Markets Shift To Trust But Verify Mode After Trump Pause Meets Iran Denial

Markets shifted into a “trust but verify” mode as sharp volatility unfolded following a sudden geopolitical pivot. Initial optimism surged after US President Donald Trump announced a pause in planned strikes against Iranian energy infrastructure, but gains were quickly tempered as Iran denied any direct or indirect talks, raising doubts over the credibility of the de-escalation narrative.

The initial trigger for the rally came from Trump’s statement that “very good and productive conversations” had taken place, leading to a decision to postpone “any and all military strikes” for a five-day period. The announcement marked a sharp reversal from the earlier 48-hour ultimatum that had threatened immediate escalation if the Strait of Hormuz was not reopened.

Markets reacted aggressively to the perceived de-escalation. Brent crude briefly plunged to as low as 96, reflecting a rapid unwinding of war risk premium. Gold rebounded sharply to 4,463 after nearly breaking through the key 4,000 psychological level, while US equity futures surged, with DOW futures at one point up around 1,300 points.

However, the relief rally proved short-lived. Iranian media reports quickly pushed back against the US narrative, stating there had been no direct or indirect communication with Washington. This introduced a critical layer of uncertainty, suggesting that the “productive conversations” cited by Trump may have involved only intermediaries rather than a genuine diplomatic breakthrough.

The market reaction to this credibility shock was swift. Oil prices reversed sharply, with Brent climbing back above 105, while equity futures surrendered roughly half of their earlier gains. The rapid reversal highlights how fragile sentiment remains, with positioning highly sensitive to headline risk.

At its core, the market is grappling with a widening credibility gap. While the pause in military action reduces immediate escalation risk, the absence of confirmed dialogue raises questions about whether a meaningful resolution is underway. This has left investors reluctant to fully embrace the relief rally.

Importantly, the underlying structural risks remain unchanged. The Strait of Hormuz continues to face severe disruption, a critical concern given that roughly 20% of global oil flows pass through the chokepoint. Until shipping conditions normalize, the energy shock—and its inflationary consequences—will continue to weigh on global markets.

Meanwhile, governments are already preparing for a prolonged crisis. In the UK, Prime Minister Keir Starmer convened an emergency “Cobra” meeting to address the economic fallout, including rising borrowing costs and cost-of-living pressures. This signals that the conflict is increasingly feeding into domestic policy responses across major economies.

In Asia, the situation is being viewed as a regional crisis. With around 80% of oil shipments through Hormuz destined for Asian markets, economies such as Japan and South Korea remain particularly vulnerable. This helps explain the persistent underperformance of Asia-linked assets and currencies.

In currency markets, the picture remains mixed but consistent with a cautious tone. Australian Dollar continues to lead losses, followed by New Zealand Dollar and Swiss Franc. Yen is the strongest performer, reflecting safe-haven demand, while Sterling and Dollar are also supported. Euro and Canadian Dollar are trading in the middle as markets await clearer signals.

For now, markets remain trapped between optimism and uncertainty. The pause in military action offers temporary relief, but without confirmation of genuine diplomatic progress, sentiment is likely to stay fragile. Until the situation in the Strait of Hormuz is resolved, markets are likely to remain highly reactive, with “trust but verify” defining the near-term outlook.

In Europe, at the time of writing, FTSE is up 0.19%. DAX is up 1.87%. CAC is up 1.43%. UK 10-year yield is down -0.053 at 4.887. Germany 10-year yield is down -0.054 at 2.998. Earlier in Asia, Nikkei fell -3.48%. Hong Kong HSI fell -3.54%. China Shanghai SSE fell -3.63%. Singapore Strait Times fell -2.17%. Japan 10-year JGB yield rose 0.054 to 2.323.

Gold rebounds on TACO-driven de-escalation as 4,000 support holds

Gold’s sharp selloff stalled at the 4000 support zone before rebounding on a sudden policy reversal from Washington. The TACO-driven pause in planned Iran strikes has eased immediate escalation risks, but with yields still elevated, the move may prove to be a temporary stabilization rather than a confirmed bottom. Read more.

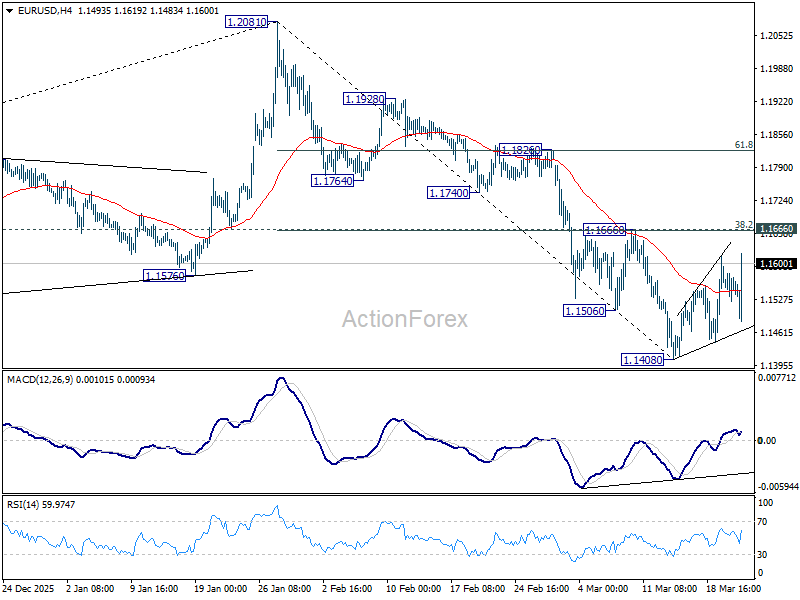

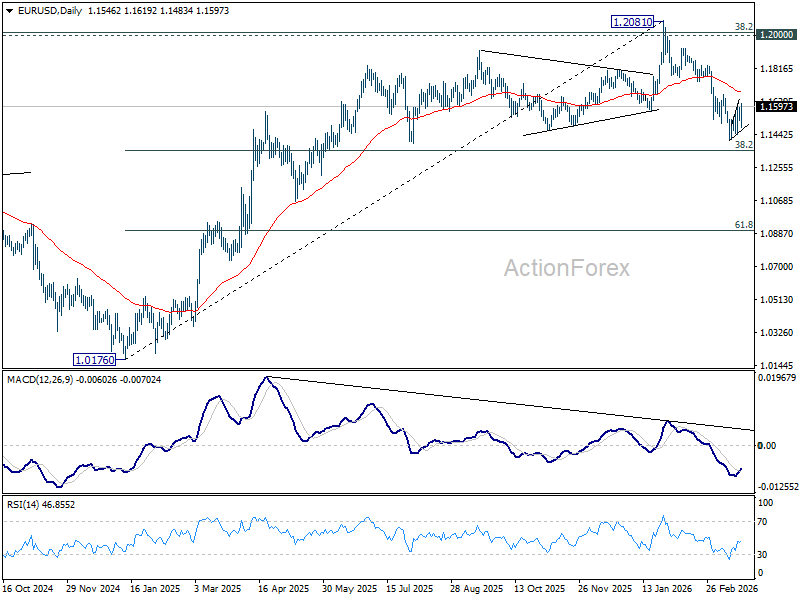

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1532; (P) 1.1565; (R1) 1.1605; More….

EUR/USD rebound from 1.1408 extended higher today but upside is still capped below 1.1666 cluster resistance (38.2% retracement of 1.2081 to 1.1408 at 1.1665). Intraday bias stays neutral and further decline remains in favor. On the downside, below 1.1408 will resume the fall from 1.2081 to 38.2% retracement of 1.0176 to 1.2081 at 1.1353. However, decisive break of 1.1666 will argue that the fall from 1.2081 has completed, and turn bias back to the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824.

In the bigger picture, prior break of 55 W EMA (now at 1.1501) should confirm rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. Deeper fall is expected to long term channel support (now at 1.0528). Meanwhile, risk will stay on the downside as long as 1.2081 holds, even in case of strong rebound.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more