Dollar Steady After PCE, Euro Finds Support On ECB Survey

The forex markets are relatively steady in early US trading, with most pairs consolidating after a week of sharp moves. The latest batch of US data offered few surprises, leaving traders reluctant to push directional bets ahead of next week’s pivotal employment report.

US PCE inflation for August came in broadly in line with expectations, confirming that disinflation has stalled for now. Meanwhile, spending remained resilient, highlighting the strength of US demand. The combination gives the Fed every reason to proceed cautiously.

That caution, however, does not rule out further easing. Officials have stressed the need to insure against risks to employment, and a weak non-farm payrolls report next week could quickly tilt the balance toward another cut.

For now, the Dollar looks set to digest some of this week’s gains into the weekly close. Positioning remains constructive after strong GDP, claims, and durable goods data earlier in the week, but the lack of fresh catalysts is tempering momentum.

Elsewhere, Euro is holding slightly firmer after the ECB’s consumer survey showed inflation expectations ticking higher. That supports the case for the ECB to remain on hold, barring a steep downturn in growth. Canadian Dollar, by contrast, showed little reaction to stronger-than-expected July GDP as advance data signaled stagnation in August, leaving recovery fragile.

Overall on the week, Dollar leads the performance board, followed by Swiss Franc and Euro. At the bottom, Kiwi lags behind, with Loonie and Yen also weak. Sterling and the Aussie sit mid-pack.

In Europe, at the time of writing, FTSE is up 0.61%. DAX is up 0.77%. CAC is up 0.86%. UK 10-year yield fell -0.022 to 4.737. Germany 10-year yield fell -0.027 to 2.748. Earlier in Asia, Nikkei fell -0.87%. Hong Kong HSI fell -1.35%. China Shanghai SSE fell -0.65%. Singapore Strait Times fell -0.18%. Japan 10-year JGB yield rose 0.01 to 1.659.

US PCE inflation matches forecasts, income and spending beat

US inflation data for August came in largely as expected. Headline PCE rose 2.7% yoy, slightly up from July’s 2.6%. Core PCE held steady at 2.9% yoy. On the month, headline and core rose 0.3% mom and 0.2% mom, respectively, both in line with consensus.

Beyond inflation, the demand side showed more momentum. Personal income climbed 0.4% mom, above the 0.3% forecast. Personal spending gained 0.6% mom, also beating estimates of 0.5%.

For the Fed, the data reinforces the case for continued but measured easing. Inflation progress remains gradual, while firmer demand signals that the economy is not yet at risk of stalling.

Canada GDP rebounds 0.2% mom in July, first gain in four months

Canada’s GDP expanded 0.2% mom in July, beating expectations of 0.1% and marking the first increase in four months. The rebound was driven primarily by goods-producing industries, which rose 0.6% mom after three straight months of contraction, with every sector in the grouping recording gains.

Services output was more subdued, rising just 0.1% mom as wholesale trade and real estate contributed modestly while retail trade slipped. In total, only 11 of 20 industrial sectors posted growth.

Looking ahead, advance estimates suggest GDP was flat in August, with gains in wholesale and retail offset by declines in resource extraction, manufacturing, and transport.

ECB consumer survey: Inflation expectations edge higher, growth outlook weak

Eurozone households lifted their inflation expectations in August, according to the ECB’s latest survey. Median expectations for the next 12 months rose to 2.8% from 2.6% in July, while five-year expectations climbed from 2.1% to 2.2%, the highest since August 2022. Three-year expectations were steady at 2.5%.

At the same time, the growth outlook remained grim, with respondents predicting output to shrink by -1.2% over the next 12 months. Job worries also inched higher, with unemployment expectations up to 10.7% from 10.6%.

The survey highlights a lingering inflation mindset among households, even as economic prospects stay fragile. For the ECB, the persistence of medium-term price expectations near or above target may limit the scope for further easing if growth continues to stagnate.

Tokyo CPI core stays at 2.5% in September, core-core slows

Tokyo inflation came in softer than expected in September, with core CPI (ex-fresh food) unchanged at 2.5% yoy versus forecasts of 2.8% yoy. The moderation was largely attributed to measures by the metropolitan government, including cuts to childcare fees and water charges, easing some of the burden from rising living costs.

Core-core inflation, stripping out fresh food and energy, slowed sharply from 3.0% yoy to 2.5% yoy, while headline CPI was also steady at 2.5% yoy. Food inflation excluding fresh items cooled to 6.9% yoy from 7.4% yoy, highlighting a broadening slowdown in price pressures.

The weaker data may give the BoJ some breathing room, though markets still price another 25bps hike in the months ahead. Opinion remains divided on whether policymakers act as soon as October or hold off until January.

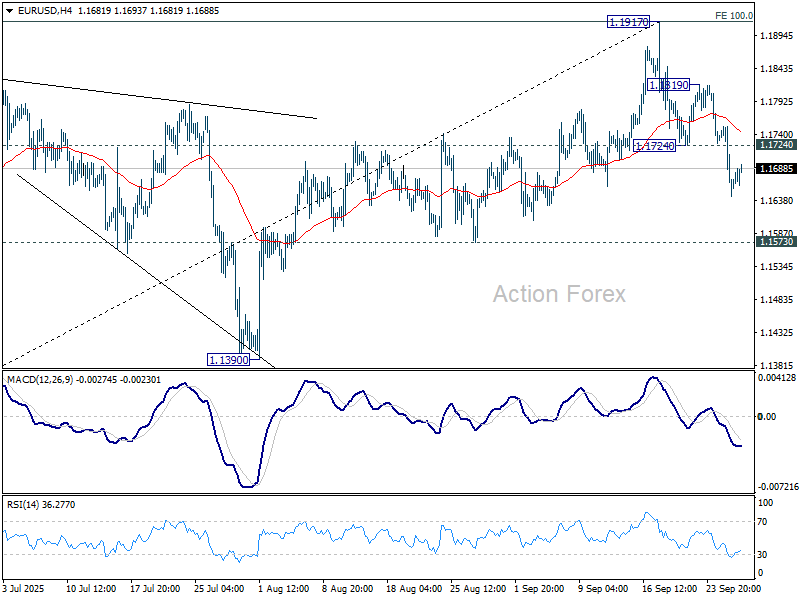

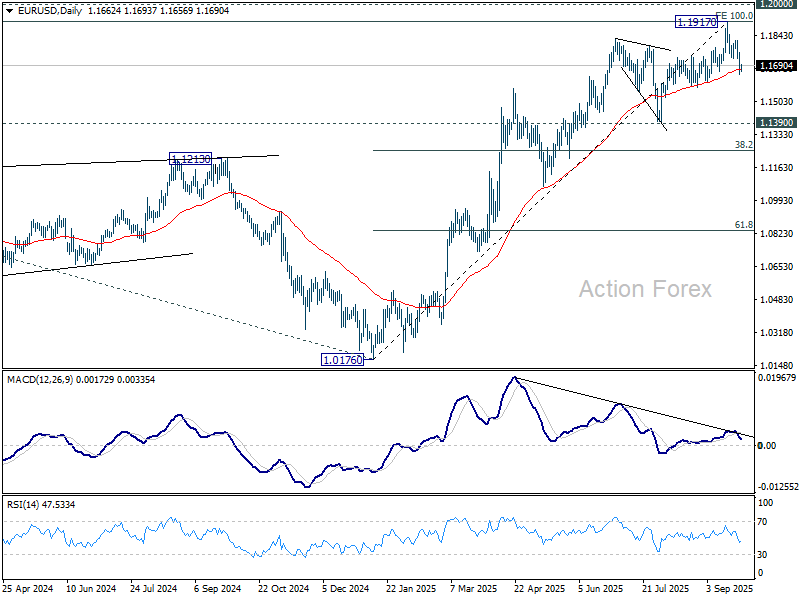

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1622; (P) 1.1688; (R1) 1.1732; More…

Intraday bias in EUR/USD stays mildly on the downside for the moment. Considering bearish divergence condition in D MACD, sustained break of 55 D EMA (1.1667) will argue that 1.1917 is already a medium term top. Deeper fall should then be seen to 1.1390 support next. On the upside, above 1.1734 support turned resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1819 resistance holds, in case of recovery.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1214).

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more