EUR/CHF Bounces As Lower Eurozone Inflation Expectations Fail To Derail ECBs September Hike

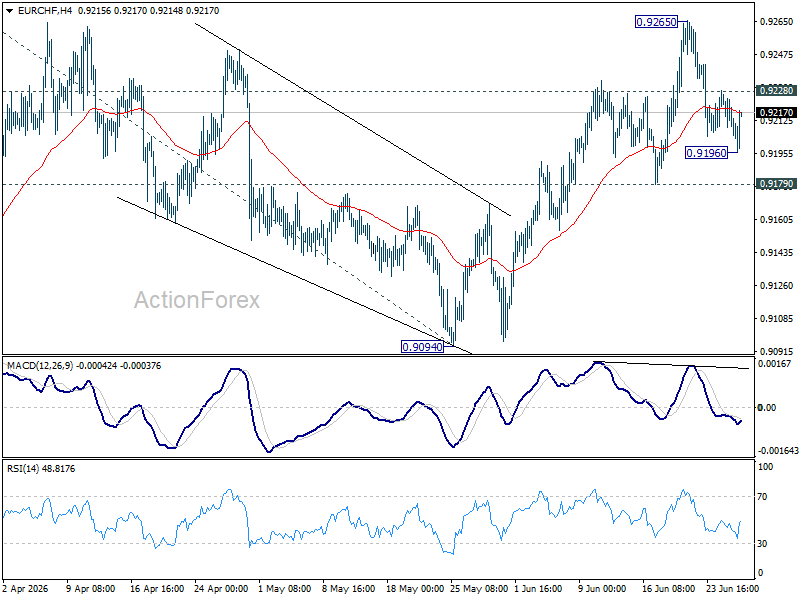

EUR/CHF recovered after briefly dipping to 0.9196 as the latest ECB Consumer Expectations Survey offered modest encouragement on inflation but ultimately reinforced expectations that the central bank’s tightening cycle is not over. While households became less concerned about inflation over the coming year, the improvement was not sufficient to materially alter the policy outlook. Markets continue to view a July pause as the most likely outcome, but a follow-up rate hike in September remains firmly on track.

The most encouraging development in the survey was the sharp decline in one-year inflation expectations. Consumers now expect inflation to average 3.5% over the next 12 months, down from 4.0% previously. That will undoubtedly be welcomed by ECB policymakers, particularly after the inflation shock triggered by the Middle East conflict. However, the improvement looks far less impressive when viewed in a broader context. Before tensions in the region drove energy prices sharply higher, one-year inflation expectations had been as low as 2.5% in February. At 3.5%, households still expect inflation to run a full percentage point above that pre-conflict level, suggesting the recent energy shock has not fully disappeared from consumers’ thinking.

The bigger concern for the ECB may lie further out the curve. Three-year inflation expectations were unchanged at 2.9%, remaining well above February’s 2.5% reading. While five-year expectations also held steady at 2.4%, the lack of improvement in the medium-term outlook is likely to attract greater attention from hawkish policymakers. Persistent medium-term inflation expectations risk feeding into wage negotiations and corporate pricing decisions, making it more difficult for inflation to return sustainably to the ECB’s 2% target.

That is why the survey is unlikely to change the near-term policy path. Following June’s widely anticipated rate hike to 2.25%, the ECB is expected to leave rates unchanged at its July 23 meeting to assess incoming data and evaluate how quickly lower energy prices feed through to inflation. There is little need for back-to-back tightening when policy is already moving into restrictive territory.

September, however, remains a different story. The ECB’s latest staff projections still see headline inflation averaging 3.0% in 2026, reflecting the lingering effects of higher energy prices and the Middle East conflict. As long as medium-term inflation expectations remain elevated and inflation forecasts stay well above target, another 25-basis-point increase to 2.50% continues to appear the most likely outcome. The bigger question for markets is not whether September delivers another hike, but whether inflation proves persistent enough to force one additional move to 2.75% before year-end.

Technically, EUR/CHF is attempting to regain upside momentum after finding support at 0.9179. Immediate focus is now on minor resistance at 0.9228. A firm break there would suggest the pullback from 0.9265 has already completed and shift attention back to that recent high.

More importantly, as long as 0.9179 holds, the broader bullish case remains intact. Decisive break above 0.9265 would confirm resumption of the rally from the March low at 0.8979 and open the way toward 100% projection of 0.8979 to 0.9264 from 0.9094 at 0.9379.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more