Dollar Resilient As Trust Gap Offsets Peace Pivot

Dollar remained resilient as markets attempted to price in a tentative “peace pivot”, but with skepticism over its credibility limiting any sustained risk rally. Asian equities opened higher following the rebound in US markets overnight, but gains were modest, with major indexes recovering only about half of the previous day’s losses.

The initial optimism was driven by US President Donald Trump’s decision to postpone planned strikes on Iranian energy infrastructure for five days after what he described as “very good and productive” conversations. The announcement encouraged markets to unwind some of the extreme escalation risks that had been priced in following the earlier 48-hour ultimatum.

However, this narrative quickly ran into a credibility wall. Tehran dismissed the claims as “fake news” and “psychological warfare,” casting doubt on whether any meaningful diplomatic progress had been made. The conflicting signals have left markets hesitant to fully embrace the idea of de-escalation.

On the ground, developments have reinforced this caution. Reports of explosions over Jerusalem following Iranian missile fire highlight that hostilities remain active despite the rhetoric of talks. This disconnect between words and actions has kept investors wary of a sudden “snap-back” in tensions.

Oil markets reflect this skepticism. Brent crude rebounded back above 100, indicating that traders are not pricing in a lasting resolution. The persistence of elevated oil prices continues to anchor inflation expectations and limit the scope for a broader risk-on move. In equities, the muted rebound underscores the lack of conviction. The market is effectively caught between relief from delayed escalation and concern over unresolved risks.

Currency markets are showing a clearer expression of this dynamic. Dollar is the strongest performer for the day so fart. Yen is also firm on safe-haven demand, while Canadian Dollar benefits from oil strength. In contrast, Australian and New Zealand Dollars remain under pressure, reflecting their sensitivity to global growth and Asia-linked risks. Sterling is also softer, while Euro and Swiss Franc are trading in the middle as markets await clearer direction.

The next 96 hours are critical. The five-day pause is conditional on the “success of ongoing meetings,” leaving open the possibility that the original threat to strike Iranian infrastructure could return if progress stalls. This binary outcome is keeping volatility elevated.

Until there is concrete evidence of de-escalation—either through a joint statement or the reopening of the Strait of Hormuz—markets are likely to remain trapped in a headline-driven cycle. For now, the dominant theme is cautious positioning, with the Dollar’s resilience reflecting a market that is not yet ready to fully price in peace.

Elsewhere, Australia and the European Union formally signed a long-awaited free trade agreement after years of negotiations. The deal removes tariffs on Australian critical minerals, and includes a broader Security and Defense Partnership.

The agreement is being framed as a move toward supply chain diversification at a time of heightened geopolitical risk. By opening European markets further to Australian resources, it reduces reliance on China while strengthening support for the global energy transition, particularly in critical mineral supply chains.

In Asia, at the time of writing, Nikkei is up 0.43%. Hong Kong HSI is up 1.32%. China Shanghai SSE is up 0.64%. Singapore Strait Times is up 0.15%. Japan 10-year JGB yield is down -0.042 at 2.280. Overnight, DOW rose 1.38% S&P 500 rose 1.15%. NASDAQ rose 1.38%. 10-year yield fell -0.057 to 4.334.

Japan core CPI falls to 1.7% in February, as energy costs drag inflation lower

Japan CPI data point to easing inflation momentum driven by energy costs, though core-core inflation suggests underlying pressures remain. Read more.

Japan PMI composite falls to 52.5, war lifts costs and hits sentiment

Japan’s PMI data show growth cooling as input costs surge and business sentiment weakens. The Middle East conflict is lifting energy prices and disrupting supply chains, squeezing margins and raising uncertainty. Read more.

Australia PMI composite falls to 47, cost inflation hits 3-yr high on Middle East conflict

Australia’s PMI data signal a sharp shift into contraction as demand weakens and cost inflation surges to a three-year high. The combination highlights early stagflation risks as the Middle East shock begins to hit growth and prices. Read more.

RBNZ’s Breman warns of inflation spike but cautions against overreaction

RBNZ Governor Anna Breman warns the Middle East conflict will lift inflation while weighing on growth, but stresses policy must avoid overreacting to temporary shocks. The focus remains on preventing short-term price spikes from becoming persistent inflation. Read more.

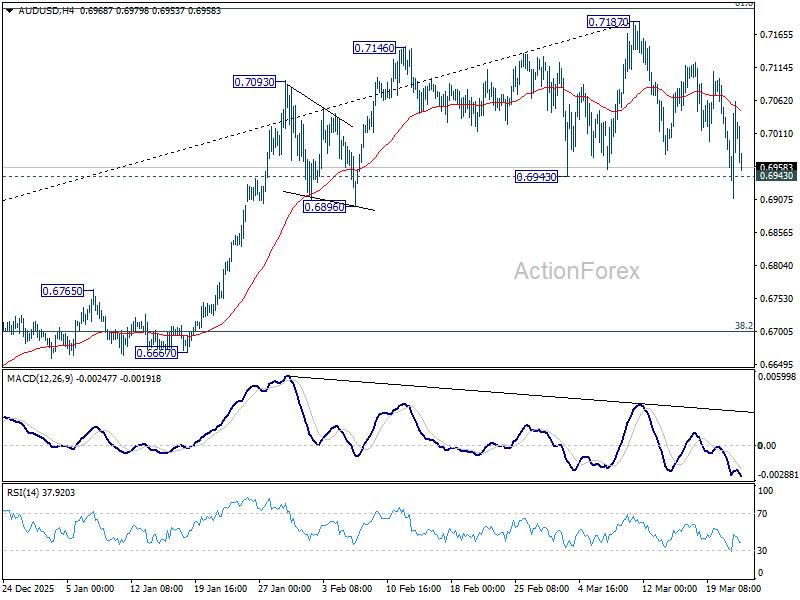

AUD/USD Daily Report

Daily Pivots: (S1) 0.6927; (P) 0.6995; (R1) 0.7079; More...

Focus stays on 0.6943 support in AUD/USD after the volatility in the last 24 hours. Decisive break there should confirm rejection by 0.7206 key fibonacci resistance. That would set up deeper correction to the whole up trend from 0.5913, and target 38.2% retracement of 0.5913 to 0.7187 at 0.6700. Nevertheless, strong rebound from current levels would retain near term bullishness for breakout through 0.7187 at a later stage.

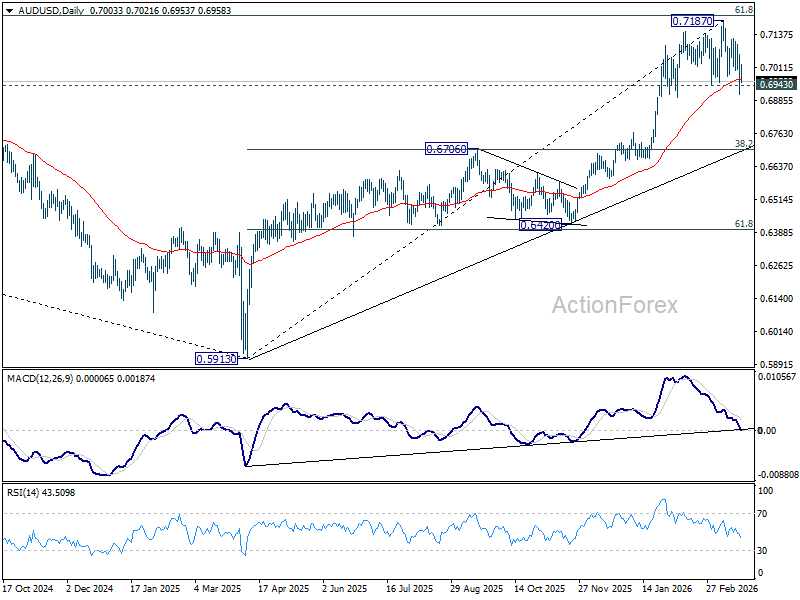

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will pave the way back to 0.8006. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more