Oil Shock Drowns Out Weak NFP, Risk Aversion Supports Dollar

Markets appeared largely unfazed by the shockingly weak US non-farm payroll report, as attention is already occupied by the explosive surge in oil prices. WTI crude has broken decisively above the 85 mark and continues to climb as the US session begins, turning energy markets into the dominant driver of global sentiment.

The weak payrolls report has shifted Fed expectations. The probability of the Fed holding rates at the current 3.50–3.75% range has fallen to around 50%, compared with roughly 67% just a day earlier. In effect, a 25-basis-point rate cut in the first half of the year has marginally returned to the table. However, the outlook remains highly dependent on how inflation evolves amid surging energy prices.

Surprisingly, Dollar has not weakened in response to the poor jobs report. Instead, the greenback is drawing support from risk aversion as equity markets come under pressure. DOW futures have fallen more than -1.2%, signaling a sharply weaker open for US equities and reinforcing safe-haven demand for the Dollar.

The real shock to markets is coming from the oil complex. WTI’s surge above 85 signals that markets are transitioning from geopolitical “risk-off” concerns to a more severe phase of structural panic. The effective blockade of the Strait of Hormuz provided the initial spark, but the latest comments from Qatar Energy Minister Saad al-Kaabi have dramatically intensified fears of a prolonged supply crisis.

Kaabi warned that Gulf energy exporters may soon declare force majeure, a move that would legally free them from their contractual delivery obligations. Such a scenario would mean that the world is no longer facing a temporary logistical disruption but rather a potential evaporation of Middle Eastern supply.

The minister’s remarks have also introduced a new psychological anchor for energy markets. By openly referencing the possibility of oil reaching 150 per barrel, Kaabi has effectively reset the upper bound of market expectations. Traders are increasingly beginning to price in the “chain reaction” he described.

That chain reaction could involve shortages of both crude oil and LNG feedstocks, forcing industrial shutdowns across Europe and Asia if supply disruptions persist. In that context, the recent surge above 85 is no longer seen as an extreme price level but rather an early stage of a potentially much larger move.

Even a rapid de-escalation in the Middle East may not immediately stabilize energy markets. With tanker traffic halted through the Strait of Hormuz, restoring supply chains could take weeks or even months after hostilities end.

In the currency markets, for the week so far, Loonie is the strongest performer, benefiting directly from rising oil prices, while the US Dollar holds second place as risk aversion lifts demand for safe assets. Sterling follows as the third-best performer. At the other end of the spectrum, Kiwi is the weakest currency this week, followed by Euro and Aussie. Swiss Franc are trading near the middle of the pack as markets grapple with the increasingly dominant energy shock narrative.

In Europe, at the time of writing, FTSE is down -1.28%. DAX is down -1.56%. CAC is down -1.39%. UK 10-year yield is up 0.174 at 4.655. Germany 10-year yield is up 0.029 at 2.874. Earlier in Asia, Nikkei rose 0.62%. Hong Kong HSI rose 1.72%. China Shanghai SSE rose 0.38%. Singapore Strait Times rose 0.03%. Japan 10-year JGB yield rose 0.009 to 2.166.

NFP misses big with -92k jobs, but wages hold up

US labor market data delivered a sharp downside surprise in February as non-farm payroll employment contracted by -92k, far below expectations for a 65k increase. The report marks a significant setback for the labor market outlook and contrasts with the relatively resilient signals from earlier indicators such as ADP and ISM employment data.

The details of the report were also weaker than expected. The unemployment rate rose from 4.3% to 4.4%, while the labor force participation rate slipped by -0.1 percentage point to 62.0%.

In addition, payroll revisions were notably negative, with December’s figure revised down by 65k to -17k and January trimmed slightly to 126k, further highlighting the softening momentum in hiring.

Despite the weakness in employment growth, wage pressures remained firm. Average hourly earnings rose by 0.4% mom, above expectations of 0.3%, while annual wage growth held at a solid 3.8%. The average workweek was unchanged at 34.3 hours.

Fed’s Waller downplays oil surge as temporary inflation shock

Fed Governor Christopher Waller signaled that the recent surge in oil prices tied to the Middle East conflict may not significantly alter the longer-term inflation outlook. Speaking to Bloomberg Television, Waller acknowledged that Americans will likely see a noticeable jump in gasoline prices in the near term, warning that drivers could be “a little shocked” when they see prices at the pump.

However, Waller emphasized that if the spike in energy prices unwinds within a few weeks or even a couple of months, “it’s not going to be a big factor down the road.”

From a policy perspective, Waller characterized the current oil shock as closer to a “one-off event” rather than a sustained inflation driver. He reiterated that the Fed focuses primarily on core inflation—which excludes volatile components such as energy and food—precisely because commodity prices can fluctuate sharply in response to temporary shocks without altering the underlying inflation trend.

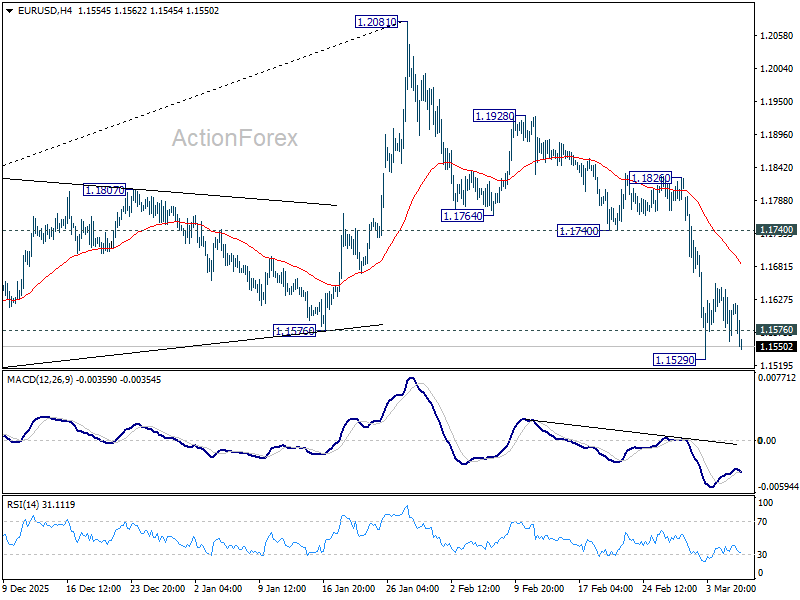

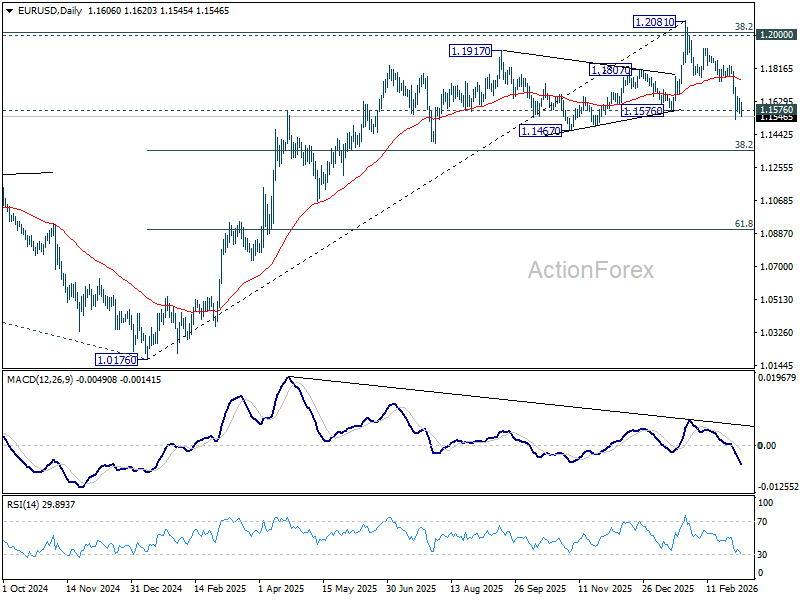

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1564; (P) 1.1605; (R1) 1.1652; More….

EUR/USD weakened notably today but stays above 1.1529 temporary low. Intraday bias stays neutral first. On the downside, below 1.1529 will resume the fall from 1.2081. Sustained break of 1.1576 structural support would confirm rejection by 1.2 key psychological level. That should also confirm medium term topping on bearish divergence condition in D MACD. Further decline should be seen to 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. In any case, risk will stay on the downside as long as 1.1740 support turned resistance holds.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more