Investors Tread Carefully Following FOMC Minutes, Awaiting Key US Job Reports

Major US stock indexes closed lower overnight, after FOMC minutes revealed Fed might be hesitance to lower interest rates soon. Notably, the likelihood of a March interest rate cut, as inferred from Fed funds futures, dipped below the 70% market following the release of the minutes. Dollar, however, is encountering challenges in gaining further momentum in its near term rebound. This struggle is partly attributed to 10-year Treasury yield’s rejection by 4% level. Investors are now turning their attention to today’s ADP employment data, though significant market moves are more likely to be reserved for tomorrow’s non-farm payroll report.

In the broader currency market, Japanese Yen is currently the weakest performer for the week. BoJ Governor Kazuo Ueda reiterated today the importance of a “virtuous cycle” between wages and prices in his speech. However, the recent devastating earthquake in Japan has led some economists to pull back their expectations of a January rate hike, as BoJ may need additional time to assess the earthquake’s economic impact.

Euro and Australian Dollar are also among the weaker performers. Euro’s immediate focus is on the German CPI data due today and, more significantly, Eurozone CPI flash data expected tomorrow. Meanwhile, Australian Dollar has not found substantial support despite positive data from China’s services sector. Conversely, Pound is showing resilience, partly supported by buying against Euro. Canadian Dollar also maintains a firm position, while Swiss Franc displays mixed performance.

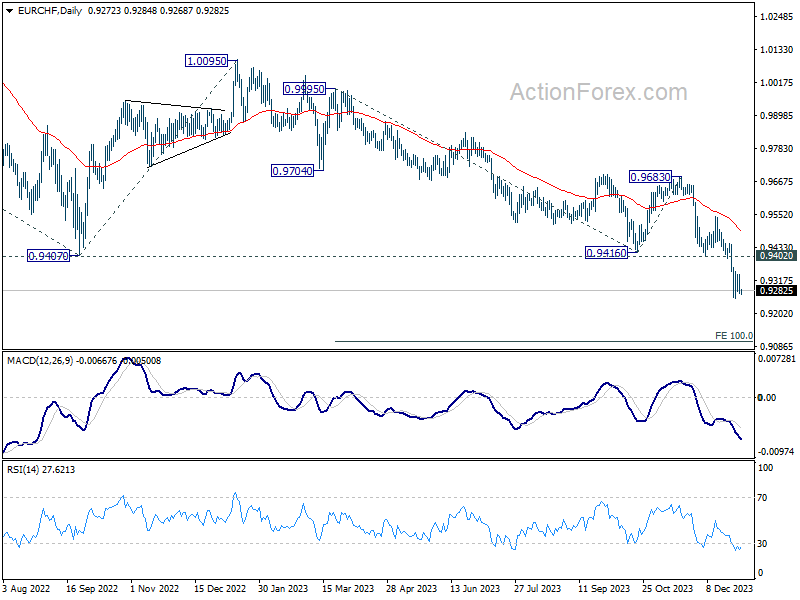

Technically, EUR/CHF would be a focus for the rest of the week with Eurozone CPI flash featured. Price actions from 0.9252 are seen as a consolidation pattern only. While another recovery cannot be ruled out, outlook will stay bearish as long as 0.9402 support turned resistance holds. Break of 0.9252 will resume larger down trend to 100% projection of 0.9995 to 0.9416 from 0.9683 at 0.9104 next.

In Asia, at the time of writing, Nikkei is down -0.57%. Hong Kong HSI is down -0.62%. China Shanghai SSE is down -0.87%. Singapore Strait Times is down -1.18%. Japan 10-year JGB yield is down -0.0060 at 0.620. Overnight, DOW fell -0.76%. S&P 500 fell -0.80%. NASDAQ fell -1.18%. 10-year yield fell -0.039 to 3.907.

FOMC minutes see dual-mandate dilemma ahead

Minutes from FOMC’s December meeting indicate that some participants are concerned about the risks of stalling progress in bringing down inflation to target. Simultaneously, there is apprehension about downside risks to the economy resulting from “overly restrictive monetary policy”. Hence, a few suggested that Fed could “face a trade off between its dual-mandate goals in the period ahead”.

Significantly, the minutes indicate a consensus among participants that, considering the improved inflation outlooks, a lower target range for federal funds rate would likely be appropriate by the end of 2024. However, they also recognized “an unusually elevated degree of uncertainty” in their economic outlooks, leaving room for the possibility that economic developments might necessitate further rate increases or maintaining the current target range longer than currently anticipated.

The emphasis in the discussions was on the need for a “careful, data-dependent approach” to policy decisions. The minutes also highlighted that “it would be appropriate for policy to remain at a restrictive stance for some time,” underlining the commitment to ensure that inflation is sustainably moving towards the Committee’s objective.

Participants also discussed risk-management considerations for future policy decisions. They acknowledged that while upside risks to inflation have decreased, inflation is “still well above the Committee’s longer-run goal.” Moreover, the minutes reflected a concern about the duration for which a restrictive monetary policy would be necessary, pointing to “downside risks to the economy” associated with such a stance. A few participants raised the possibility of a trade-off between the Fed’s dual-mandate goals.

Japan’s PMI manufacturing finalized at 47.9, deeper contraction and higher input inflation

Japan’s PMI Manufacturing was finalized at 47.9 in December, down from November’s 48.3, marking the most significant sector contraction since February 2023. S&P Global reports that this downturn was characterized by notable declines in both production and new orders, alongside rise in input price inflation. Despite these challenges, there was an unexpected increase in business confidence, reaching a five-month high.

Paul Smith from S&P Global Market Intelligence noted, “Market uncertainty led to reduced orders and output, especially from key export clients in China, Europe, and North America.” He also mentioned specific struggles in the electronics sector and a general lack of investment.

However, Smith acknowledged increased cost pressures, with input price inflation at a three-month high due to more expensive raw materials, particularly imports.

Looking ahead, Smith conveyed optimism among Japanese manufacturers, expecting an end to client destocking and predicting that new product launches will boost production in 2024.

China’s Caixin PMI services rises to 52.9, businesses express confidence

China’s Caixin PMI Services marked a significant rise to 52.9 in December from 51.5, achieving its highest level since July. Concurrently, PMI Composite, which combines both manufacturing and services, also saw an improvement, climbing from 51.6 to 52.6.

Wang Zhe, Senior Economist at Caixin Insight Group, noted that businesses are “expressing confidence” in an improved economic outlook for the coming year. This optimism is reflected in the business expectations gauge, which, despite being “about 3 points below” the 2023 average for the first 11 months, still aligns with the “historical mean” from 2012 to 2022.

Looking ahead

Germany CPI flash, Eurozone PMI services final and UK PMI services final will be released in European session. Later in the day, main focus will be on US ADP employment and jobless claims.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6698; (P) 0.6735; (R1) 0.6767; More…

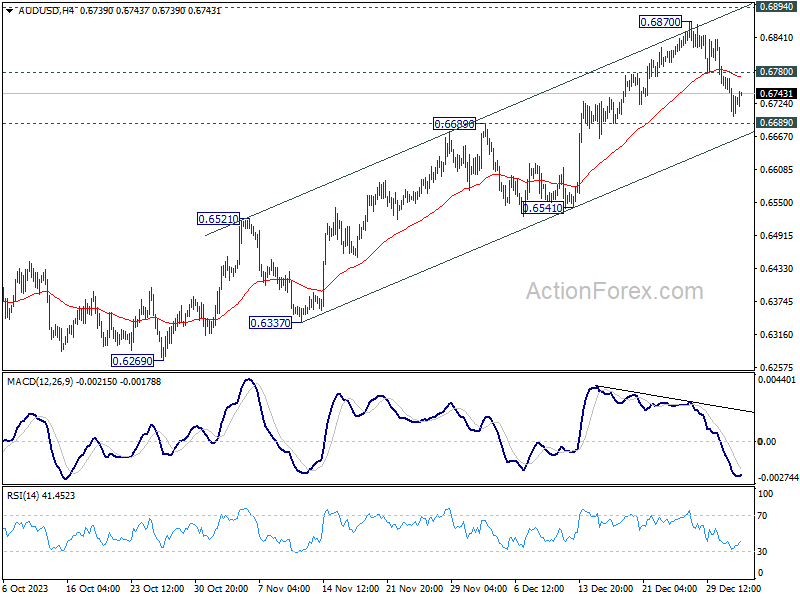

Intraday bias in AUD/USD remains mildly on the downside at this point. Pull back from 0.6870 short term top is in progress for 0.6689 resistance turned support, and possibly below. But strong support would be seen from channel support (now at 0.6663) to bring rebound. On the upside, above 0.6780 minor resistance will turn bias back to the upside for retesting 0.6870 instead.

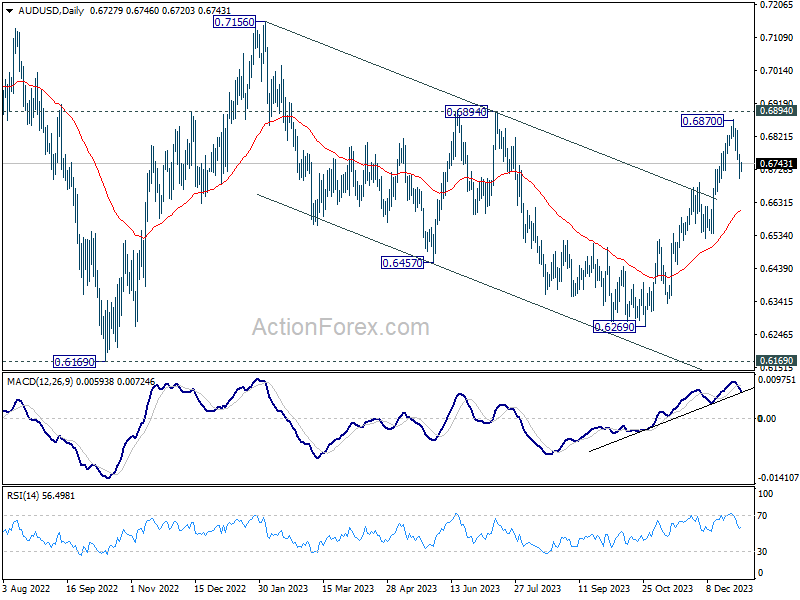

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. Price actions from 0.6169 (2022 low) could be just a medium term corrective pattern. Rise from 0.6269 is seen as the third leg of the pattern. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Dec F | 47.9 | 47.7 | 47.7 | |

| 01:45 | CNY | Caixin Services PMI Dec | 52.9 | 51.6 | 51.5 | |

| 08:45 | EUR | Italy Services PMI Dec | 49.8 | 49.5 | ||

| 08:50 | EUR | France Services PMI Dec F | 44.3 | 44.3 | ||

| 08:55 | EUR | Germany Services PMI Dec F | 48.4 | 48.4 | ||

| 09:00 | EUR | Eurozone Services PMI Dec F | 48.1 | 48.1 | ||

| 09:30 | GBP | Services PMI Dec F | 52.7 | 52.7 | ||

| 09:30 | GBP | Mortgage Approvals Nov | 48K | 47K | ||

| 09:30 | GBP | M4 Money Supply M/M Nov | 0.20% | 0.30% | ||

| 12:30 | USD | Challenger Job Cuts Y/Y Dec | -40.80% | |||

| 13:00 | EUR | Germany CPI M/M Dec P | 0.20% | -0.40% | ||

| 13:00 | EUR | Germany CPI Y/Y Dec P | 3.80% | 3.20% | ||

| 13:15 | USD | ADP Employment Change Dec | 130K | 103K | ||

| 13:30 | USD | Initial Jobless Claims (Dec 29) | 210K | 218K | ||

| 14:45 | USD | Services PMI Dec F | 51.3 | 51.3 | ||

| 15:30 | USD | Natural Gas Storage | -33B | -87B | ||

| 16:00 | USD | Crude Oil Inventories | -3.2M | -7.1M |

When The Wave Turns

Why Retirement Investing Is Moving Towards Resilience Jeremy Grantham’s latest market warnings have revived an old tru... Read more

Gyrostat Capital Management: July Retirement Portfolio Resilience Assessment

The Market Is Currently Presenting an Opportunity to Strengthen Retirement Portfolio Resilienc... Read more

The Invisible Risk That Decides Your Retirement

Why how investors behave matters more than what markets do and what disciplined port... Read more

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more