Market Trepidation Over Chinese Data, Dollar Marches On

Prevailing mood of risk aversion was evident in Asian session today. Hong Kong stocks led the region lower, reflecting investors’ dissatisfaction with the latest batch of Chinese economic data. While China’s Q4 GDP growth wasn’t far off from analysts’ expectations, it still fell short for some, contributing to the market’s cautious stance. Additionally, concerns were heightened by the weak retail sales growth and China’s continuing population shrinkage, underscoring deeper economic challenges. Japan’s Nikkei index stood out as the only exception, remaining relatively stable.

In the currency markets, Dollar is standing out as the best performer for the week so far. The prevailing risk-off sentiment is providing sustained boost to the greenback. Concurrently, reports have surfaced, mentioning an “extreme scenario” where no major central bank might cut interest rates this year. This perspective, highlighted by a Bank of America FX strategist, brings into question the potential scenario where central banks remain on hold due to persistent inflation and ongoing robust economic growth. That’s a stark contrast to current market pricing that suggests six Fed cuts this year, which is also “unrealistic” at the other end.

Australian and New Zealand Dollars are facing considerable pressure, primarily due to their economic linkages with China. Japanese Yen, too, is among the weaker currencies at the moment. On the flip side, Canadian Dollar and Euro are showing some resilience, with Canadian Dollar being the second strongest. Sterling and Swiss Franc are showing mixed performances, with the Pound particularly focused on the upcoming UK CPI data, which could provide further direction.

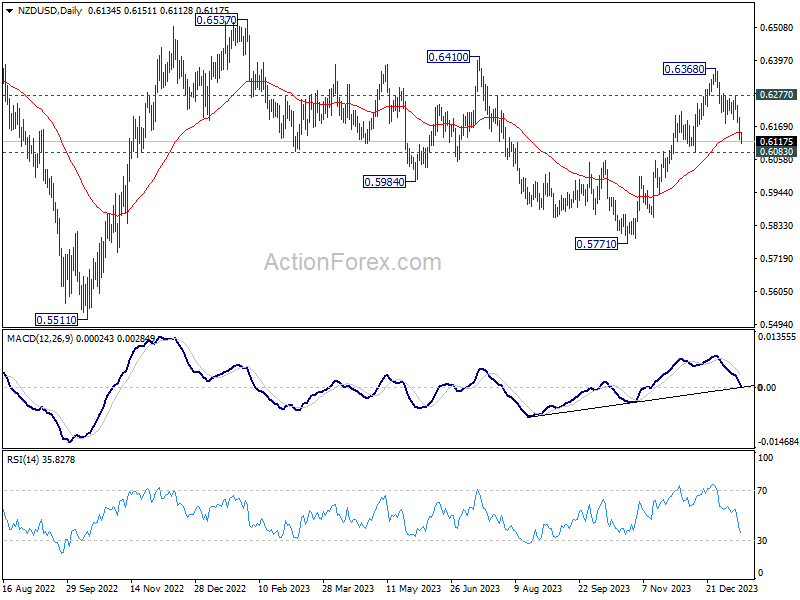

Technically, focus is now on 0.6083 support after this week’s decline in NZD/USD. Firm break there will argue that rebound from 0.5771 has completed at 0.6368 already. More importantly that would argue that whole corrective pattern from 0.6537 is still in progress. Deeper fall would be seen towards 0.5771 support. On other hand, stronger rebound from 0.6083, followed by break of 0.6277 resistance, will retain near term bullishness for a test on 0.6537 high next.

In Asia, Nikkei closed down -0.22%. Hong Kong HSI is down -3.31%. China Shanghai SSE is down -0.98%. Singapore Strait Times is down -1.06%. Japan 10-year JGB yield is up 0.0123 at 0.610. Overnight, DOW fell -0.62%. S&P 500 fell -0.37%. NASDAQ fell -0.19%. 10-year yield rose 0.0116 to 4.066.

Fed’s Waller anticipates rate cuts this year, stresses upcoming CPI revisions

Fed Governor Christopher Waller expressed growing confidence bring inflation down to target. He noted in a speech overnight that Fed is “within striking distance of achieving a sustainable level of 2 percent PCE inflation”. However, he also emphasized the need for more data in the coming months to confirm or challenge the notion that inflation is moving sustainably toward Fed’s goal.

Waller also mentioned that he perceives the risks to employment and inflation mandates as “more closely balanced” now. His focus is on watching for sustained progress on inflation and a modest cooling in the labor market.

Regarding interest rate cuts, Waller expressed that “as long as inflation doesn’t rebound and stay elevated”, he believes Fed will be able to lower the target range for the federal funds rate “this year”. But he also clarified, “Clearly, the timing of cuts and the actual number of cuts in 2024 will depend on the incoming data.”

Waller also highlighted the importance of the upcoming revisions to CPI inflation scheduled for next month. He recalled that last year’s annual update to the seasonal factors reversed what initially appeared to be a decline in inflation. The January CPI report and revisions for 2023, due in mid-February, are anticipated to potentially alter the current understanding of inflation. Waller expressed hope that these revisions would confirm the progress observed so far but emphasized that good policy must be based on data rather than hope.

ECB’s Simkus and Müller urge caution over aggressive rate cut expectations

ECB Governing Council Gediminas Simkus expressed a conditional optimism about rate reductions within the year, stating, “If we don’t see any surprises that would change the data and the thinking, I’m positive about rate cuts this year.”

However, Simkus tempered his outlook with a dose of realism regarding the timing of these cuts. He clarified, “I’m far less optimistic than markets about rate cuts in March or April.”

Separately, another Governing Council member Madis Müller commented on the aggressiveness of market expectations for ECB rate cuts in 2024. He observed that these expectations do not align with the current data available to the central bank.

Müller further emphasized that wage growth in Eurozone remains out of sync with the ECB’s current inflation targets. He noted that ECB cannot proceed with cutting rates until data reflects the desired price growth conditions.

China’s 2023 economic growth at 5.2%, population shrinks for second year

China’s GDP grew 5.2% yoy in Q4, an uptick from Q3’s 4.9% yoy. For the full year of 2023, the economy also recorded a growth rate of 5.2%. On a quarter-by-quarter basis, GDP growth rate was 1.0% qoq, matched expectation, though this marked a slowdown from the previous quarter’s revised 1.5% qoq gain.

In the industrial sector, production rose by 6.8% yoy in December, slightly higher than the previous month’s 6.6%, meeting market forecasts. However, retail sales growth decelerated to 7.4% yoy, a drop from November’s 10.1% yoy and below the expected 8.1% yoy.

Investment patterns showed a mixed trend. Overall fixed asset investment in 2023 grew by 3.0%, slightly exceeding the 2.9% expectation. Within this category, real estate investment saw a significant drop of -9.6%. Conversely, investment in infrastructure and manufacturing rose by 5.9% and 6.5%, respectively, signaling growth in these areas.

Amidst these economic developments, China faces a demographic challenge as its population fell for the second consecutive year in 2023. Total population decreased by -2.75m to 1.409B, a more rapid decline than in 2022.

Looking ahead

UK CPI data is the main focus in European session while Eurozone will publish CPI final too. Later in the day, US retail sales will catch most attention. US import price, industrial production, business inventories and NAHB housing index will also be released. Fed will release Beige Book economic report too.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6552; (P) 0.6608; (R1) 0.6641; More…

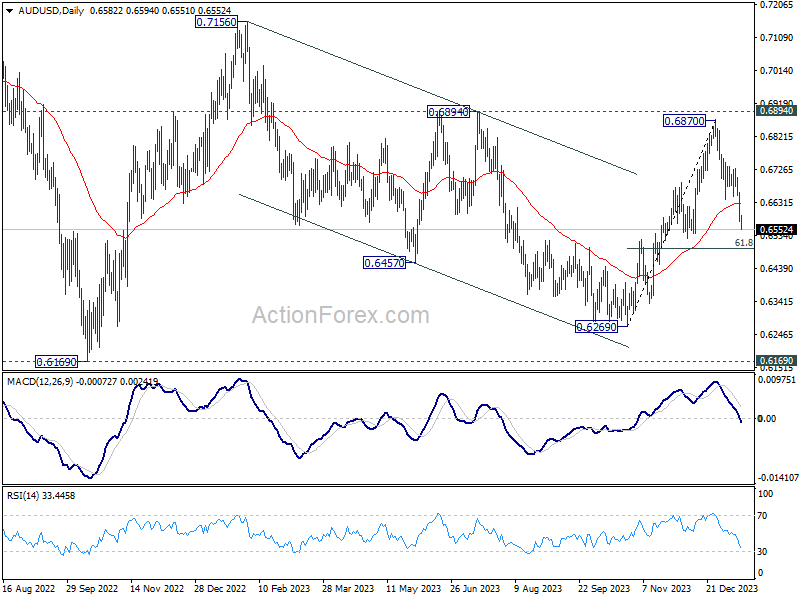

AUD/USD’s fall from 0.6870 continues today and intraday bias stays on the downside. Deeper fall would be seen to 61.8% retracement of 0.6269 to 0.6870 at 0.6497. Sustained break there will argue that whole rebound from 0.6269 has completed, and bring deeper fall to this support. On the upside, above 0.6632 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 02:00 | CNY | GDP Y/Y Q4 | 5.20% | 5.20% | 4.90% | |

| 02:00 | CNY | Industrial Production Y/Y Dec | 6.80% | 6.80% | 6.60% | |

| 02:00 | CNY | Retail Sales Y/Y Dec | 7.40% | 8.10% | 10.10% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Dec | 3.00% | 2.90% | 2.90% | |

| 07:00 | GBP | CPI M/M Dec | 0.20% | -0.20% | ||

| 07:00 | GBP | CPI Y/Y Dec | 3.80% | 3.90% | ||

| 07:00 | GBP | Core CPI Y/Y Dec | 4.90% | 5.10% | ||

| 07:00 | GBP | RPI M/M Dec | 0.40% | -0.10% | ||

| 07:00 | GBP | RPI Y/Y Dec | 0.40% | 5.30% | ||

| 07:00 | GBP | PPI Input M/M Dec | -0.70% | -0.30% | ||

| 07:00 | GBP | PPI Input Y/Y Dec | -1.90% | -2.60% | ||

| 07:00 | GBP | PPI Output M/M Dec | -0.20% | -0.10% | ||

| 07:00 | GBP | PPI Output Y/Y Dec | 0.40% | -0.20% | ||

| 07:00 | GBP | PPI Core Output M/M Dec | 0.00% | |||

| 07:00 | GBP | PPI Core Output Y/Y Dec | 0.20% | |||

| 10:00 | EUR | Eurozone CPI Y/Y Dec F | 2.90% | 2.90% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Dec F | 3.40% | 3.40% | ||

| 13:30 | CAD | Industrial Product Price M/M Dec | -0.70% | -0.40% | ||

| 13:30 | CAD | Raw Material Price Index Dec | -2.10% | -4.20% | ||

| 13:30 | USD | Retail Sales M/M Dec | 0.40% | 0.30% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Dec | 0.20% | 0.20% | ||

| 13:30 | USD | Import Price Index M/M Dec | -0.50% | -0.40% | ||

| 14:15 | USD | Industrial Production M/M Dec | -0.10% | 0.20% | ||

| 14:15 | USD | Capacity Utilization Dec | 78.70% | 78.80% | ||

| 15:00 | USD | Business Inventories Nov | -0.10% | -0.10% | ||

| 15:00 | USD | NAHB Housing Index Jan | 39 | 37 | ||

| 19:00 | USD | Fed’s Beige Book |

When The Wave Turns

Why Retirement Investing Is Moving Towards Resilience Jeremy Grantham’s latest market warnings have revived an old tru... Read more

Gyrostat Capital Management: July Retirement Portfolio Resilience Assessment

The Market Is Currently Presenting an Opportunity to Strengthen Retirement Portfolio Resilienc... Read more

The Invisible Risk That Decides Your Retirement

Why how investors behave matters more than what markets do and what disciplined port... Read more

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more