Euro Fights “Two-Front War” Against Sterling And Swiss Franc

At first glance, Euro looks healthy this week. Dollar is falling, oil prices are collapsing, and risk appetite is roaring back as markets price the possibility of a US-Iran breakthrough and reopening of the Strait of Hormuz. But underneath the broad Dollar selloff, Euro is quietly losing two very important battles — one against Sterling, and another against Swiss Franc.

The fight against Sterling is fundamentally about growth credibility. Europe’s slowdown is looking uglier than Britain’s. Eurozone PMI Composite crashed to 47.5 in May, the weakest level in 31 months, with Services collapsing to 46.4 and Manufacturing momentum fading rapidly. The UK was weak too, with Composite slipping to 48.5, but the details matter enormously. British Manufacturing held at 53.7, the strongest reading in four years, while factory output improved to 52.4. In other words, Britain still looks like an economy slowing into a soft landing. The Eurozone increasingly looks like one drifting toward stagnation with inflation problems still unresolved.

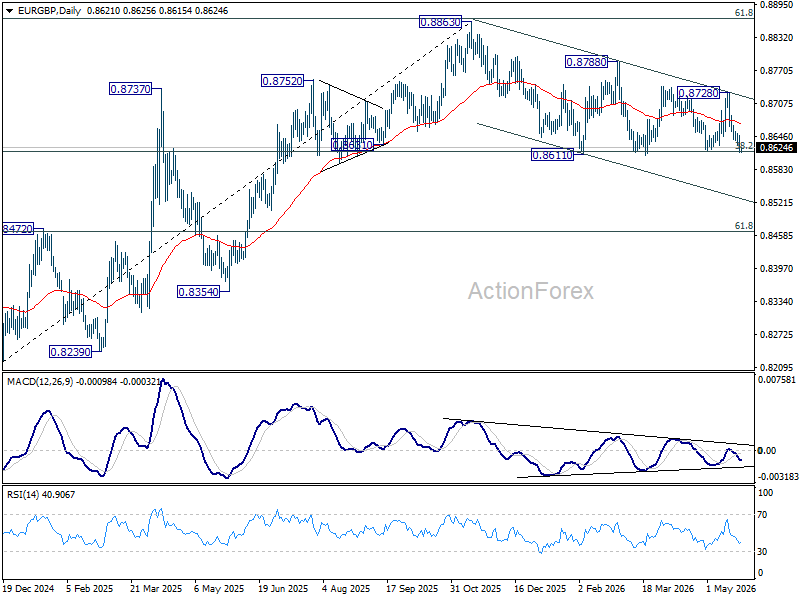

Markets are beginning to reflect that divergence more aggressively in EUR/GBP. The cross is now back pressing the critical 0.8618 Fibonacci support zone, 38.2% retracement of 0.8821 (2024 low) to 0.8863 (2025 high).

A decisive break there would also push the cross firmly below 55 W EMA {now at 0.8649). That would strengthen the case that the entire rise from 0.8821 already topped at 0.8863 after rejection near the major 61.8% retracement of 0.9267 (2022 high) to 0.8821 at 0.8867. In that scenario, deeper losses toward 61.8% retracement of 0.8821 to 0.8863 at 0.8466 should follow.

The battle against Swiss Franc is completely different. Here, the problem is not growth — it is yields and oil. As markets increasingly price a de-escalation in the Middle East, oil prices are falling sharply and global bond yields are retreating. Ironically, the same “peace dividend” helping global equities is also strengthening CHF because lower yields reduce the carry advantage that had supported EUR/CHF.

Technically, EUR/CHF’s rejection at 55 D EMA (now at 0.9164) reinforces the near term bearish outlook. The rebound from 0.8979 should be complete at 0.9264, while the broader downtrend remains intact below the falling 55 W EMA and medium-term trendline resistance.

Retest of 0.8979 is likely next, and a firm break there would resume the broader decline from 0.9928, extending the long-term downtrend that began from the 2018 high at 1.2004.

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more

Gyrostat May Market Outlook: When The Cost Of Protection Falls - Signals For Portfolio Positioning

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. It... Read more

The Risk Most Portfolios Do Not Explicitly Manage

Most portfolios are constructed on a simple and widely accepted assumption: that equity risk will be r... Read more

Gyrostat April Outlook: The Changing Cost Of Protection

Signals For Portfolio Construction This monthly Gyrostat Risk-Managed Market Outlook does not attemp... Read more

What Advisers Misunderstand About Protection

Protection is rarely rejected outright. More often, it is misunderstood. Most advisers recognise th... Read more

Gyrostat Market Outlook: Looking Beyond The 30-day Volatility Headlines

This outlook examines how financial markets are pricing risk rather than attempting to forecast market... Read more