Dollars Dominance Continues, Sterling And Euro Accelerate Down

Dollar’s robust rally persists in early US session, and gains momentum alongside the strong rise 10-year yield, now surpassing the 4.1% mark. Fed Chair Jerome Powell’s hawkish comments in CBS interview air during the weekend continued to shift market expectations. The probability of Fed holding interest rate unchanged in March has soared to approximately 85%, with the anticipation of a May rate cut dropping to just over 60%. It’s important to note, though, that these expectations could shift in response to the forthcoming ISM Services data, which remains a crucial determinant of market sentiment.

In terms of currency strength, Japanese Yen emerges as the runner-up, with New Zealand Dollar not far behind. This scenario, however, reflects more on the deeper depreciation of other currencies rather than intrinsic strength in Yen and Kiwi. On the other end of the spectrum, Euro and Sterling are the worst performers, finding themselves under considerable pressure against Dollar. Australian Dollar is also soft, and appears susceptible to dovish surprises from RBA in the upcoming Asian session. Meanwhile, Canadian Dollar and Swiss Franc show mixed performances, finding themselves in the market’s middle ground.

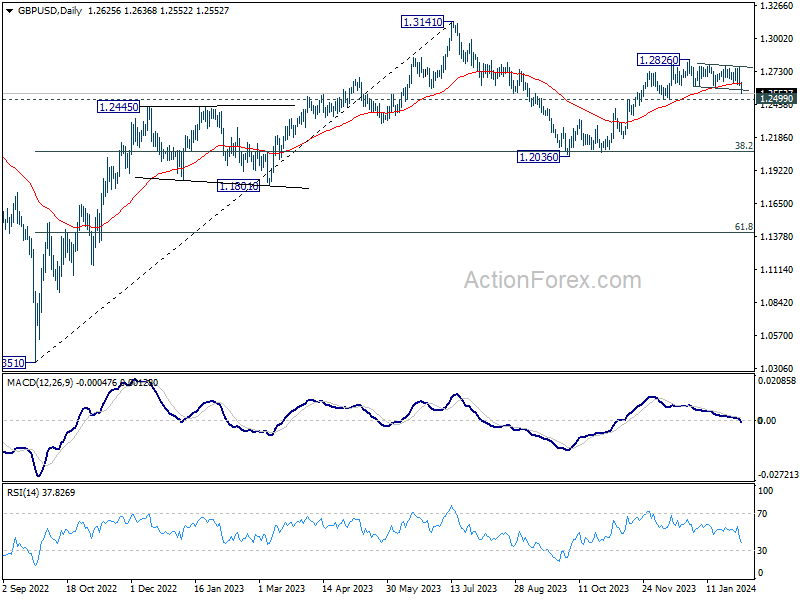

Technically, as Dollar advances, a focus will be on 1.2499 support in GBP/USD. Sustained break there will argue that whole rise from 1.2036 has completed, as the second leg of the corrective pattern from 1.3141 high. If realized, that would turn outlook bearish for 1.2036, as the third leg of the pattern progresses.

In Europe, at the time of writing, FTSE is up 0.31%. DAX is down -0.09%. CAC is down -0.12%. UK 10-year yield is up 0.077 at 4.008. Germany 10-year yield is up 0.0698 at 2.310. Earlier in Asia, Nikkei rose 0.54%. Hong Kong HSI fell -0.15%. China Shanghai SSE fell -1.02%. Singapore Strait Times fell -1.43%. Japan 10-year yield rose 0.0598 to 0.720.

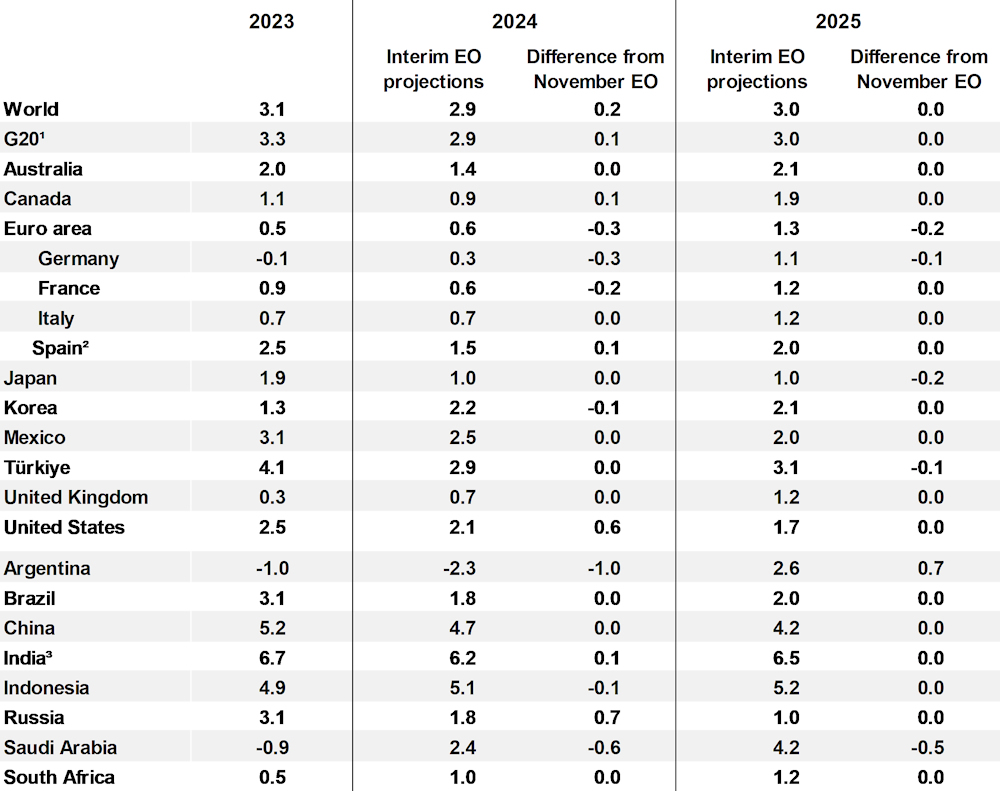

OECD raises global growth forecasts to 2.9% in 2024 on robust US performance

OECD’s latest Interim Economic Outlook report presents a cautiously optimistic upgrade in global growth forecasts for 2024 to 2.9% (up from November’s 2.7% forecast), a notable uplift largely attributed to stronger performance of US economy.

“Some moderation of growth” from 2023 is expected, under the influence of tighter financial conditions affecting credit and housing markets, alongside a subdued global trade dynamics. Recent attacks on ships in the Red Sea have introduced further volatility and exert upward pressure on prices.

Despite some moderation in growth and the ongoing adjustments to tighter financial conditions, OECD cautions that it is “too soon to be sure that underlying price pressures are fully contained.” Labor markets showing signs of equilibrium bring a positive note, yet the persistently high unit labor cost growth looms as a challenge for meeting medium-term inflation targets.

The specter of high geopolitical tension, particularly in the Middle East, poses a “significant near-term risk to activity and inflation”, with potential disruptions in energy markets likely to have far-reaching consequences. Furthermore, persistent service price pressures could lead to inflation surprises, necessitating reevaluation of monetary policy easing expectations. On the other hand, growth could be weaker if effects of past monetary tightening are stronger than expected.

Here are some details.

- Global growth forecast for 2024 raised up by 0.2% to 2.9%. 2025 unchanged at 3.0%.

- US growth forecast for 2024 raised by 0.6% to 2.1%. 2025 unchanged at 1.7%.

- Eurozone growth forecast for 2024 lowered by -0.3% to 0.6%, 2025 down by -0.2% to 1.3%.

- Japan’s growth forecast for 2024 unchanged at 1.0%. 2025 lowed by -0.2% to 1.0%.

- China’s growth forecast for 2024 unchanged at 4.7%. 2025 unchanged at 4.2%.

Eurozone Sentix rises to -12.9, Germany a negative economic pull

Eurozone Sentix Investor Confidence index climbed for the fourth consecutive month to -12.9, marking its highest point since April 2023. Both Current Situation Index, now at -20.0 (its peak since June 2023), and Expectations Index, reaching -5.5 (the highest since February 2022), have shown similar upward trends, indicating gradual improvement in investor sentiment across the region.

Despite these positive trends, Sentix highlighted that the Eurozone continues to grapple with recessionary pressures. For a genuine economic turnaround, the expectation values need to shift into positive territory.

Germany emerges as a primary concern, acting as the “negative economic pull” for Eurozone. Germany’s investor confidence dipping further from -26.1 to -27.1. Current Situation Index worsened to -39.3, but there’s a silver lining as Expectations Index improved to -14.0, reaching its highest since April 2023.

Eurozone PPI down -0.8% mom, -10.6% yoy in Dec

Eurozone PPI was down -0.8% mom, -10.6% yoy in December, versus expectation of -0.8% mom, -10.6% yoy. For the month, industrial producer prices decreased by -2.3% mom for energy and by -0.3% mom for intermediate goods, while prices remained stable for both capital goods and durable consumer goods, and prices increased by 0.1% mom for non-durable consumer goods. Prices in total industry excluding energy decreased by -0.1% mom.

EU PPI was down -0.9% mom, -10.0% yoy. The largest monthly decreases in industrial producer prices were recorded in Ireland (-12.0%), the Netherlands (-1.8%) and Estonia (-1.4%), while increases were observed in Greece (+1.0%), Belgium (+0.5%), Cyprus and Luxembourg (both +0.3%) as well as in France (+0.1%).

Eurozone PMI services finalized at 48.4, Southern strength versus Northern softness

Eurozone PMI Services was finalized at 48.4 in January, down slightly from December’s 48.8. PMI Composite was finalized at 47.9, up from prior month’s 47.6, a 6-month high.

The data reveals a striking “north-south divide”, challenging conventional perceptions. Spain and Italy, with Composite PMIs of 51.5 and 50.7 respectively, outperform their northern peers, Germany (47.0) and France (44.6).

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that ECB caution regarding interest rate cuts is justified by the rising price indices, reflecting increasing input and output prices in the services sector. This inflationary pressure complicates ECB’s decisions, especially in light of the latest GDP data for Q4 2023, which showed the eurozone narrowly avoiding a technical recession.

The persistent eurozone-wide labor shortage, leading to wage increases and input price inflation, especially in the top economies, indicates a cautious approach to workforce reductions, even in weaker service sectors of Germany and France.

UK PMI services finalized at 54.3, revival gained momentum

UK PMI Services was finalized at 54.3 in January, up from December’s 53.4. PMI Composite was finalized at 52.9, up from prior month’s 52.1.

Tim Moore from S&P Global noted the service sector’s performance revival, with output growth at its fastest in eight months due to increased business and consumer spending. New orders have rebounded, driven by diminishing recession fears and more flexible financial conditions.

Inflationary pressures eased in January, despite demand surge, with input costs rising at one of the slowest rates in three years. This slowdown is attributed to reduced energy, fuel, and raw material costs. However, service providers still face elevated wage pressures, contributing to a continued, albeit slower, rise in prices charged.

Japan’s PMI services finalized at 53.1, fueling overall economic growth

Japan’s PMI Services was finalized at 53.1 in January, marking a continuous expansion for the 17th month and an improvement from December’s 51.5. PMI Composite was finalized at 51.5, up from prior month’s 50.0, indicating a modest uptick in overall private sector activity for the first time since October.

According to Usamah Bhatti, Economist at S&P Global Market Intelligence, key observations include accelerated growth in business activity, new orders, and the first rise in exports in five months.

Capacity pressures intensified, with the strongest backlog increase since last June and a sharper job creation rate. Business confidence for the year ahead hit an eight-month high, reflecting robust optimism.

China’s PMI services dips slightly to 52.7, significant challenges remain

In January, China’s Caixin PMI Services slightly decreased to 52.7 from 52.9, aligning with expectations. PMI Composite also and a minor reduction to 52.5 from 52.6.

Wang Zhe, Senior Economist at Caixin Insight Group, pointed out that the economy faces “significant challenges” including tepid demand, increased employment pressures, and subdued market expectations, indicating that “This status quo has yet to experience a fundamental reversal.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0747; (P) 1.0822; (R1) 1.0864; More…

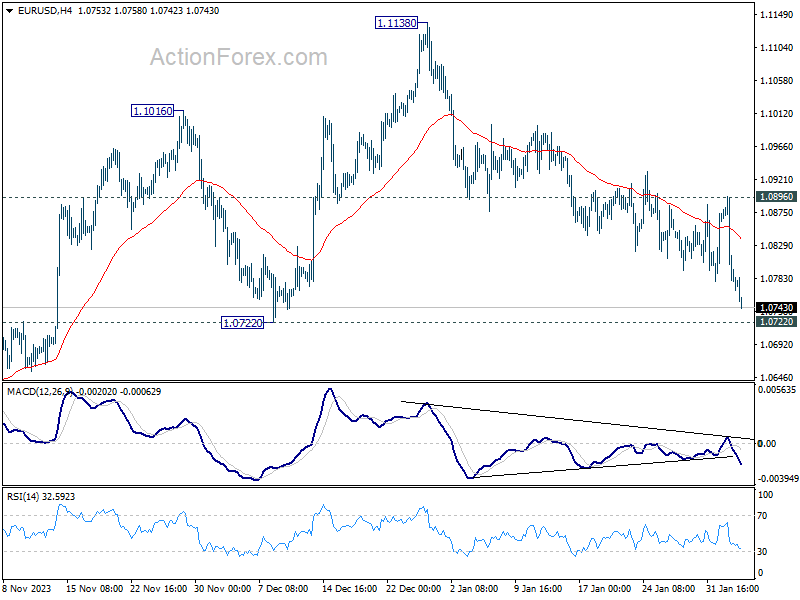

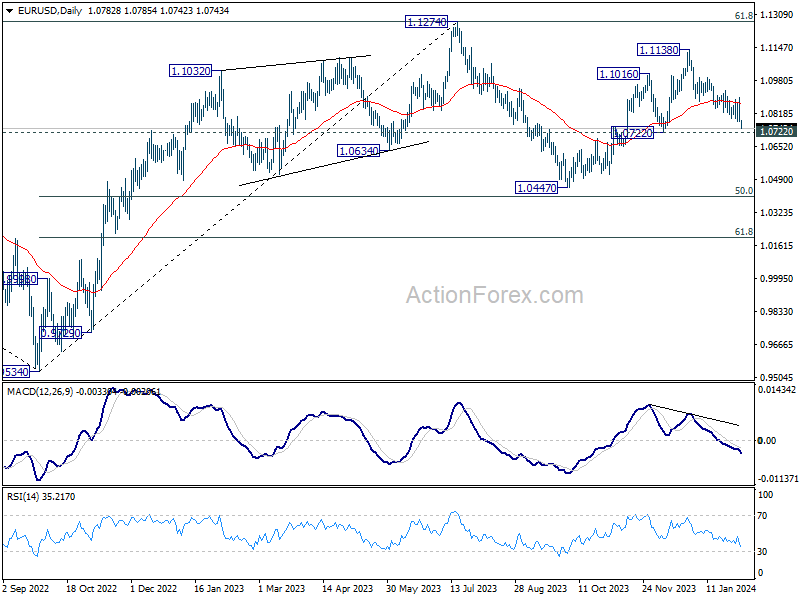

EUR/USD’s fall from 1.1138 continues today, and the break of trend line in 4H MACD indicates downside acceleration. Intraday bias remains on the downside. Sustained break of 1.0722 structural support will argue that whole rise from 1.0447 has completed. Deeper fall would then be seen to target this low. On the upside, break of 1.0896 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | TD Securities Inflation M/M Jan | 0.30% | 1.00% | ||

| 00:30 | AUD | Goods Trade Balance (AUD) Jan | 10.96B | 10.50B | 11.44B | |

| 01:45 | CNY | Caixin Services PMI Jan | 52.7 | 52.7 | 52.9 | |

| 07:00 | EUR | Germany Trade Balance (EUR) Dec | 22.2B | 22.3B | 20.4B | |

| 08:45 | EUR | Italy Services PMI Jan | 51.2 | 50.8 | 49.8 | |

| 08:50 | EUR | France Services PMI Jan F | 45.4 | 45 | 45 | |

| 08:55 | EUR | Germany Services PMI Jan F | 47.7 | 47.6 | 47.6 | |

| 09:00 | EUR | Eurozone Services PMI Jan F | 48.4 | 48.4 | 48.4 | |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Feb | -12.9 | -15 | -15.8 | |

| 09:30 | GBP | Services PMI Jan F | 54.3 | 53.8 | 53.8 | |

| 10:00 | EUR | Eurozone PPI M/M Dec | -0.80% | -0.80% | -0.30% | |

| 10:00 | EUR | Eurozone PPI Y/Y Dec | -10.60% | -10.50% | -8.80% | |

| 14:45 | USD | Services PMI Jan F | 52.9 | 52.9 | ||

| 15:00 | USD | ISM Services PMI Jan | 52.1 | 50.6 |

When The Wave Turns

Why Retirement Investing Is Moving Towards Resilience Jeremy Grantham’s latest market warnings have revived an old tru... Read more

Gyrostat Capital Management: July Retirement Portfolio Resilience Assessment

The Market Is Currently Presenting an Opportunity to Strengthen Retirement Portfolio Resilienc... Read more

The Invisible Risk That Decides Your Retirement

Why how investors behave matters more than what markets do and what disciplined port... Read more

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more