Dollar Strength Persists As Markets Await Fed Speakers

Dollar stayed broadly firm in Asian session today, after rallying on robust manufacturing data and significant rebound in treasury yields overnight. The spotlight now shifts to upcoming comments from Fed officials, including Governor Michelle Bowman and New York Fed President John Williams, as markets seek clues about the central bank’s monetary easing path.

The burning question for investors and analysts alike revolves around Fed’s readiness to initiate interest rate cuts in June, and whether three cuts will be delivered this year. The forthcoming remarks from Fed officials are expected to offer a glimpse into the current hawk-dove dynamic within the central bank, with additional guidance likely to emerge from the ISM services data and Non-Farm Payroll reports slated for later in the week.

In the broader forex market, Sterling is currently the weakest performer so far this week, trailed by Kiwi and Euro. On the other hand, Canadian Dollar and Japanese Yen have shown relative resilience, while Australian Dollar and Swiss Franc are mixed in the middle.

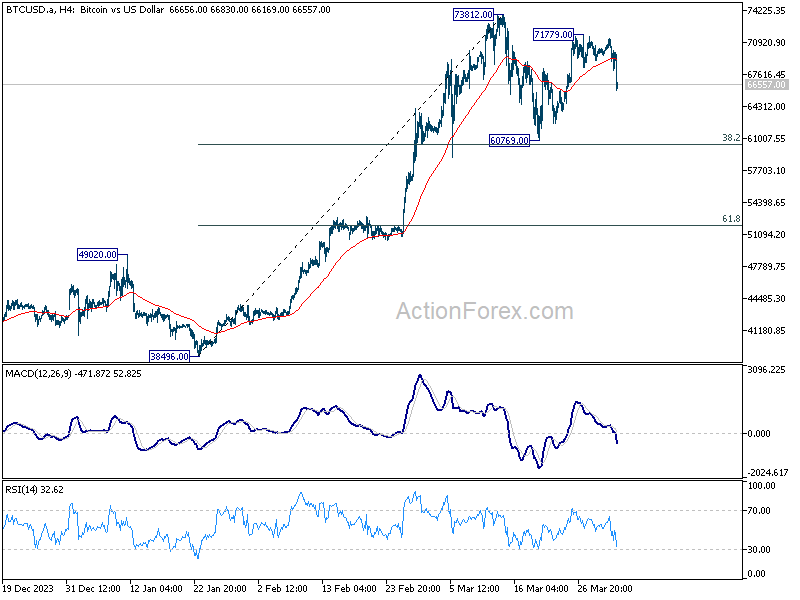

On the technical front, Bitcoin has experienced a sharp decline, indicating that the recent rebound from 60,769 may have reached its peak at 71,779. This suggests that the corrective pattern from 73,812 is entering its third leg, with a deeper fall anticipated back to 60,769. However, significant support is expected around the 38.2% retracement of 38,496 to 73,812 at 60,321, potentially marking the completion of the pattern. Consequently, a firm breach below the 60k threshold appears unlikely at this juncture. In essence, a firm breach of the 60k threshold seems unlikely at this juncture.

In Asia, at the time of writing, Nikkei is up 0.03%. Hong Kong HSI is up 2.25%. China Shanghai SSE is down -0.16%. Singapore Strait Times is up 0.30%. Japan 10-year JGB yield is up 0.0027 at 0.745. Overnight, DOW fell -0.60%. S&P 500 fell -0.20%. NASDAQ rose 0.11%. 10-year yield rose 0.123 to 4.329.

RBA minutes: No rate hike discussed, focus on preserving labor market gains

RBA’s minutes from March 18-19 meeting revealed no explicit discussion on rate hikes, marking a departure from previous communications that outlined the board’s considered options.

The board assessed that it would require more time to gain “sufficient confidence” in inflation’s return to target range within a foreseeable timeframe. At the same time, it emphasized on the priority to “preserve as many of the gains in the labor market as possible.”

These considerations led to the characterization of the policy outlook as ambiguous, with the board finding it “difficult to either rule in or out future changes” in the cash rate target.

Inflation remains elevated, albeit on a gradual decline towards the target, while labor market is approaching conditions synonymous with full employment. In light of these observations, maintaining the cash rate target unchanged was deemed the most suitable course of action.

The board also recognized that risks had become little more even”, noting that recent data did not suggest “materialisation of upside risks to inflation” and confirmed an anticipated slowdown in economic output.

RBNZ’s Orr asserts laser-focused commitment to inflation control

RBNZ Governor Adrian Orr articulated a firm stance today and emphasized that the committee is “laser-focused” on steering inflation back to its target range.

Orr’s acknowledged the progress and RBNZ is “on track” getting inflation back to targets. Yet he also tempers expectations by noting that the journey is far from complete with the admission that they are “not there yet.”

A critical element highlighted by Orr concerns inflation expectations, which he identifies as a significant challenge in the battle against rising He pointed out the cyclical nature of inflation expectations, stating, “the more people think inflation will rise next year, the more inflation will rise next year.”

Looking ahead

Swiss retail sales and PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final, and Germany CPI flash will be released in Euroepan session. Later in the day, US will release factory orders.

EUR/USD Daily Outlook

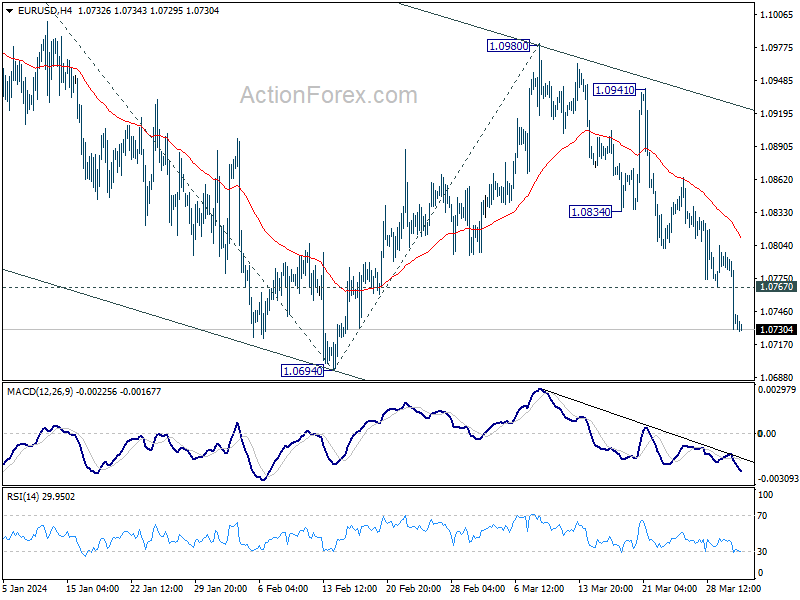

Daily Pivots: (S1) 1.0716; (P) 1.0758; (R1) 1.0784; More…

Intraday bias in EUR/USD stays on the downside for 1.0694 support. Decisive break there will resume the whole decline from 1.1138 and target 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536. On the upside, above 1.0767 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.0834 support turned resistance holds, in case of recovery.

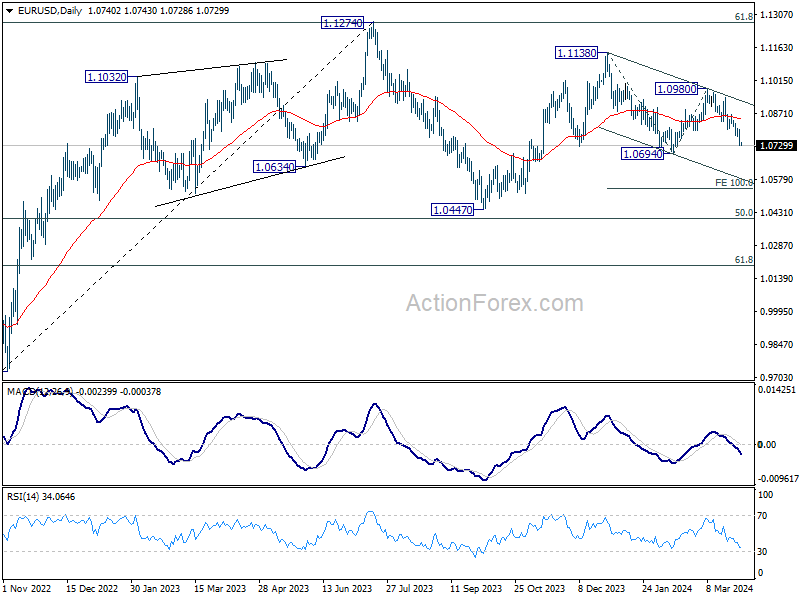

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Feb | 1.30% | 2.20% | 2.50% | |

| 23:50 | JPY | Monetary Base Y/Y Mar | 1.60% | 2.50% | 2.40% | |

| 00:00 | AUD | TD Securities Inflation M/M Mar | 0.10% | -0.10% | ||

| 00:30 | AUD | RBA Meeting Minutes | ||||

| 06:30 | CHF | Real Retail Sales Y/Y Feb | 0.40% | 0.30% | ||

| 07:30 | CHF | Manufacturing PMI Mar | 44.9 | 44 | ||

| 07:45 | EUR | Italy Manufacturing PMI Mar | 48.8 | 48.7 | ||

| 07:50 | EUR | France Manufacturing PMI Mar F | 45.8 | 45.8 | ||

| 07:55 | EUR | Germany Manufacturing PMI Mar F | 41.6 | 41.6 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Mar F | 45.7 | 45.7 | ||

| 08:30 | GBP | Mortgage Approvals Feb | 57K | 55K | ||

| 08:30 | GBP | M4 Money Supply M/M Feb | 0.20% | -0.10% | ||

| 08:30 | GBP | Manufacturing PMI Mar F | 49.9 | 49.9 | ||

| 12:00 | EUR | Germany CPI M/M Mar P | 0.40% | 0.40% | ||

| 12:00 | EUR | Germany CPI Y/Y Mar P | 2.40% | 2.70% | ||

| 14:00 | USD | Factory Orders M/M Feb | 1.00% | -3.60% |

When The Wave Turns

Why Retirement Investing Is Moving Towards Resilience Jeremy Grantham’s latest market warnings have revived an old tru... Read more

Gyrostat Capital Management: July Retirement Portfolio Resilience Assessment

The Market Is Currently Presenting an Opportunity to Strengthen Retirement Portfolio Resilienc... Read more

The Invisible Risk That Decides Your Retirement

Why how investors behave matters more than what markets do and what disciplined port... Read more

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more