Markets Aggressively Price US-Iran Deal As Hormuz Reopens, Oil And Dollar Fall

Dollar tumbles again in early US session as oil prices dive on fresh geopolitical progress. A sharp selloff has pushed WTI back toward the mid-$80s and Brent into the low-$90s. The move reflects increasingly aggressive positioning ahead of the second round of US-Iran talks, with markets no longer waiting for confirmation but actively pricing a breakthrough.

The trigger was a key development out of Tehran. Iranian Foreign Minister Abbas Araghchi announced that the Strait of Hormuz is “completely open” for commercial shipping “in line with ceasfire in Lebanon. The move removes one of the most critical risk points in global energy supply and is being interpreted as a clear step toward de-escalation.

With key logistical risks easing, traders are leaning more confidently into a de-escalation scenario. The sequence is becoming clearer: open shipping lanes, sustained ceasefire, then formalized negotiations. In that context, the collapse in oil prices is not just a reaction—it is a forward-looking repricing of a normalization outcome.

At the same time, expectations for the talks have become more realistic—and more achievable. Rather than aiming for a full peace deal, both sides are now expected to settle for an interim memorandum or framework agreement. That shift lowers the threshold for success, increasing the likelihood that negotiations deliver a market-friendly outcome.

Meanwhile, Yen is also under broad-based pressure, but for very different reasons. Markets are expressing clear dissatisfaction with the lack of guidance from BoJ Governor Kazuo Ueda. Despite having a high-profile platform following IMF meetings, Ueda refrained from signaling any imminent policy shift this month, instead reiterating a data-dependent stance.

His comments—that inflation could rise with oil but fall if growth slows, and that decisions will be made “meeting by meeting”—were seen as overly open-ended. Markets had expected at least some forward guidance, especially given the BoJ’s past pattern of subtly preparing markets ahead of policy changes. The absence of such signaling is now being interpreted as inertia.

Still, it would be premature to fully rule out policy action. The BoJ has a history of surprising markets, and the current silence does not preclude a rate hike at upcoming meetings. But for now, the lack of direction is weighing on Yen, pushing it alongside Dollar at the bottom of the weekly performance table.

In contrast, pro-cyclical currencies remain firmly in control. Aussie continues to lead gains, supported by both global risk sentiment and domestic strength, followed by Loonie and Kiwi. Euro and Swiss Franc are holding mid-pack, reflecting a more neutral positioning.

In Europe, at the time of writing, FTSE is down -0.05%. DAX is up 0.72%. CAC is up 0.57%. UK 10-year yield is down -0.184 at 4.653. Germany 10-year yield is down -0.068 at 2.965. Earlier in Asia, Nikkei fell -1.75%. Hong Kong HSI fell -0.89%. China Shanghai SSE fell -0.10%. Singapore Strait Times fell -0.20%. Japan 10-year JGB yield rose 0.015 to 2.420.

BoE’s Breeden Says Risks Often Underestimated Before Crises

BoE’s Sarah Breeden warns that while the financial system is more resilient, risks from leverage and complexity are re-emerging and could trigger instability. Read more.

EU Exports to US Drop 26.4% YoY in February, Down 16.1% to China

EU exports dropped sharply in February, with shipments to the US and China falling significantly, signaling weakening global demand. Read more.

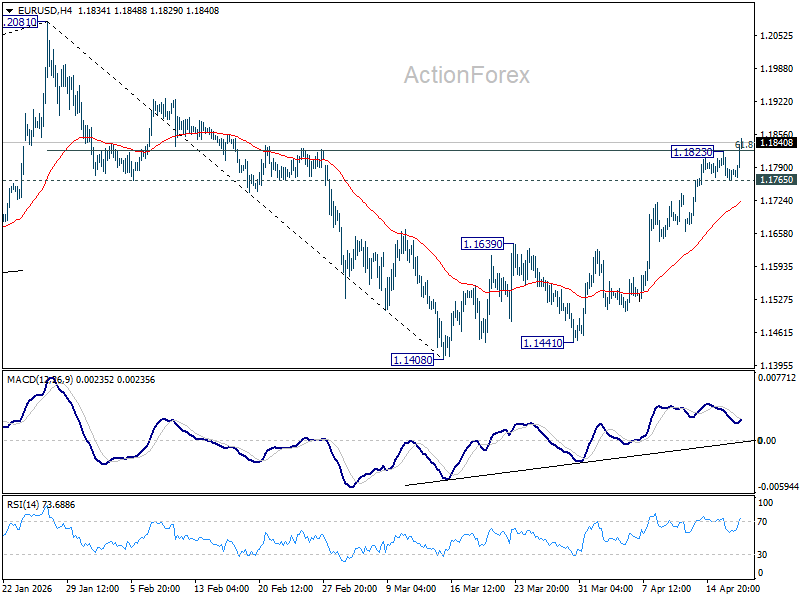

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1758; (P) 1.1792; (R1) 1.1817; More….

EUR/USD’s rally resumed after brief consolidations and intraday bias is back on the upside. Sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will extend the rally from 1.1408 to retest 1.2081 high. On the downside, below 1.1765 minor support will turn intraday bias neutral again first.

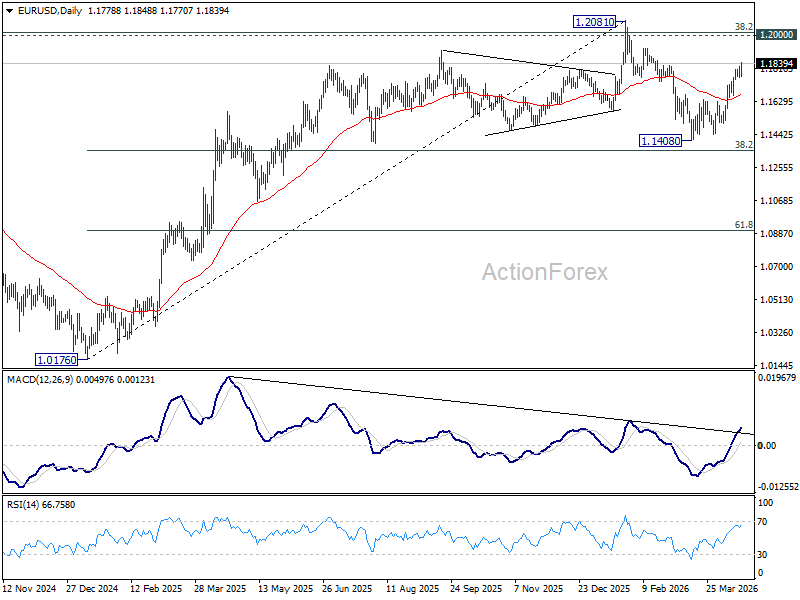

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1513). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more