Loonie Rises On Strong Jobs Data, BoC Pressure Eases

Canadian Dollar strengthened notably in the early U.S. session after robust September employment data signaled that Canada’s economy was more resilient than anticipated in face of U.S. tariffs.. The upbeat data provided a welcome boost to the Loonie, which had already been one of the week’s top performers, and may prompt markets to reassess expectations for further rate cuts from the BoC later this month.

The strength of the report should ease pressure on the BoC ahead of its October 29 policy meeting. The central bank resumed rate cuts in September amid a softening labor market and persistent trade uncertainty, but the latest data point to renewed momentum, particularly in full-time employment and manufacturing. That may give policymakers room to pause and evaluate whether recent easing has already stabilized conditions.

The next major test will come from September CPI on October 21, which will help determine whether the recent easing has struck the right balance between supporting growth and containing inflation.

Meanwhile in Japan, political uncertainty returned to the spotlight as Sanae Takaichi’s premiership bid was thrown into doubt. The ruling LDP’s coalition partner Komeito announced its withdrawal from the alliance after disputes over the handling of a political funding scandal, ending a 26-year relationship. Komeito leader Tetsuo Saito said the party would not support Takaichi in the parliamentary vote expected later this month, leaving her leadership uncertain.

Takaichi called the decision “extremely regrettable,” vowing to continue efforts to form a government. The political split adds to the uncertainty surrounding Japan’s policy direction, particularly with Takaichi’s fiscally expansionary and dovish leanings toward monetary policy. Nonetheless, the Yen managed to stabilize, aided by verbal intervention from Japanese officials stressing that FX moves must reflect fundamentals.

Overall, Dollar remains the week’s strongest performer, followed by Loonie, which now has a chance to overtake if post-jobs momentum continues. Aussie remains third strongest. At the other end, Yen remains the weakest, with Euro and Sterling trailing just ahead. Swiss Franc and Kiwi are holding in the middle.

In Europe, at the time of writing, FTSE is up 0.03%. DAX is up 0.04%. CAC is up 0.01%. UK 10-year yield is down -0.062 at 4.687. Germany 10-year yield is down -0.031 at 2.671. Earlier in Asia, Nikkei fell -1.01%. Hong Kong HSI fell -1.73%. China Shanghai SSE fell -0.94%. Singapore Strait Times fell -0.30%. Japan 10-year JGB yield fell -0.001 to 1.696.

Canada jobs surge 60.4k in September, unemployment steady at 7.1%

Canada’s labor market delivered a strong upside surprise in September, with employment rising by 60.4k, well above expectations of just 2.8k. The gains were concentrated in manufacturing (+28k), health care and social assistance (+14k), and agriculture (+13k), while wholesale and retail trade saw a notable decline of -21k.

The report reinforces signs of resilience across key sectors even amid broader uncertainty over the impact of U.S. trade and tariff policies.

The data also showed a healthy quality of job growth, with full-time employment surging 106k while part-time positions dropped -46k, suggesting improved job stability.

Unemployment rate held steady at 7.1%, defying expectations for a modest uptick to 7.2%. Wage growth also firmed slightly, with average hourly earnings up 3.3% yoy, from 3.2% yoy in August.

Japan producer prices hold at 2.7% as import declines ease in September

Japan’s corporate goods price index rose 2.7% yoy in September, unchanged from August and slightly above expectations of 2.5%. The data suggest that while upstream cost pressures remain contained, they have yet to fade meaningfully.

Yen-based import price index declined -0.8% yoy, a much smaller drop than August’s -3.9%, pointing to easing import deflation as Yen’s weakness and rising global input costs filter through.

In terms of components, food and beverage prices climbed 4.7% yoy, following a 4.9% in August. Agricultural goods prices, including rice, jumped 30.5%, moderating from August’s 41% surge.

RBA’s Bullock: Inflation back in band but services still sticky, jobs market tight

RBA Governor Michele Bullock told lawmakers today that the economy is in a “pretty good spot,” with inflation back within the 2–3% target band and the labor market still tight. Speaking before a parliamentary committee in Canberra, she said, “the key now is to make sure it stays there sustainably.”

She said that services inflation remains the main concern, running “a little sticky” at around 3%, even as goods inflation continues to moderate. That offset has kept headline inflation contained for now.

On employment, Bullock said the labor market is in “a pretty good place”, though “possibly a little bit tight” in certain sectors. The RBA expects unemployment to edge higher over the coming months, a move consistent with a gradual rebalancing.

She also highlighted that household consumption is picking up, filling the gap left by weaker public demand—an important transition, she said, to keep growth on track.

NZ BNZ manufacturing flat at 49.9, firms cite soft demand and rising costs

New Zealand’s BNZ Performance of Manufacturing Index held steady at 49.9 in September, marking another month of contraction and remaining below its long-term average of 52.4.

The data highlighted a mixed picture across key components — production edged up from 47.8 to 50.1, barely returning to expansion, while employment dropped from 49.1 to 47.5, weighing on the overall index. New orders also slipped from 54.7 to 50.3, suggesting softening demand momentum.

BusinessNZ Director of Advocacy Catherine Beard said it was encouraging that the PMI did not show deeper contraction, but the sector remained “agonizingly close to returning to expansion mode.” She added weakness in employment prevented the headline figure from crossing the 50 threshold.

Survey respondents continued to highlight muted customer demand and rising cost pressures, with 60% of comments negative, up from August. Manufacturers reported lower order volumes, tight margins, and competitive pricing pressures, reflecting both domestic uncertainty and subdued export demand.

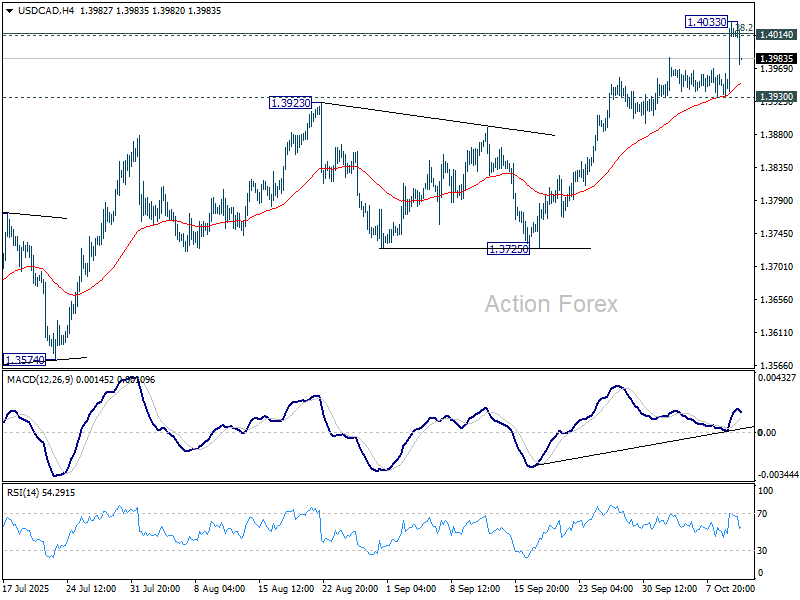

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3959; (P) 1.3996; (R1) 1.4059; More…

Intraday bias in USD/CAD is turned neutral again with current retreat. On the downside, firm break of 1.3930 support will indicate rejection by 1.4014/7 cluster resistance. That would keep the rebound from 1.3538 corrective, and turn bias to the downside for 1.3725 support. Nevertheless, sustained break of 1.4014/7 cluster resistance will suggest that USD/CAD Is already reversing the whole fall from 1.4719, and target 61.8% retracement at 1.4312.

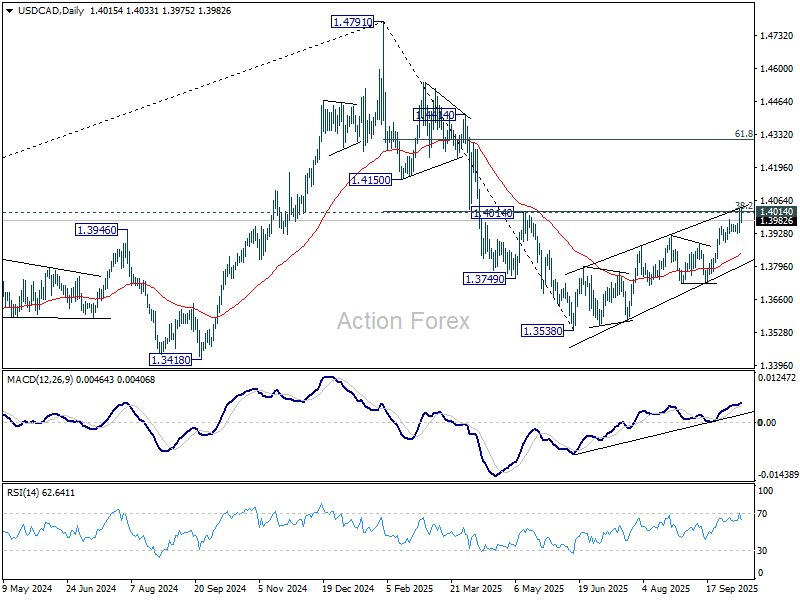

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. However sustained trading above 1.4014 will suggest that it’s more likely just a correction, and the larger up trend would be in favor to resume through 1.4791 at a later stage.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more