Dollar Stays Weak As Trump Pivots From Maximum Pressure To Reconstruction Mode In Iran

The war premium is fading—and with it, the Dollar’s support. The greenback stayed under pressure in Asian session as oil prices retreated on renewed optimism that US-Iran talks could resume within the next two days. More importantly, markets are picking up on a subtle but meaningful shift in US strategy, with President Donald Trump’s latest remarks suggesting negotiations could move directly toward a deal, even without extending the current ceasefire.

“It could end either way, but I think a deal is preferable because then they can rebuild,” he said, adding that “we took out the radicals.” The messaging points to a transition from a “maximum pressure” stance toward what can be interpreted as a “reconstruction-focused” approach, where the objective shifts from coercion to settlement.

However, the refusal to extend the ceasefire is a double-edged sword—it signals confidence that a deal is close, but also creates a hard deadline that could quickly reintroduce volatility if talks fail to deliver.

Meanwhile, the broader macro debate remains unsettled. The International Monetary Fund has highlighted the risk of slower growth and higher inflation stemming from the Middle East conflict, warning of significant downside risks to the global economy. In contrast, US Treasury Secretary Scott Bessent pushed back against the more pessimistic global outlook, dismissing the IMF’s warnings of slower growth and higher inflation as an “overreaction.”

Speaking to reporters, he argued that while energy prices may rise in the near term, the US economy is well positioned to absorb the shock. “I think that they probably overreacted, but we’ll see,” he said, signaling confidence that inflation pressures would not become entrenched.

Bessent drew a clear distinction between the US and other major economies. He suggested that countries in Europe and Asia are more likely to rely on consumer or industrial subsidies to cushion the impact of higher energy costs—policies he views as counterproductive. In his view, such interventions risk prolonging inflation by keeping prices artificially elevated while also increasing government borrowing, effectively embedding inflationary pressures for longer.

However, Bessent’s confidence hinges heavily on the geopolitical outcome. If negotiations fail and the ceasefire expires without a deal, the war premium could return sharply to energy markets, potentially validating the IMF’s more cautious scenario of persistent inflation and weaker growth.

Another key development—largely flying under the radar—is the rollout of the CAPE system for tariff refunds next Monday. US authorities confirmed that the system is ready to begin issuing refunds totaling around USD 166B to American importers, following the Supreme Court’s decision to strike down the tariffs as unlawful.

This represents a sizable and unexpected liquidity injection. For businesses, the refunds improve cash flow and balance sheet flexibility at a time when input costs remain volatile. In macro terms, it functions as a stealth stimulus, supporting demand without requiring new fiscal legislation.

The timing is particularly important. As geopolitical risks and energy price swings cloud the outlook, the CAPE-driven cash injection could help cushion the domestic economy. It also reinforces the narrative that the US may be better positioned than its peers to absorb external shocks.

In the currency markets, Dollar remains the worst performer for the week so far, followed by Yen, and then Loonie. Kiwi is the best, followed by Aussie, and then Swiss Franc. Euro and Sterling are positioning in the middle.

In Asia, at the time of writing, Nikkei is up 0.33%. Hong Kong HSI is up 0.41%. China Shanghai SSE is up 0.26%. Singapore Strait Times is up 0.28%. Japan 10-year JGB yield is down -0.012 at 2.408. Overnight, DOW rose 0.66%. S&P 500 rose 1.18%. NASDAQ rose 1.96%. 10-year yield fell -0.041 to 4.256.

WTI Drops Below $90, $80 Next If US-Iran Talks Deliver ‘Bridge Deal’

WTI has slipped below $90 as markets bet a second round of US-Iran talks could deliver a ceasefire extension or even a “bridge deal,” paving the way toward $80. With the war premium unwinding, traders are front-running a path to de-escalation rather than waiting for confirmation. Read more.

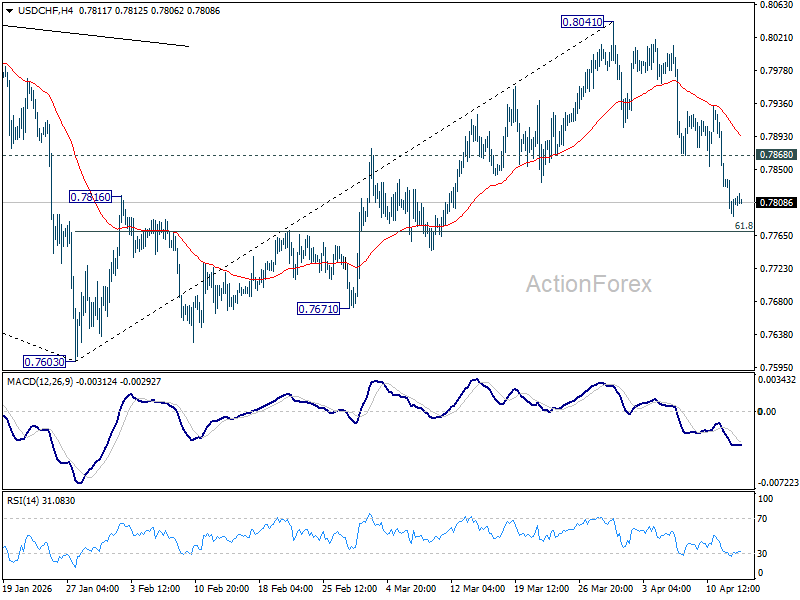

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7785; (P) 0.7814; (R1) 0.7838; More….

Intraday bias in USD/CHF remains on the downside at this point. Fall from 0.8041 is in progress for 61.8% retracement of 0.7603 to 0.8041 at 0.7770. Decisive break there will target a retest on 0.7603 low. On the upside, above 0.7868 minor resistance will turn intraday bias neutral first.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8071) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it’s probably correcting the larger scale down trend from 1.0146 (2022 high).

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more