Just over a year since the former CEO (in)famously quit to "sit at the beach and do nothing", Jupiter Asset Management's CIO-turned-CEO Matthew Beesley presides over a firm that has been in the headlines arguably more than most would hope for.

During his tenure the firm has suffered through difficult results, the departure of anchor names Edward Bonham Carter and Richard Buxton, platforms restricting assets into its UK Mid Cap fund and the recent exit of chair Nicola Pease.

Jupiter chair Nichola Pease steps down

There have also been positive stories, including strong inflows to its institutional business and a warm industry reception to the firm's daily dealing unlisted assets ban.

Six months after joining, Beesley was thrust into the CEO position and wasted no time in reshaping the house. Some of this would come via the ‘fund rationalisation' process, while other elements have continued more quietly, particularly the growth of its lesser-known fixed income and European arms.

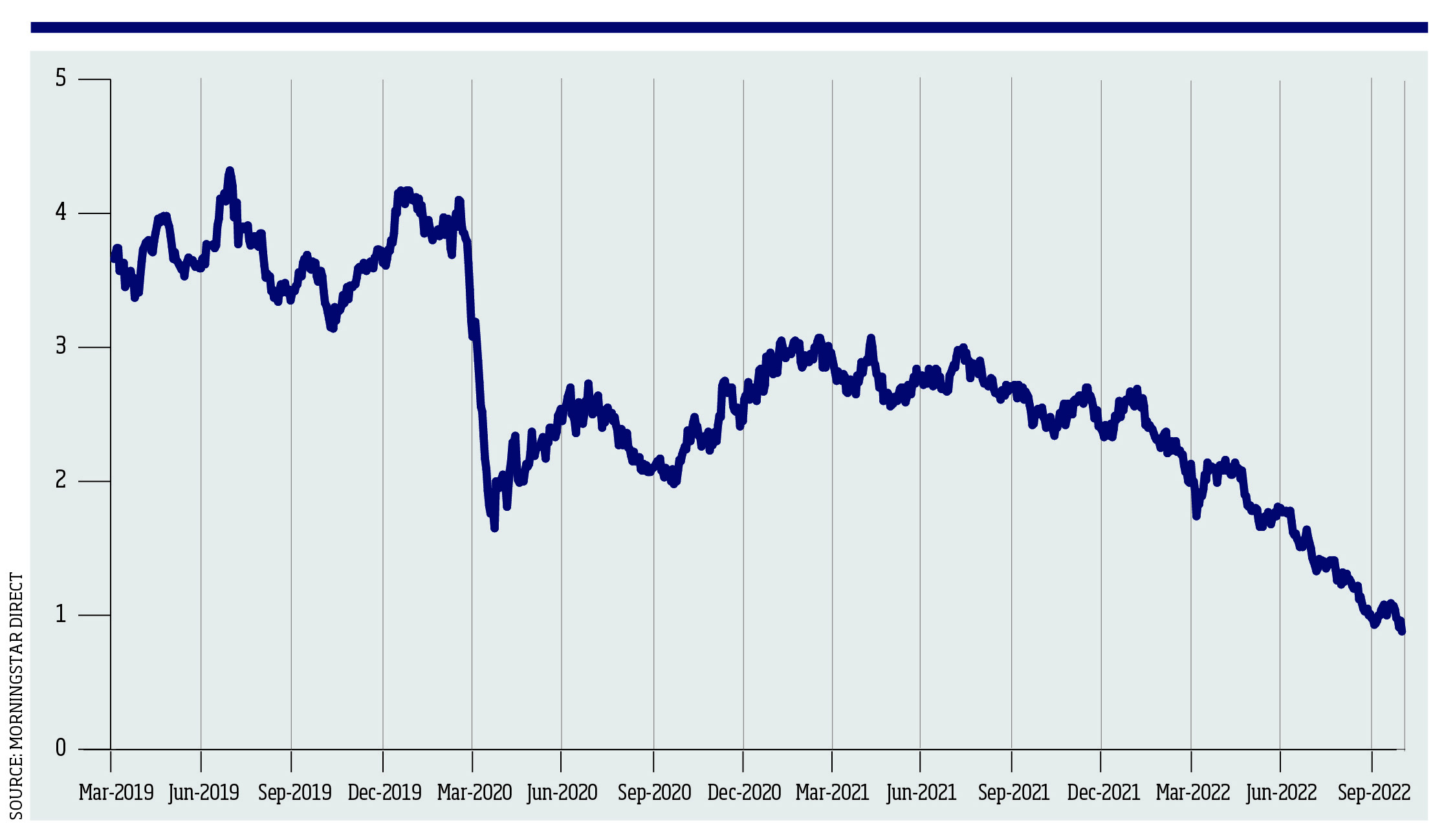

Over his predecessor Andrew Formica's tenure, Jupiter's share price plummeted an eye-watering 74.5%, according to data from Morningstar Direct.

Jupiter Asset Management's share price (£) under Andrew Formica (1 March 2019 - 30 September 2022)

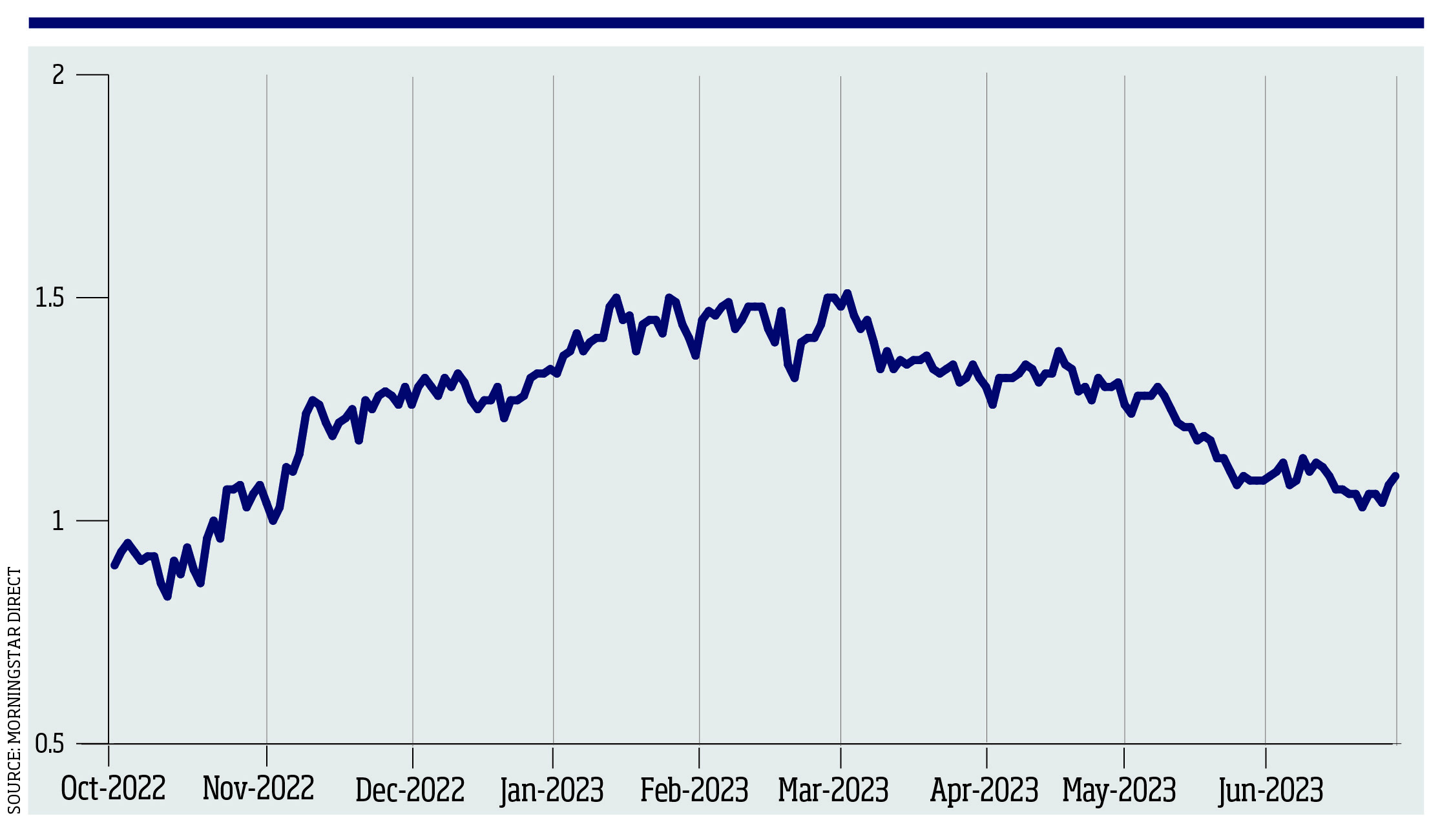

While the asset manager remains 42.1% below its IPO, as of 30 June 2023, Beesley's opening months have been met with a 25% share price foray into the black - not that this is where his focus lies.

Jupiter Asset Management's share price (£) under Matthew Beesley (1 October 2022 - 30 June 2023)

"We can't control the share price," Beesley explains. "What we can do as a management team is make sure we're doing the right thing, set this business up strategically on a multi-year view and know that, over time, shareholders will understand what it is we do.

"And the value of the business will increase if we make the right decisions and execute on that strategy in the right way."

Senior restructuring

Sitting alongside the CEO are the duo who have split the CIO role: head of equities Kiran Nandra-Koehrer and head of fixed income Matthew Morgan.

Nandra-Koehrer, who joined from Pictet Asset Management at the beginning of the year, now heads Jupiter's legacy asset class and found herself at the head of a team eager to make things happen in the new structure.

"The business has got behind [the CIO split] very quickly," she says. "It's been easy to get plugged in and I've had the opportunity to really sit down with all the investors.

"I was blown away by the depth and breadth of expertise across the floor."

Jupiter appoints head of equities as it pushes ahead with split CIO role

Beyond the talent in house, Nandra-Koehrer believes Jupiter's "huge focus" on active management is what sets the firm aside from its competitors.

"That's the standout for Jupiter, the focus on independent active management - especially when you've got the threat of passive, there is no room for benchmark huggers."

Morgan, who has been with the firm since April 2019, echoes much of his colleague's sentiments and reasserts the value of letting people get on with the job.

"We attract managers by giving them a great deal of independence," he explains. "We don't have a top-down CIO view and that means we can attract people who want that freedom - within the proper constraints, obviously."

Against a background of recession, rising rates, sticky inflation and widespread uncertainty, the trio firmly believe active management can offer investors something unique.

"A really simple fact about fixed income is that you get a little return for most of the things you invest in and the things that go wrong you lose all your money," Morgan jokingly explains is an exaggeration, but with some truth.

"In that great wave of central bank and government support after the Global Financial Crisis, everybody forgot the need for active management of things like your interest rate exposure.

"Last year showed you really need it, and I think the clients are going to want to be a lot more focused on exactly what's in their portfolio."

Absolute return's comeback

"The biggest thing [in fixed income] will be absolute return coming back," Morgan declares. "We have seen this in asset allocators and consultants scrambling to add absolute return to lists of managers they forgot about in the busier times."

Jupiter proposes merger of fixed income funds

He remains confident when questioned about the fate of some of the sector's best-known funds, names such as abrdn's GARS holding less than glowing reviews from some investors.

"Absolute return funds had a really tough time," he admits. "If an absolute return fund is there to give a cash-plus return and give you a fairly boring experience while protecting you from drawdown, if you have ten years of great returns for markets, investors are going to start to ask questions.

"But the last ten years has shown there was a period in which people forgot the need for diversification, and as long as people will listen to us, we will continue to bang the drum for the power of diversification.

"Look at what happened in 2022; the power of diversification is enormous."

A differentiated, active offering

If there's one thing Beesley wants Jupiter to be known for, it's active management. If there's a second thing, it's doing active management differently.

"Jupiter is very simple: we stand for being active managers," he says. "When clients consider the need for an active solution to a particular asset class challenge they have, and they want something that's going to be differentiated versus their peers, we want them to think about Jupiter."

Even when debating a venture into ETFs, active remains the key for Beesley, who reveals the firm is debating an active ETF iteration of its upcoming range of five thematic funds, which are set for a mutual fund launch later this year.

Jupiter changes benchmarks on two funds

On a company level, Beesley also remains actively focused and suggests the company shouldn't be averse to utilising some available capital to pursue inorganic growth that would supplement the current fund stable.

"There's nothing new that's coming soon," he confirms, "but we are absolutely thinking about the range of different things we could do to broaden that appeal to clients consistent with our stated strategic objectives."

Could such an acquisition supplement an LTAF proposition at the fund house?

"The LTAF structure is really interesting," Beesley admits. "As of today, we don't have investment capability that would naturally manufacture products to suit the LTAF structure.

"Could it be that our distribution capabilities and clout and knowledge and brand and reputation, pair well with an alternatives investor manufacturer in an LTAF structure? Could that be something of interest down the line? Potentially."

Fund rationalisation

Announced at the beginning of Beesley's tenure, ‘fund rationalisation' is a term that has probably defined his early days.

The programme was met with trepidation at first, with 25% of funds set to be merged, closed or repositioned a large figure in absolute terms.

However, as Beesley stated at the time and continues to reaffirm, this only targeted "subscale" funds, with most holding less than £100m in AUM.

Jupiter's unlisted assets ban hailed as 'positive move' for investors

The process is still on track to meet its roughly mid-2023 deadline, give or take some regulatory hurdles, the result of which will have seen around 25 of the 100 or so stable of Jupiter funds affected.

"What was really important is how little assets under management attrition this process has resulted in. Just 0.3% of total AUM has left us during the process," Beesley explains.

"What that tells you is the funds we've been rationalising truly were the smaller, subscale, non-differentiated funds.

"There'll always be ongoing need to curate the product shelf, and the rationalisation process has been really important to make it crystal clear to our clients what it is that we stand for."

‘Completely different' to Woodford

One fund that has featured in negative headlines for Jupiter is its UK Mid Cap fund, managed by Chrysalis' manager Richard Watts, which has found itself as the new poster child for arguments against holding unlisted assets in a daily dealing vehicle.

An Investment Week study found Jupiter UK Mid Cap delivered the worst maximum drawdown in the UK All Companies sector over 2022, recording a worst-case figure of 43.7%, while Fidelity International restricted new investment into the fund for certain customers on 30 December 2022.

The concerns centred mostly on the fund's investment in the unlisted Starling Bank, which grew to such an extent it threatened to breach the 10% liquidity rule.

When asked if the fund represented a reputational risk for the asset manager, Beesley is succinct: "No."

"While we had over multiple periods effectively and carefully managed exposure of [Starling Bank] and [Jupiter UK Mid Cap], clients were concerned that it might be getting too large and what the ramifications would be," he explains.

"We addressed that by selling the asset in its entirety, and to reflect evolving client needs and views, we've undertaken an intention to prohibit from here onwards investment into private assets by our daily priced, unitised vehicles."

Stifel downgrades Jupiter's Chrysalis to 'Sell'

Jupiter changed its investment policies around unlisted assets earlier this year as Beesley told clients in a letter it would no longer make investments in the asset class via any open ended funds.

However, its closed ended options were still able to pick up stocks in this space, which meant when Starling Bank was sold from UK Mid Cap, the stake was picked up by Chrysalis, the investment trust co-managed by Watts, which some noted was a move used by Neil Woodford in the latter days of Woodford Investment Management.

"There is no link here to the issues with Neil Woodford," Beesley affirms. "It's a completely different set of circumstances.

"We're talking about one asset, whereas in the case of Neil Woodford there was obviously a range of assets in that portfolio.

"At no point was that asset breaching any of the regulatory guidelines to which we adhere at all times, and like most asset management businesses, where we have potential conflicts of interest, we work very carefully to make sure they are identified and appropriately addressed."

Misleading pigeonholes

Jupiter Asset Management may well be known in the UK as an equities house with a legacy of star managers, but Beesley notes, on the continent, the firm is better known as a fixed income house.

While the UK remains 70% of Jupiter's business, its non-UK arm is growing faster than the UK, which may eventually see these two branches balance out in the coming years.

Beesley reaffirms his commitment to the wholesale market but adds that requests for proposals from institutional investors have doubled in size from an average of £250m in 2022, to around £500m this year.

"I've got a very clear mandate from the board to take this business forward - my focus with Matt and Kiran and other parts of the management team is on executing on that strategy," he says.

"Any attempt to try and pigeonhole us is likely to be somewhat misleading."