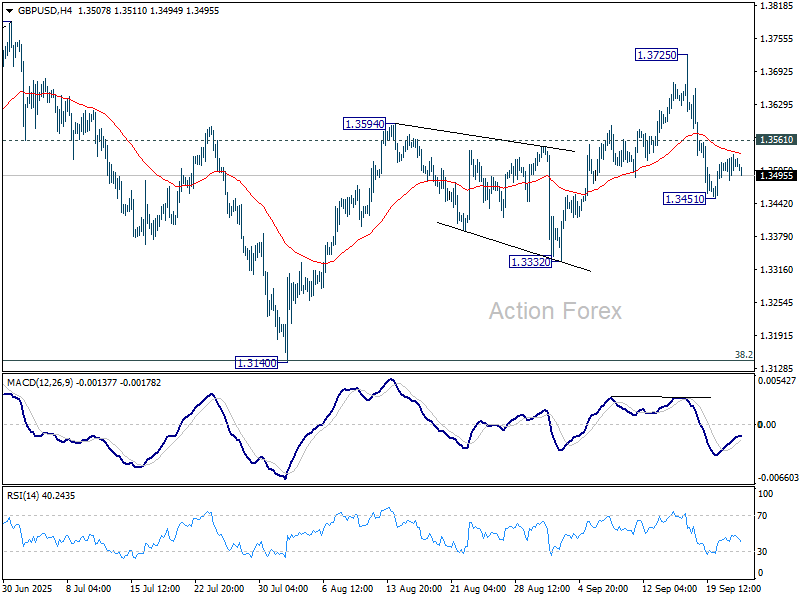

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3496; (P) 1.3517; (R1) 1.3546; More…

Intraday bias in GBP/USD remains neutral and more sideway trading could be seen above 1.3451. On the downside, below 1.3451 will resume the fall from 1.3725, as the third leg of the pattern from 1.3787, and target 1.3332 support first. Nevertheless, decisive break of 1.3561 will turn bias back to the upside for retesting 1.3725 instead.

In the bigger picture, rise from 1.3051 (2022 low) is in progress, and would target 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. However, with 1.4248 resistance (2021 high) intact, this rally is more likely a corrective move. Sustained break of 55 W EMA (now at 1.3157) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more