Falling Yields Drive Euro And Sterling Down

Euro and Sterling are falling broadly in European session today, a trend largely driven by notable decrease in benchmark yields in Germany and the UK. German 10-year bund yield has reached its lowest point since June. Simultaneously, UK 10-year gilt yield has dipped below 4% mark for the first time since May

These movements in bond markets reflect increasing expectations among investors for upcoming rate cuts by ECB and BoE. Current market pricings suggest the likelihood of four rate cuts from ECB and three from the BoE in 2024. This aggressive pricing-in of rate cuts underscores growing concerns about the economic outlook in Europe and while disinflation is making significant progress.

In the broader currency markets, commodity currencies are displaying robustness, particularly led by New Zealand Dollar, with Australian Dollar also showing strength but not to the same extent. Canadian Dollar’s performance is keenly watched as traders and investors await the upcoming rate decision from BoC. There is a focus on whether the BoC will introduce dovish elements in its policy statement, which could significantly influence the Loonie’s next move.

Meanwhile, Swiss Franc is showing mixed performance, gaining strength against its European peers while maintaining a balanced position overall. Dollar turns softer after weaker than expected ADP Job data, while Yen is digesting this week’s gains.

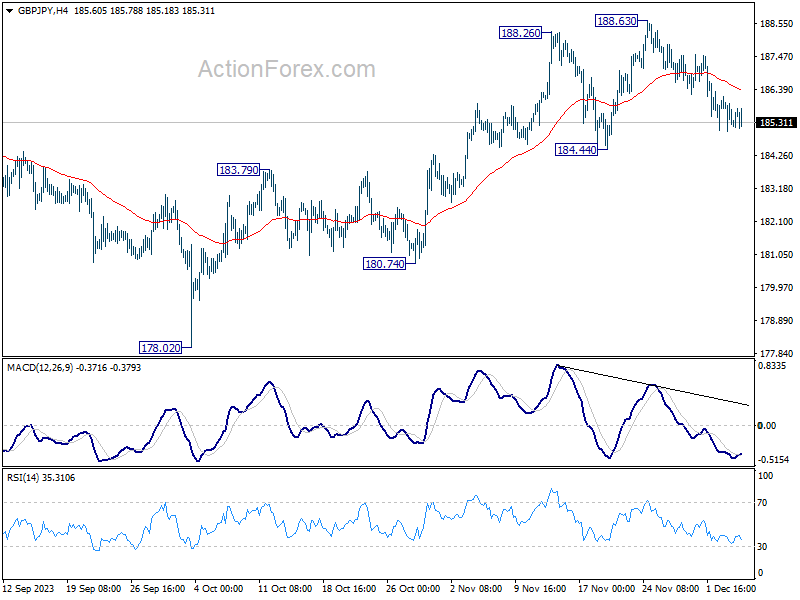

Technically, GBP/JPY is so far still resilient, holding above 184.44 support despite extending the pull back from 188.63. However, firm break of 184.44 will align the outlook with EUR/JPY. That is this decline is actually a larger scale correction. That would open up deeper fall to 180.74 support, or even further to 178.02 key structural support level.

In Europe, at the time of writing, FTSE is up 0.51%. DAX is up 0.58%. CAC is up 0.60%. German 10-year yield is down -0.013 at 2.237. UK 10-year yield is down -0.039 at 3.998. Earlier in Asia, Nikkei rose 2.04%. Hong Kong HSI rose 0.83%. China Shanghai SSE fell -0.11%. Singapore Strait Times rose 0.33%. Japan 10-year JGB yield fell -0.0246 to 0.648.

US ADP jobs grows 103k, pay rise slows further

US ADP private sector employment grew 103k in November, below expectation of 120k. By sector, goods-producing jobs fell -14k while service-providing jobs rose 117k. By establishment size, small companies added 6k jobs, medium companies added 68k, large companies added 33k.

Job-stays saw a 5.6% yoy pay increase, down from 5.7% yoy, and the slowest since September 2021. Job-changes saw a 8.3% yoy pay rise, down from 8.4% yoy, slowest since June 2021.

“Restaurants and hotels were the biggest job creators during the post-pandemic recovery,” said Nela Richardson, chief economist, ADP. “But that boost is behind us, and the return to trend in leisure and hospitality suggests the economy as a whole will see more moderate hiring and wage growth in 2024.”

Eurozone retail sales rises 0.1% mom in Oct, EU up 0.3% mom

Eurozone retail sales volume rose 0.1% mom in October, below expectation of 0.2% mom. Volume of retail trade increased by 0.8% mom for non-food products, while it decreased by -0.8% mom for automotive fuels and by -1.1% mom for food, drinks and tobacco.

EU retail sales rose 0.3% mom. Among Member States for which data are available, the highest monthly increases in the total retail trade volume were registered in Croatia (+3.1%), the Netherlands (+2.4%) and Slovakia (+1.9%). The largest decreases were observed in France (-1.0%), Belgium and Austria (both -0.8%), Spain and Portugal (both -0.4%).

UK PMI construction fell to 45.5, ongoing sectoral downturn

UK PMI Construction ticked down from 45.6 to 45.5 in November, remaining below the neutral 50 mark and underperforming against the expected 47.1. This level indicates continued contraction in the construction sector for the third month, marking it as the second-lowest reading since May 2020.

Tim Moore of S&P Global Market Intelligence highlighted the sector’s issues, stating, “A slump in house building has cast a long shadow over the UK construction sector.” He pointed out that the downturn in residential construction has persisted for the past 12 months, with recent reductions among the steepest since 2009.

Elevated mortgage costs and adverse market conditions were cited as key reasons for the decline in housing projects. Additionally, rising interest rates and economic uncertainty are adversely affecting commercial construction, while civil engineering activity saw its sharpest drop since July 2022.

Moore also noted a significant decrease in overall input prices for the second consecutive month, marking the fastest rate of decline since July 2009. Despite this decrease in costs, the sector continues to face substantial challenges.

BoE’s Bailey: Rates to stay high for an extended period

BoE Governor Andrew Bailey, in a press conference today, stated that “rates are likely to need to remain at these levels for an extended period to bring inflation back to target on a sustained basis,” referring to the current bank rate at 5.25%.

He also noted that the full impact of the higher interest rates is yet to be fully realized, and highlighted the central bank’s vigilance towards potential financial stability risks that might emerge as a result.

Separately, BoE’s half-yearly Financial Stability Report noted, “The overall risk environment remains challenging, reflecting subdued economic activity, further risks to the outlook for global growth and inflation, and increased geopolitical tensions.”

The report also drew attention to the strains on household finances due to rising living costs and higher interest rates. It pointed out that some effects of these higher rates, particularly in terms of mortgage repayments, have yet to fully manifest.

Australia’s Q3 GDP growth slows to 0.2% qoq, per capita output declines

Australia’s GDP for Q3 showed a modest increase of 0.2% qoq, falling short of the expected 0.5% qoq growth. On a year-on-year basis, GDP grew by 2.1%. However, a contrasting picture emerges when considering GDP on a per capita basis, which revealed a decline of -0.5% qoq and a -0.3% yoy.

Katherine Keenan, ABS head of national accounts, said: “This was the eighth straight rise in quarterly GDP, but growth has slowed over 2023.” She pointed out that government spending and capital investment were the primary contributors to GDP growth in this quarter.

Specifically, government final consumption expenditure rose by 1.1%. Additionally, gross fixed capital formation also saw a 1.1% rise.

An interesting aspect of the September quarter’s GDP was the contribution of 0.4% points from changes in inventories. Notably, mining inventories increased by AUD 2.4B, a reflection of the larger fall in exports compared to production volumes.

On the other hand, trade in services had a negative impact on growth. Imports of services surged by 8.4%, significantly outpacing the 1.9% growth in services exports.

BoJ’s Himino stresses patience in monetary easing to prevent return to “frozen state”

BoJ Deputy Governor Ryozo Himino, in a speech today, affirmed the central bank’s commitment to continued monetary easing. He noted, “the Bank will patiently continue with monetary easing until sustainable and stable achievement of the price stability target, accompanied by wage increases, comes in sight.”

He acknowledged the positive changes in firms’ wage- and price-setting behavior, noting “solid progress” and “signs in the right direction.” However, he warned of the risks of reverting to a deflationary state if a virtuous cycle between wages and prices is not established.

Explaining further, Himino commented on the longstanding norm in Japan where neither wages nor prices could rise significantly. “Japan had worked for many years to break free from this,” he added, “and simply returning to such a frozen state after the current high inflation comes down would not be a desirable outcome either.”

Himino highlighted the longstanding norm in Japan where “neither wages nor prices could rise”. He stressed that Japan’s efforts to break free from this stagnation, adding, “simply returning to such a frozen state after the current high inflation comes down would not be a desirable outcome”.

He also outlined the multiple challenges facing Japanese monetary policy, including addressing current inflation, supporting moderate economic recovery, encouraging wage increases, and preventing a return to deflation. “The Bank is struggling to find a solution and this is by no means an easy task,” he admitted.

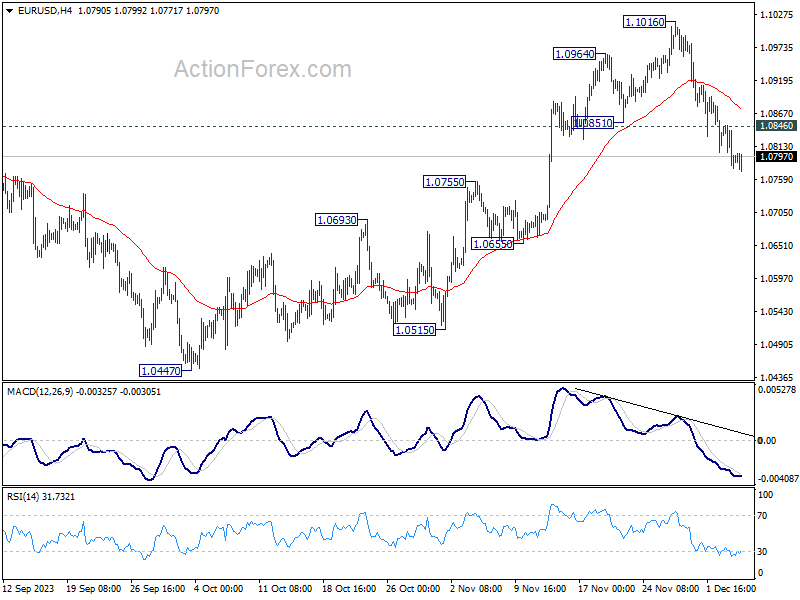

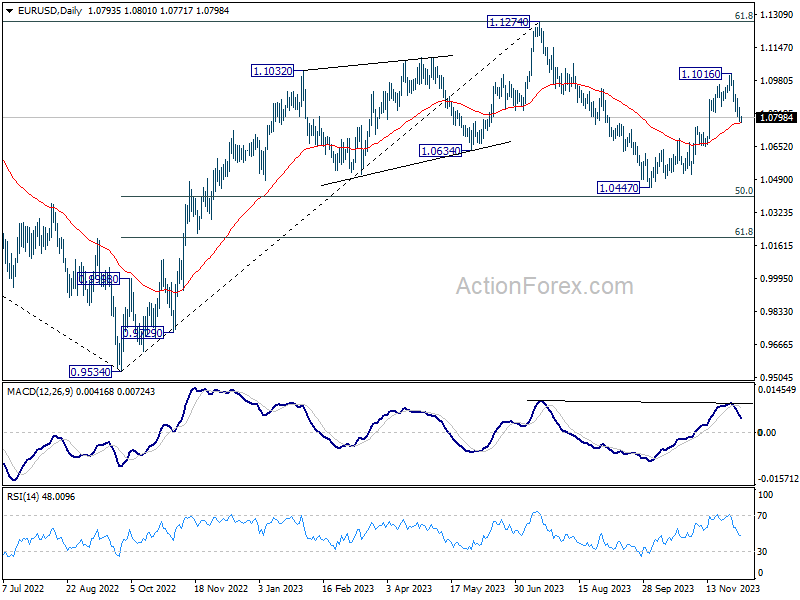

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0768; (P) 1.0808; (R1) 1.0838; More…

EUR/USD’s fall from 1.1016 is still in progress and intraday bias stays on the downside. Sustained break of 55 D EMA (now at 1.0770) will pave the way to retest 1.0447 support. On the upside, above 1.0846 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1016 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q3 | 0.20% | 0.40% | 0.40% | |

| 07:00 | EUR | Germany Factory Orders M/M Oct | -3.70% | 0.50% | 0.20% | 0.70% |

| 09:30 | GBP | Construction PMI Nov | 45.5 | 47.1 | 45.6 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | 0.10% | 0.20% | -0.30% | -0.10% |

| 13:15 | USD | ADP Employment Change Nov | 103K | 120K | 113K | 106K |

| 13:30 | CAD | Labor Productivity Q/Q Q3 | -0.80% | 0.20% | -0.60% | |

| 13:30 | CAD | Trade Balance (CAD) Oct | 3.0B | 1.8B | 2.0B | |

| 13:30 | USD | Trade Balance (USD) Oct | -64.3B | -63.0B | -61.5B | -61.2B |

| 13:30 | USD | Nonfarm Productivity Q3 | 5.20% | 4.70% | 4.70% | |

| 13:30 | USD | Unit Labor Costs Q3 | -1.20% | -0.80% | -0.80% | |

| 15:00 | CAD | BoC Rate Decision | 5.00% | 5.00% | ||

| 15:00 | CAD | Ivey PMI Nov | 54.2 | 53.4 | ||

| 15:30 | USD | Crude Oil Inventories | -1.3M | 1.6M |

When The Wave Turns

Why Retirement Investing Is Moving Towards Resilience Jeremy Grantham’s latest market warnings have revived an old tru... Read more

Gyrostat Capital Management: July Retirement Portfolio Resilience Assessment

The Market Is Currently Presenting an Opportunity to Strengthen Retirement Portfolio Resilienc... Read more

The Invisible Risk That Decides Your Retirement

Why how investors behave matters more than what markets do and what disciplined port... Read more

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more