Dollar Slightly Softer As Bessent Warns Shutdown Could Hit GDP

Dollar is slightly softer today but not under heavy selling pressure. US Treasury Secretary Scott Bessent cautioned in a CNBC interview that the current government shutdown could hurt economic performance. “We could see a hit to the GDP, a hit to growth and a hit to working America,” he warned, adding that such brinkmanship is “not the way to have a discussion.”

While the shutdown so far has had little direct impact on sentiment, the risk of delayed economic data releases, including nonfarm payrolls, continues to hang over markets. That uncertainty, combined with softer labor signals, has capped the Dollar’s upside.

Meanwhile, Yen’s broad-based strength extended, supported by remarks from BoJ Deputy Governor Shinichi Uchida. His comments were not groundbreaking but were interpreted as upbeat, particularly in his reference to receding uncertainty around US tariffs, which investors see as reinforcing the BoJ’s direction toward further rate hikes.

Still, Uchida offered no firm signal on timing, leaving markets uncertain about whether the BoJ will move as soon as this month. Traders are now looking ahead to Governor Kazuo Ueda’s speech tomorrow, which may provide clearer guidance on whether October or December is the more likely window for another hike.

In terms of weekly performance, Yen remains the strongest currency, followed by Aussie and Kiwi, both supported by risk-on sentiment in Asia-Pacific. Loonie and Dollar sit at the bottom of the table, while Euro, Sterling, and Swiss Franc are trading mixed in the middle.

In Europe, at the time of writing, FTSE is up 0.04%. DAX is up 1.38%. CAC is up 1.38%. Germany 10-year yield is down -0.003 at 2.715. UK 10-year yield is up 0.027 at 4.722. Earlier in Asia, Nikkei rose 0.87%. Hong Kong HSI rose 1.61%. China was on holiday. Singapore Strait Times rose 1.67%. Japan 10-year JGB yield rose 0.014 to 1.666.

BoE survey shows inflation expectations edge higher, uncertainty still elevated

UK firms reported a slight uptick in inflation expectations in September, according to the BoE’s Decision Maker Panel survey. Year-ahead CPI expectations rose by 0.1 percentage point to 3.4%, while three-year expectations were unchanged at 2.9%.

Wage growth expectations held steady at 3.6% on a three-month basis, though the single-month figure rose by 0.3 percentage points to 3.8%.

The survey highlighted ongoing concerns around the business outlook. Some 58% of firms judged overall uncertainty as high or very high, up slightly from 57% in August. That said, uncertainty surrounding year-ahead sales dipped marginally to 4.3%, while price uncertainty was unchanged at 1.7%, both far below the levels seen during past peaks.

Swiss CPI holds low 0.2% in September, core steady at 0.7%

Swiss consumer prices dipped -0.2% mom in September, in line with expectations. Core CPI also dropped -0.2% mom. Domestic product prices fell -0.3% mom while imported product prices slipped -0.1% mom.

On an annual basis, headline CPI was unchanged at 0.2% yoy, slightly below the 0.3% forecast but positive for a fourth straight month.

Core inflation, excluding fresh and seasonal items as well as energy, held steady at 0.7% yoy. Domestic prices were unchanged at 0.6% yoy. Imported prices swung higher, rising to -0.9% yoy from -1.3% previously.

BoJ’s Uchida: Economy resilient, inflation to re-accelerate gradually

BoJ Deputy Governor Shinichi Uchida highlighted resilience in Japan’s economy, pointing to positive corporate sentiment in the Tankan survey and improved manufacturer outlooks as trade uncertainty with the US has eased. He noted that despite tariff-related profit pressures for some firms, revenues remain elevated, capital expenditure is trending higher, and consumption is firm.

On inflation, Uchida said underlying price growth may stagnate in the near term but should re-accelerate gradually as expectations rise. This suggests the BoJ continues to see progress toward achieving its price stability goal, albeit at a measured pace.

Reaffirming the policy stance, Uchida said the BoJ will continue lifting rates if economic and price trends evolve as projected, while remaining data-dependent. He stressed that decisions will be guided by evidence, not pre-set commitments.

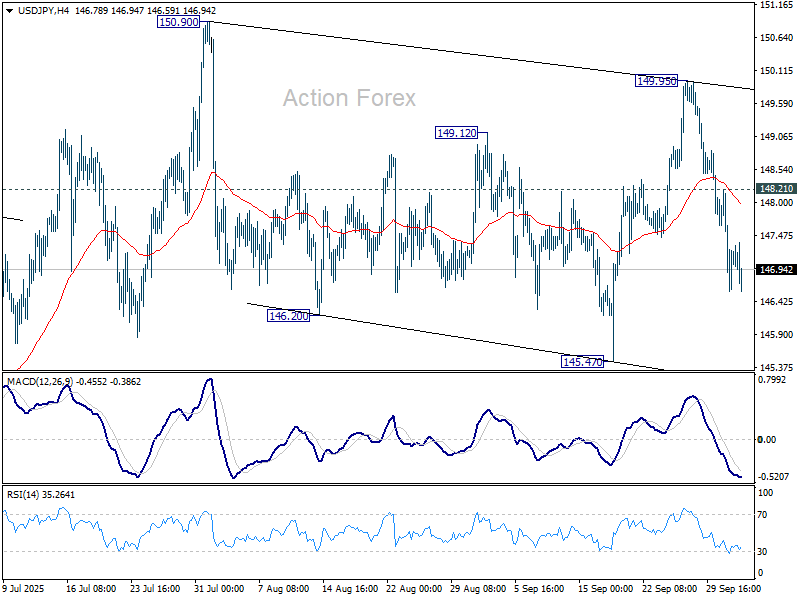

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.37; (P) 147.30; (R1) 148.01; More…

USD/JPY’s fall from 149.95 continues today and intraday bias stays on the downside for 145.47. Strong support from there will keep the pattern from 150.90 corrective. That is, rise from 139.87 would still be in favor to resume at a later stage. On the upside, above 148.12 minor resistance will turn intraday bias neutral first. However, decisive break of 145.47 will indicate near term reversal, and bring deeper fall to 142.66 support next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more