Markets Enter Countdown Mode As US Ultimatum Raises Escalation Risks, AUD Leads FX Losses

Global markets are entering a critical countdown as tensions between the US, Israel, and Iran escalate ahead of a looming deadline. US President Donald Trump’s 48-hour ultimatum has introduced a clear timeline for military action, shifting market dynamics toward event-driven positioning and heightened volatility.

Asian markets have reacted most sharply to the developments. South Korea’s KOSPI dropped more than -6%, while Japan’s Nikkei fell around -4%, reflecting both direct and indirect exposure to the unfolding crisis. US equity futures are also under pressure, though declines remain less severe.

The primary driver remains the risk of a sustained energy shock. With the Strait of Hormuz still constrained, the ultimatum has forced markets to consider the possibility of a prolonged disruption to global oil flows. This has intensified inflation concerns and reinforced expectations of a higher-for-longer interest rate environment.

Iran’s counter-threat has broadened the scope of risks. By signaling possible attacks on energy and water infrastructure across the Gulf, Tehran has raised the prospect of systemic disruption extending beyond oil supply. This introduces a wider range of economic consequences, from energy shortages to industrial slowdowns.

A particularly notable development is the emergence of financial risk as a direct channel. Iran’s warning targeting holders of US Treasuries has unsettled Asian sovereign investors, highlighting vulnerabilities within global capital flows. This has added a extra uncertainty, linking geopolitical escalation to financial stability concerns.

The regional impact is especially pronounced in East Asia. Countries such as Japan and South Korea face dual exposure through energy dependence and financial integration. Even with significant oil reserves, the possibility of a prolonged blockade is driving defensive positioning and accelerating equity market declines.

At the same time, supply chain disruptions are beginning to surface. Delays in critical materials used in semiconductor manufacturing, including helium and etching chemicals, are raising concerns about the continuity of AI-related production. This has contributed to heavy selling in technology sectors across East Asia.

Currency markets are reflecting a similar picture. Australian and New Zealand Dollars are underperforming at the bottom. Meanwhile, Dollar and Canadian Dollar are benefiting from a combination of safe-haven demand and energy-linked support, while Yen and European currencies are sitting in the middle of the performance board.

With the ultimatum set to expire at 23:44 GMT Monday, markets face a binary event risk. A military strike could trigger a sharp escalation and broader market dislocation, while any delay may offer only temporary relief. Until then, investors are likely to remain cautious, with positioning driven by the potential for rapid shifts in both geopolitical and macro conditions.

In Asia, at the time of writing, Nikkei is down -3.47%. Hong Kong HSI is down -3.94%. China Shanghai SSE is down -3.75%. Singapore Strait Times is down -2.29%. Japan 10-year JGB yield is up 0.042 at 2.310.

Silver may find floor at 60, but break risks deeper fall to 50

Silver’s correction is approaching a critical stage as macro pressure builds and key supports come into focus. While 60 may provide a floor supported by industrial demand, a break could trigger a deeper move toward 50, shifting the balance from fundamentals to technical liquidation. Read more.

Stagflation test begins: PMIs to reveal growth shock and rising costs

Markets enter a critical phase as attention shifts from pricing an energy shock to testing its real economic impact. With oil disruptions intensifying, this week’s CPI and global PMIs will determine whether stagflation is already taking hold. The results could reinforce policy divergence—or trigger a broader reassessment of growth risks and central bank paths. Read More.

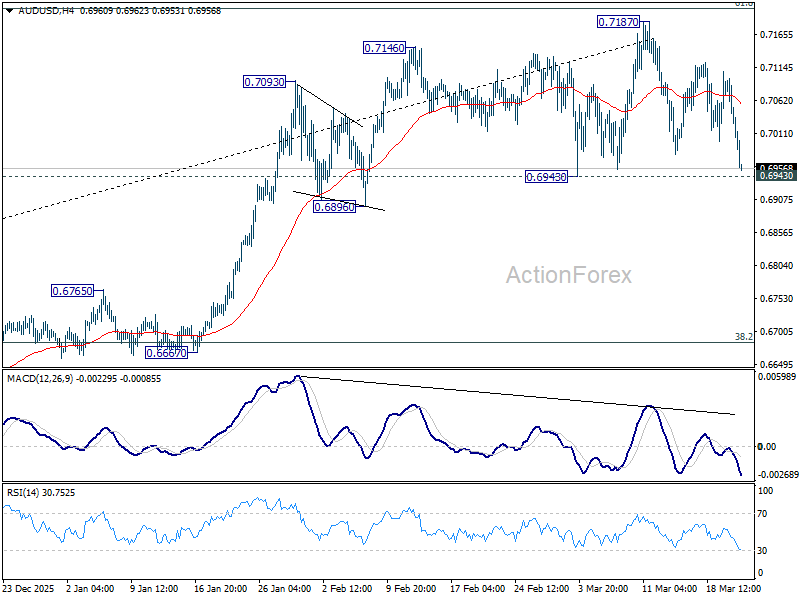

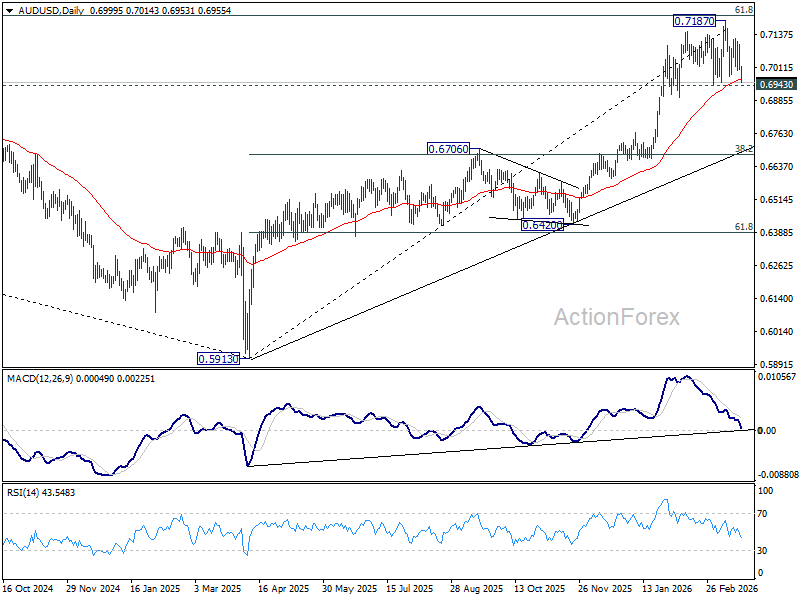

AUD/USD Daily Report

Daily Pivots: (S1) 0.6986; (P) 0.7042; (R1) 0.7080; More...

Immediate focus in now on 0.6943 support in AUD/USD. Decisive break there should confirm rejection by 0.7206 key fibonacci resistance. That would set up deeper correction to the whole up trend from 0.5913, and target 38.2% retracement of 0.5913 to 0.7187 at 0.6700. Nevertheless, strong rebound from current levels would retain near term bullishness for breakout through 0.7187 at a later stage.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will pave the way back to 0.8006. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more