European PMIs Shrugged Off, Focus Turns To Aussie CPI

The forex markets remained largely directionless today, with consolidative trading dominating across major pairs. Price action was muted, and the release of PMI data failed to provide much impetus, with investors largely shrugging off the surveys.

Eurozone PMIs offered a mixed picture. Germany showed a promising improvement, but sluggish readings in France offset the optimism. Overall, the bloc remains on a growth path, though easing price pressures could give the ECB room to weigh another rate cut.

That said, most ECB officials have sounded comfortable with the deposit rate at 2.00%, and the bar for an additional move appears high. With inflation steadily at target and growth still intact, policymakers may prefer to stay patient unless a sharp downturn forces their hand.

In the UK, PMI data painted a more troubling picture. Weakening growth, rising unemployment, and softer inflation pressures raise the possibility that the BoE could tilt more dovish in coming months. However, the MPC is known for its divisions, and members may interpret the same data differently, keeping the November meeting very much live.

Looking ahead to Asia, Australia’s monthly CPI is due in the next session. The index is expected to hold steady at 2.8% in August, and only a major surprise would meaningfully alter expectations. The RBA is widely expected to keep policy unchanged next week, awaiting quarterly inflation figures before reconsidering whether to cut in November. For the Aussie, sensitivity remains higher to Chinese market sentiment rather than domestic data for now.

Performance rankings show Swiss Franc leading gains this week, followed by Euro and Sterling. At the bottom, Loonie has been the weakest, trailed by Dollar and Kiwi. Aussie and Yen are sitting mid-pack. But with nearly all major pairs and crosses still contained within last week’s ranges, the FX market is marking time.

OECD upgrades 2025 growth forecast, tariff impact less severe

OECD’s latest Interim Economic Outlook projected global GDP growth of 3.2% in 2025, an upward revision from 2.9% in June, before easing to 2.9% in 2026. The agency said tariffs and policy uncertainty remain headwinds for trade and investment, but the upward revision shows the drag is proving smaller than previously feared.

In the U.S., GDP growth is projected to slow sharply, from 2.8% in 2024 to 1.8% in 2025 and 1.5% in 2026. The drag reflects the combined effect of tariff hikes, weaker net immigration, and a reduced federal government workforce.

China is also expected to lose momentum, easing from 4.9% in 2025 to 4.4% in 2026 as earlier stimulus fades and tariffs start to bite more fully.

In the Eurozone, growth is forecast at 1.2% in 2025 and 1.0% in 2026. The region continues to face increased trade frictions and geopolitical uncertainty, though these will be partially offset by stronger public investment programs and looser credit conditions.

On prices, the OECD expects headline G20 inflation to fall from 3.4% in 2025 to 2.9% in 2026, reflecting weaker growth and softening labor markets. Core inflation in advanced economies is forecast to decline only marginally, from 2.6% to 2.5%, suggesting underlying price stickiness remains.

The report warned that risks to disinflation persist. Goods prices have edged higher again in some economies, and services inflation remains stubborn.

BoE’s Pill more comfortable on inflation, opposed slower QT pace

BoE Chief Economist Huw Pill signaled a softer tone on inflation risks, saying in a speech he is “more comfortable now” than six to twelve months ago. While he had previously stressed the balance of risks lay more on the inflationary side, he acknowledged that as time has passed and markets have repriced, the risks are shifting.

Pill has been among the more hawkish members of the MPC, opposing last week’s decision to slow the pace of quantitative tightening. The Bank will now reduce its gilt holdings by GBP 70bn over the coming year, down from GBP100bn last year, a move Pill resisted.

He explained his preference for “continuity and consistency” in QT, arguing that the framework works best when Bank Rate is the active tool for policy adjustments. With rates far from the lower bound, the MPC has flexibility to use Bank Rate to achieve its inflation target while QT runs in the background.

UK PMI composite falls to 51, raises pressure on BoE to turn dovish

UK business activity weakened sharply in September, with the flash composite PMI dropping from 53.5 to 51.0, a 4-month low. Manufacturing fell further into contraction from 47.0 to 46.2. Services slipped from 54.2 to 51.9, pointing to a broad loss of momentum across sectors.

S&P Global’s Chris Williamson described the report as a “litany of worrying news,” citing slumping overseas trade, worsening confidence, and steep job losses. The survey signalled around 50,000 job cuts over the past three months, underscoring that the economy is “almost stalling.”

The only bright spot was softer price pressures, with firms reporting one of the smallest increases in goods and services prices since the pandemic. For the BoE, the combination of weakening growth, easing inflation, and rising unemployment may shift the debate back toward a “more dovish stance” in the months ahead.

Eurozone PMI composite at 16-month high of 51.2, Germany lifts while France drags

Eurozone flash PMIs for September showed a mixed picture, with manufacturing slipping back into contraction while services drove growth. The manufacturing index fell from 50.7 to 49.5, but services rose from 50.5 to 51.4, a 9-month high, lifting the Composite PMI from 51.0to 51.2 — its strongest in 16 months.

Hamburg Commercial Bank’s Cyrus de la Rubia said the bloc is “still on a growth path,” though far from gaining “any real momentum”. Germany’s recovery stood out, with manufacturing falling from 59.8 to 48.5 but services jumping to 52.5, pushing its Composite PMI from 50.5 to 52.4 (a 16-month high). France lagged, with both manufacturing and services sliding back below 50, leaving its composite at 48.4, down from 49.8 and a 5-month low.

De la Rubia cautioned that French political uncertainty had disrupted production plans, while order books in both Germany and France showed significant declines. Hiring has now “come to a halt” across the bloc, with sluggish job creation in services and sharper losses in manufacturing. Confidence in rising output has dipped.

On the inflation side, cost pressures in services have “eased slightly” but remain unusually high, while selling prices “cooled more noticeably”. That combination could give the ECB reason to consider whether a rate cut before year-end is back on the table.

Australia PMI composite hits three-month low at 52.1, confidence slumps

Australia’s private sector momentum slowed sharply in September, with PMI Composite falling from 55.5 to 52.1, its lowest in three months. Manufacturing eased from 53.0 to 51.6, while services slipped more heavily from 55.8 to 52.0, signaling a broad moderation in activity.

S&P Global’s Jingyi Pan noted that new business growth weakened after two strong months, with manufacturing orders slipping back into contraction as U.S. tariffs began to weigh. Export orders also faltered, while overall business confidence dropped to its lowest in a year, hinting at a softer growth outlook into Q4.

The survey did show resilience in employment, with job creation little changed from August. However, selling price inflation remained “at a level that was above the long-run average”, and a steep rise in manufacturing cost inflation underscored margin pressures for goods producers.

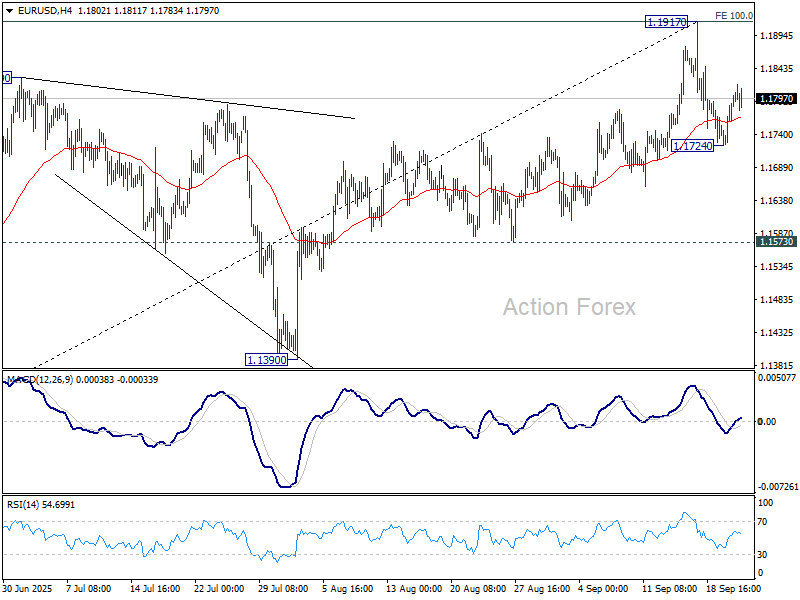

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1751; (P) 1.1777; (R1) 1.1829; More…

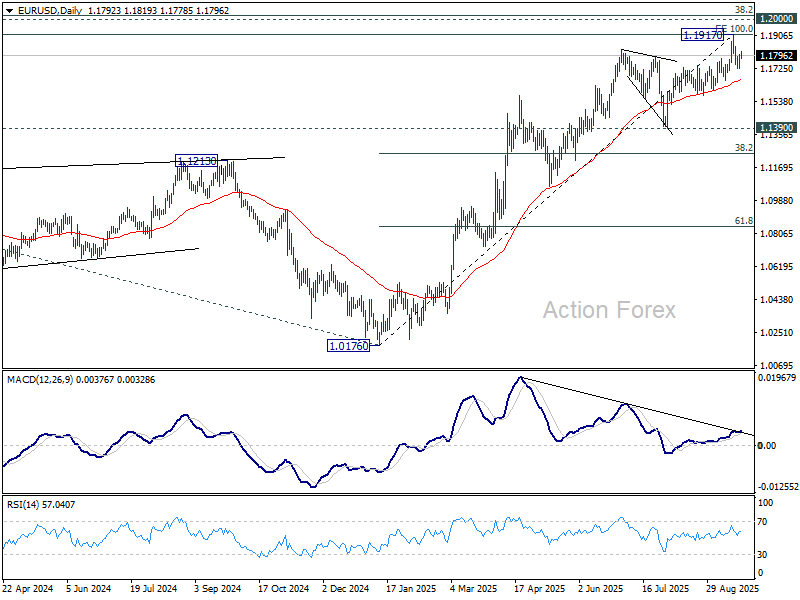

Intraday bias in EUR/USD remains neutral at this point. On the downside, break of 1.1724 will resume the fall from 1.1917 to 55 D EMA (now at 1.1663). Considering bearish divergence condition in D EMA, sustained break of 55 D EMA will argue that 1.1917 is already a medium term top. Deeper fall should then be seen to 1.1390 support next. However, sustained break of 1.1917 will resume larger up trend to 1.2 psychological level.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1214).

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more