Markets Turn To US CPI As Geopolitical Traders Hold Fire

Markets entered a temporary holding pattern on today as traders largely refrained from making aggressive geopolitical bets ahead of both US inflation data and Thursday’s Trump-Xi summit. Despite hostile rhetoric surrounding the Iran ceasefire, broader market reactions remained restrained, with investors appearing reluctant to commit strongly in either direction until clearer signals emerge later this week.

US President Donald Trump sharply escalated his criticism of Tehran overnight, describing the month-old ceasefire as “unbelievably weak” and effectively “on massive life support” after Iran submitted what he called an “unacceptable” counterproposal to Washington’s latest peace framework. “I would say the ceasefire is on massive life support, where the doctor walks in and says, ‘Sir, your loved one has approximately a 1% chance of living,’” Trump said in the Oval Office. Still, markets showed only measured reactions to the comments.

US equities closed modestly higher overnight, Brent crude stayed capped around the $105 level, and the US 10-year Treasury yield edged up only slightly to around 4.41%. Dollar attempted to extend its recent rebound but remained trapped within familiar trading ranges without decisive follow-through momentum. However, despite the deteriorating rhetoric, markets appear increasingly focused on whether larger geopolitical powers can eventually engineer some form of containment framework.

For now, traders appear unwilling to significantly expand geopolitical positioning before Thursday’s Trump-Xi summit in Beijing. When Pakistan’s mediation stalled last month, it exposed a fundamental wall that Islamabad couldn’t climb: Trust and Enforceability. Pakistan has the diplomatic ties, but China has the “checkbook” and the “oil straw” that Iran actually depends on.

China is increasingly viewed as the only party with the leverage to actually reopen the Strait of Hormuz. Recent reports indicate that Iranian officials have been in Beijing specifically to discuss reopening the shipping lanes. Investors likely believe that no matter how much “garbage” (to use Trump’s word) is in the current proposal, the real deal will be brokered—or at least green-lit—by Xi and Trump face-to-face.

As a result, markets are temporarily shifting focus back toward more traditional macro catalysts, with today’s US CPI report as the primary near-term volatility trigger. Markets expect headline CPI to rise 0.6% mom in April, lifting the year-on-year rate to 3.7%, which would mark the strongest inflation reading since September 2023. Core CPI is projected to accelerate from 2.6% yoy to 2.7% yoy, partly boosted by a one-time technical adjustment linked to last year’s government shutdown.

The implications for Federal Reserve expectations could be significant. Investors have already been steadily abandoning expectations for rate cuts this year as energy prices rise and inflation risks re-emerge. A hotter-than-expected CPI report could push markets even further toward pricing a prolonged Fed hold — or potentially reopening discussions around additional tightening. The Senate vote on Kevin Warsh’s nomination as Fed Chair is also due today, though markets currently see little chance of surprise around the outcome.

In currency markets, Dollar is currently the strongest major currency for the week so far, followed by Kiwi and Loonie. Yen is the weakest performer, followed by Swiss Franc and Sterling, reinforcing the idea that investors are not yet embracing a full-scale risk-off positioning shift despite lingering geopolitical uncertainty.

In Asia, at the time of writing Nikkei is up 0.42%. Hong Kong HSI is up 0.15%. China Shanghai SSE is down -0.53%. Singapore Strait Times is down -0.08%. Japan 10-year JGB yield is up 0.022 at 2.547. Overnight, DOW rose 0.19%. S&P 500 rose 0.19%. NASDAQ rose 0.10%. 10-year yield rose 0.04 to 4.41.

Silver’s $6 Surge May Be the Start of a FOMO Phase

Silver’s explosive rally may be entering a new phase as investors abandon hopes for a pullback and begin chasing momentum instead. The metal’s breakout above the critical 84.21–84.46 resistance zone, combined with a collapsing Gold-Silver Ratio and persistent global supply deficits, is fueling speculation that the rally could accelerate further toward 92.90. Read More.

BoJ Summary Shows Growing Support for Near-Term Rate Hike

The BOJ’s April meeting summary revealed a noticeably more hawkish debate inside the board, with several policymakers openly discussing the possibility of another rate hike as the Iran-driven oil shock lifts inflation risks. Markets are increasingly pricing a potential move as early as June. Read More.

Australia NAB Survey Shows Cost Growth Jumps to 4.5% as Margin Squeeze Intensifies

Australia’s April NAB survey painted an increasingly stagflationary picture as purchase cost growth surged to 4.5% following the Middle East energy shock. While firms continued facing rising input costs, weaker trading, employment, and activity indicators suggested margin pressure is beginning to weigh more heavily on the broader economy. Read More.

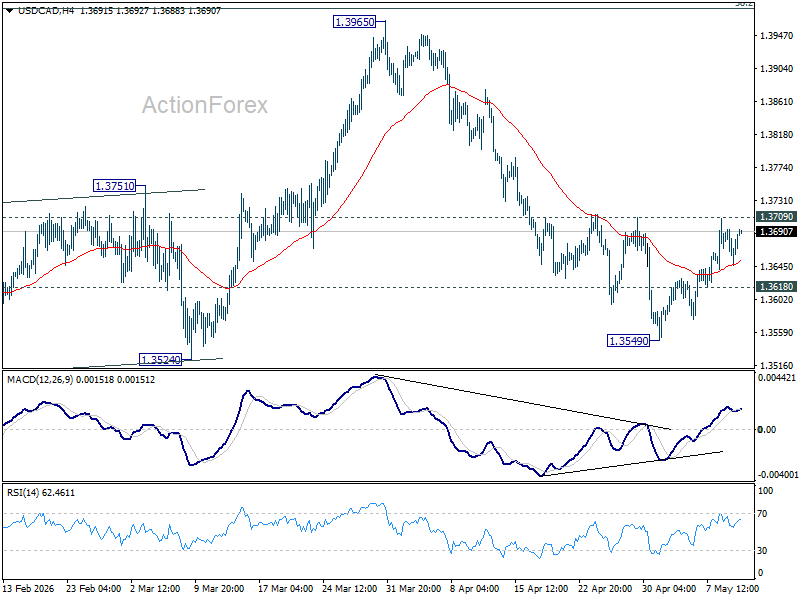

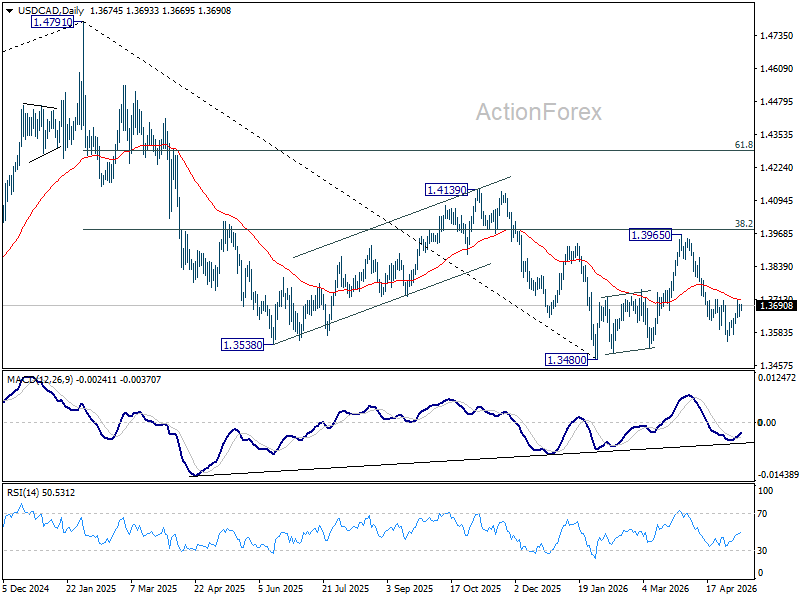

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3650; (P) 1.3672; (R1) 1.3697; More…

Intraday bias in USD/CAD remains neutral for the moment. On the downside, below 1.3618 minor support will suggest that recovery fro 1.3549 has completed, and turn intraday bias back to the downside. Break of 1.3549 will bring retest of 1.3480 low. However, sustained break of 1.3709 will confirm short term bottoming. Intraday bias will be back on the upside for 1.3965 resistance again, as in the third leg of the corrective pattern from 1.3480.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more

Gyrostat May Market Outlook: When The Cost Of Protection Falls - Signals For Portfolio Positioning

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. It... Read more

The Risk Most Portfolios Do Not Explicitly Manage

Most portfolios are constructed on a simple and widely accepted assumption: that equity risk will be r... Read more

Gyrostat April Outlook: The Changing Cost Of Protection

Signals For Portfolio Construction This monthly Gyrostat Risk-Managed Market Outlook does not attemp... Read more

What Advisers Misunderstand About Protection

Protection is rarely rejected outright. More often, it is misunderstood. Most advisers recognise th... Read more

Gyrostat Market Outlook: Looking Beyond The 30-day Volatility Headlines

This outlook examines how financial markets are pricing risk rather than attempting to forecast market... Read more