Markets Calm As U.S.–China Trade Tensions Simmer, Frances Political Reprieve Lifts Sentiment

Global markets traded with a steady and cautious tone today, as investors balanced persistent U.S.–China trade tensions with signs of easing political risk in Europe.

Despite the looming November 1 deadline for Washington’s threatened 100% tariffs on Chinese imports, traders appeared hopeful for de-escalation, judging that both sides have incentives to avoid a severe disruption before year-end. Volatility has eased slightly after a turbulent start to the week, reflecting a shift toward defensive but stable positioning. Still, rhetoric from U.S. officials remains uncompromising. Treasury Secretary Scott Bessent told CNBC that the administration would not alter its negotiating stance toward Beijing, regardless of market swings.

In Europe, however, a measure of political stability returned after a tense week in Paris. French Prime Minister Sébastien Lecornu, reinstated after his brief resignation, announced that the government would suspend President Emmanuel Macron’s pension reform—the signature measure to raise the retirement age from 62 to 64—until January 2028. The decision represents a major concession aimed at restoring unity and calming public discontent.

Lecornu also promised not to bypass parliament on the 2026 budget, in a bid to win Socialist Party support ahead of Thursday’s no-confidence votes. With this compromise, markets now see the government’s survival as likely. The prospect that France’s cost-cutting budget will pass has helped revive investor confidence.

In currencies, Aussie continues to outperform, followed by Dollar and Euro. Loonie remains the weakest for the week, trailed by Yen and Swiss Franc. Sterling and Kiwi are trading mid-pack.

In Europe, at the time of writing, FTSE is down -0.41%. DAX is down -0.11%. CAC is up 2.22%. UK 10-year yield is down -0.036 at 4.553. Germany 10-year yield is down -0.024 at 2.587. Earlier in Asia, Nikkei rose 1.76%. Hong Kong HSI rose 1.84%. China Shanghai SSE rose 1.22%. Singapore Strait Times rose 0.32%. Japan 10-year JGB yield fell -0.007 to 1.656.

Eurozone industrial output drops -1.2% in August, Germany down -5.2%

Eurozone industrial production fell -1.2% mom in August, a smaller decline than the expected -1.8%. The data from Eurostat showed broad-based declines across key sectors, with capital goods output down -2.2%, durable consumer goods down -1.6%, energy production falling -0.6%, and intermediate goods slipping -0.2%. Only non-durable consumer goods managed a slight gain of 0.1%,.

Across the European Union as a whole, industrial output fell -1.0% mom. The regional breakdown showed significant divergence among member states: Germany, the bloc’s industrial powerhouse, suffered a sharp -5.2% decline, followed by Greece (-4.5%) and Austria (-3.1%), reflecting ongoing weakness in Europe’s core. Meanwhile, Ireland (+9.8%), Luxembourg (+4.8%), and Sweden (+3.6%) recorded the strongest gains.

RBA’s Hunter: Economy holding up, inflation still persistent in some areas

RBA Assistant Governor Sarah Hunter said in a speech on Tuesday that recent data suggest the Australian economy has been performing slightly stronger than expected, reinforcing the Bank’s decision to keep the cash rate unchanged at 3.60% at its September meeting. She noted that the RBA continues to see signs that “private demand is recovering,” “inflation may be persistent in some areas,” and that labor market conditions remain “stable.”

Hunter highlighted that GDP grew 1.8% over the year to the June quarter. “If anything, outcomes have been a little stronger than those expected in the August SMP,” she said, citing resilient private spending and steady employment as evidence that the economy remains on firmer footing than previously anticipated.

She also pointed to high-frequency indicators showing that underlying inflation in the September quarter is likely to be stronger than anticipated, suggesting that economic and labor market conditions remain “a bit tighter than we had assessed.” However, she acknowledged that employment growth has slowed “slightly” more than expected, while “elevated” global uncertainty continues to cloud the outlook.

Hunter concluded that the RBA will “continually reassess” its view on the economy and adjust policy as appropriate.

China’s CPI still negative at -0.3% in September as food prices drag

China’s consumer inflation remained in negative territory in September, highlighting continued weakness in domestic demand even as underlying price pressures showed tentative signs of improvement. Headline CPI rose from –0.4% yoy to –0.3% yoy, missing expectations of –0.2% yoy.

The National Bureau of Statistics said lower food and energy prices were the main contributors to the decline, with food prices down -4.4% yoy and consumer goods prices falling -0.8% yoy, partly offset by a 0.6% yoy increase in service prices.

However, the data also showed hints of stabilization beneath the surface. Core CPI, which excludes food and energy, rose 1.0% yoy from a year earlier, its highest level since February 2024, suggesting that domestic price momentum is slowly recovering in service sectors and other non-food categories.

Meanwhile, factory-gate prices continued to contract, with PPI rising from –2.9% yoy to –2.3% yoy, in line with expectations. This marks the 36th consecutive month of producer deflation, underscoring persistent cost pressures in manufacturing. NBS statistician Dong Lijuan said recent capacity management efforts in several industries have helped narrow the pace of decline, noting that market competition has improved as industrial supply and demand slowly rebalance.

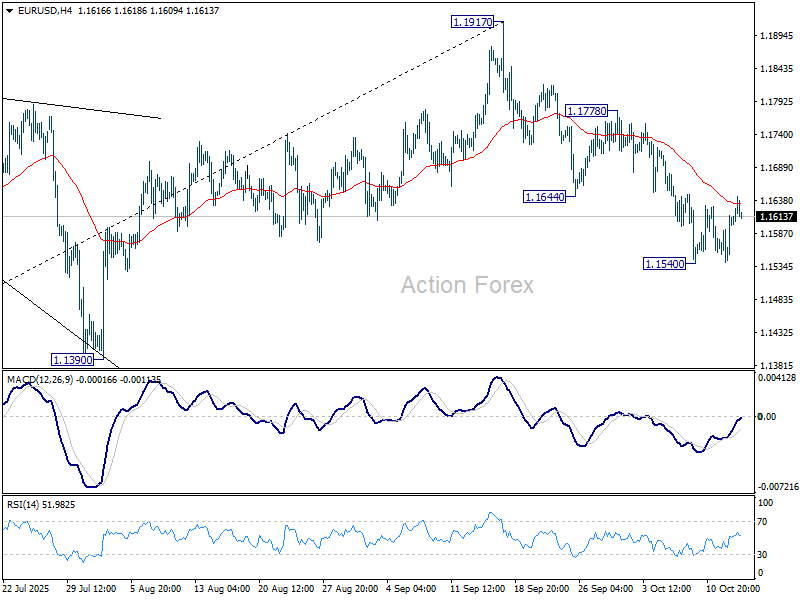

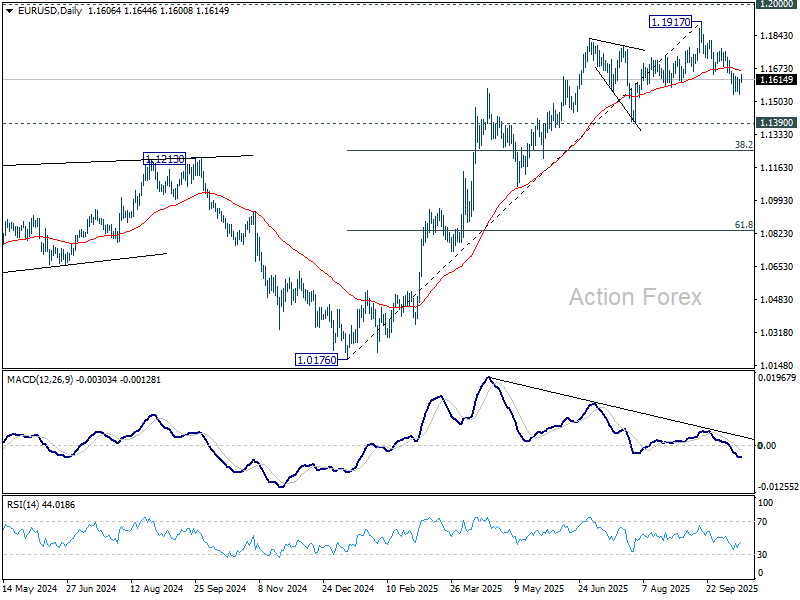

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1562; (P) 1.1588; (R1) 1.1634; More…

EUR/USD recovers mildly today as consolidations continue. Intraday bias remains neutral first. Deeper decline is expected as long as 1.1778 resistance holds. On the downside, break of 1.1540 will resume the fall from 1.1917 to 1.1390 , or further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1274) holds, the up trend from 0.9534 (2022 low) is still extended to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more