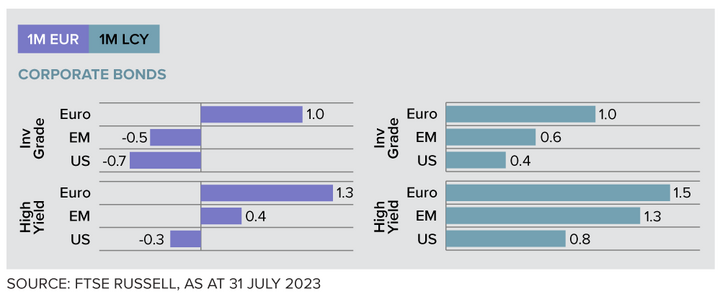

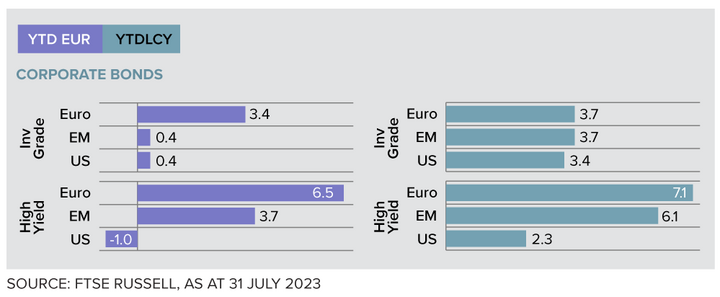

As Table 1 shows, the FTSE Euro High Yield Bond index was up 1.3% and 6.5%, respectively, in July and year-to-date, compared to 1% and 3.4% for the IG equivalents, while credits in other regions were modestly higher or lower. So why did Euro high yield credit outperform, and can this outperformance continue?

Table 1: Euro HY have led the corporate bond rally in July and YTD

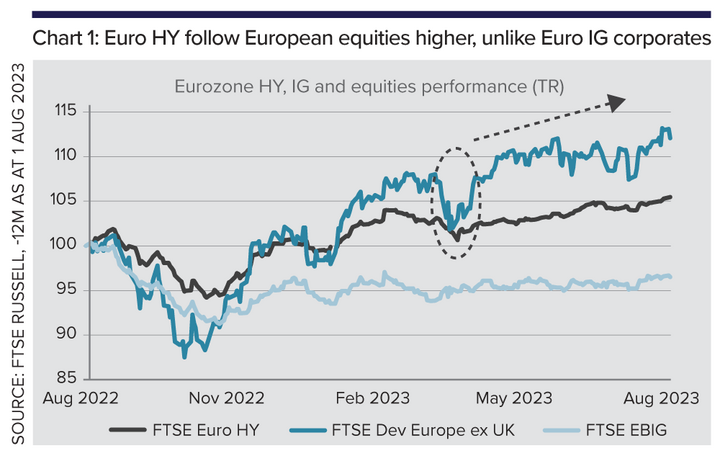

Chart 1 shows Euro high yield bonds have followed Eurozone equities higher over the last 12 months, with much of the increase seen since Q2 2023, while the performance of investment grade corporate bonds was more subdued.

Credit rallied for a number of reasons: renewed optimism over early central bank pivots, more confidence in a soft landing for growth and inflation, low default rates and increased risk appetite.

Also, both the US Fed and Swiss SNB intervened to calm markets and reduce systemic risks, after the collapse of Silicon Valley Bank and Credit Suisse in Europe, upgrading depositor protection and providing emergency liquidity.

The Swiss authorities' decision to "bail-in" Contingent Convertible bond holders, or Cocos, added pressure on high yield debt markets, since equity holders in Credit Suisse were treated more favourably than Coco bondholders in the resolution. But contagion has proved limited, helped by higher Eurozone bank Tier 1 capital ratios.

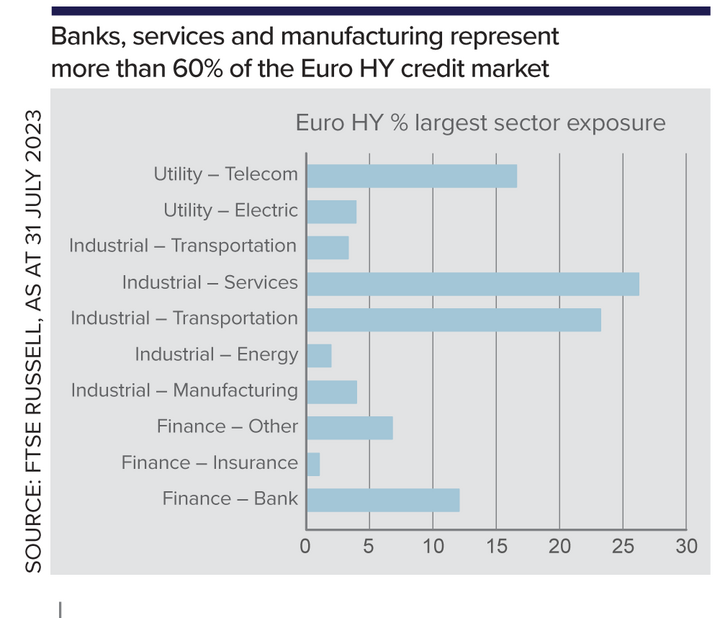

The FTSE Euro high yield bond market has a sizeable exposure to banks (12%) and, with other financials, they account for a weight close to 20% as Table 2 shows.

Moreover, the next two largest industries, manufacturing and services, represent a weight of over 20% and 25%, respectively. While manufacturing has slowed within the Eurozone, services have remained robust, underpinned by post-Covid recoveries in consumer demand in sectors like tourism and travel.

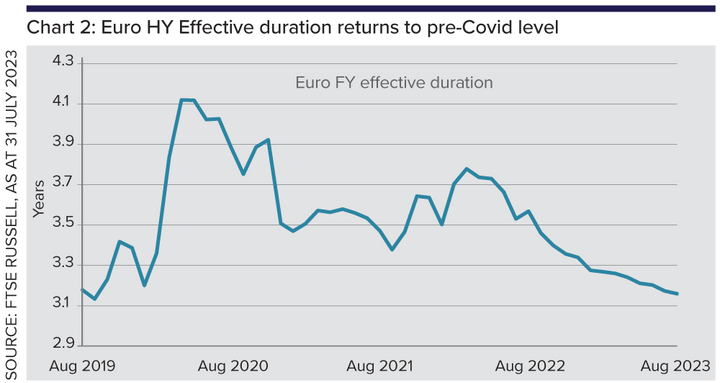

Shorter duration has also offered investor protection in high yield indices

High yield credit issuers are rarely able to borrow in longer maturities, so HY indices tend to have shorter duration than IG indices.

HY index duration proved volatile in the early days of Covid, as HY credits first fell sharply in price on risk-aversion and default fears, before rallying after the ECB began QE programmes, and eased financial conditions through its bank LTROs.

Overall, as Chart 2 illustrates, the effective duration for the FTSE Euro High Yield Bond index fell from about four years in 2020 to close to its pre-Covid level of about three years.

But HY issuance in Euros has been generally very low since Covid, as companies have often substituted bank finance at more favourable terms. The maturity profile and duration of Eurozone HY debt has also shortened as a result.

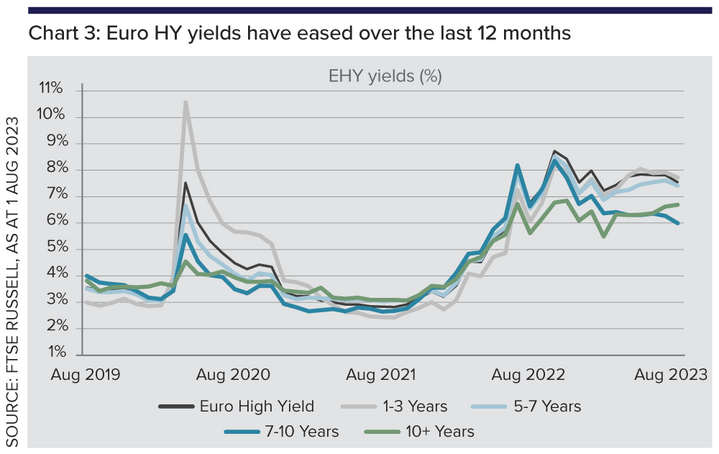

A further breakdown of the Euro HY performance across the curve shows yields declining in most maturities over the last year, with the 5-7-year section dropping the most, from 8% to about 6%.

Even so, yield levels for Euro HY are still high, and higher than during the Covid spike. Only the 1-3-year area, which was close to 11%, has fallen to about 8%.

The longest part of the curve, the 10-year plus, while stable over the last 12 months, has seen the least yield compression since 2020 (Chart 3).

Despite the higher yields, credit defaults, while rising, have remained relatively modest this year.

According to S&P Global Ratings, the number of defaults in Europe fell from seven to six since January. Meanwhile, European default rates are expected to rise "to 4.25% in the US and 3.6% in Europe by spring 2024", notably in the more speculative end of the market.

However, comparing and projecting default rates with previous credit cycles may not be a reliable metric, given that default rates are also driven by covenants within bond prospectuses, and investor protection covenants have tended to weaken since the GFC.

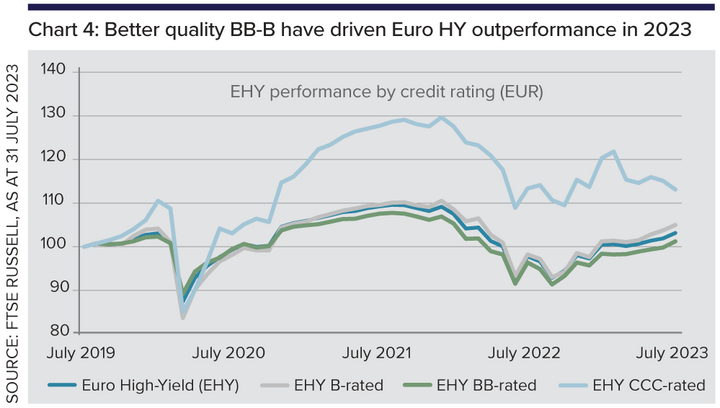

Credit quality of HY indices has improved as share of BB-rated securities increased

Looking instead at the performance of different rating buckets within high yield, lower rated CCC securities have underperformed, as Chart 4 shows, and much of the positive performance came from the higher quality BB-B securities, which make up 76% of the FTSE Euro High Yield Bond index exposure.

The higher share of BB-rated securities in HY indices reflects the impact of rating downgrades, in some cases "fallen angels", which have migrated from IG to HY.

But this has improved the overall credit quality of HY indices.

Sandrine Soubeyran is director of global investment research at FTSE Russell