Dollar rebounded in early US session following the better-than-expected June non-farm payrolls report, further reversing much of the week’s earlier weakness. While not a blowout, the report showed a labor market that remains fundamentally resilient, and significantly reduces pressure on the Fed to pull the trigger at the July meeting.

Fed Chair Jerome Powell and his like-minded colleagues have been clear they want more clarity on trade policy and inflation before moving. Today’s data buys the Fed more time to assess broader risks. The drop in wage growth could help the case for resuming cuts later this year, but not imminently.

On Capitol Hill, political developments are also in focus. House Republicans overnight broke a legislative deadlock and advanced President Donald Trump’s massive tax-and-spending bill. With the Senate already having passed the measure, attention turns to a final House vote, potentially before July 4.

In currency markets, Dollar is leading gains today, and it’s no longer at the bottom of the weekly performance ladder. Loonie and Sterling are also firming, while Kiwi, Yen, and Aussie lag. Euro and Swiss Franc are positioning in the middle.

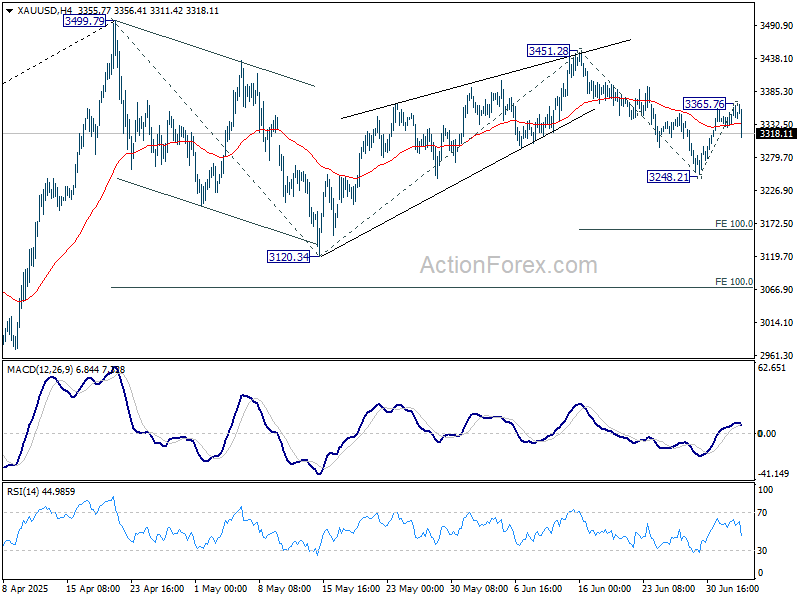

Technically, Gold falls sharply as rebound from 3248.21 might have already completed at 3365.76. Overall outlook is unchanged that fall from 3451.28 is seen as the third leg of the corrective pattern from 3499.79 high. Break of 3248.21 will target 100% projection of 3451.28 to 3248.21 from 3365.76 at 3162.69, or even further to 3120.34 support.

In Europe, at the time of writing, FTSE is up 0.69%. DAX is up 0.38%. CAC is up 0.22%. UK 10-year yield is down -0.048 at 4.57. Germany 10-year yield is down -0.024 at 2.603. Earlier in Asia, Nikkei rose 0.06%. Hong Kong HSI fell -0.63%. China Shanghai SSE rose 0.18%. Singapore Strait Times rose 0.22%. Japan 10-year JGB yield rose 0.011 to 1.443.

US NFP growth solidly by 147k in June, wage pressures ease

US non-farm payrolls rose 147k in June, above the expected 110k and broadly in line with the 12-month average of 146k. Unemployment rate unexpectedly dropped from 4.2% to 4.1%, helped in part by a small dip in the participation rate to 62.3%. Overall, the data suggest that the labor market remains stable, with no clear signs of deterioration that would force the Fed’s hand in July.

However, wage growth continues to cool. Average hourly earnings rose just 0.2% mom and 3.7% yoy, both missing expectations of 0.3% mom and 3.9% yoy, and marking a further moderation from prior readings. This combination of solid hiring and easing wage pressure may support the case for a rate cut later in the year, but is unlikely to shift the Fed’s stance in the near term.

ECB accounts: June rate cut as safeguard against prolonged inflation undershoot

ECB’s June meeting minutes revealed that “almost all members” supported the 25bps deposit rate cut to 2.00%. Policymakers viewed the move as a safeguard to ensure “temporary undershoot in headline inflation did not become prolonged”, ensuring the 2% target remains intact through 2027. The cut was also framed as positioning rates in “broadly neutral territory,” giving the ECB room to maneuver in either direction as needed.

While some officials initially favored leaving rates unchanged to allow more time to assess inflation outlook, they ultimately aligned with the majority view. One member, however, dissented. The majority concluded that delaying a cut increase the risk of “undershooting the inflation target in 2026 and 2027”.

Overall, the ECB emphasized the need for full flexibility going forward. Given elevated global uncertainty and potential for rapid changes in inflation dynamics in both directions, the account stressed a “two-sided perspective” on inflation risks and a deliberate avoidance of forward guidance.

Eurozone PMI services finalized at 50.5, significance of services inflation receding into the background

Eurozone PMI Services was finalized at 50.5 in June, up from 49.7 in May. Composite PMI ticked up to 50.6 from 50.2. Although the bloc returned to modest expansion, performance remained uneven across major economies. Germany hit a three-month high at 50.4, while France fell to 49.2. Ireland, despite slowing to a five-month low, remained the strongest performer at 528. Spain (52.1) saw a slight pickup, while Italy’s reading slipped to 51.1.

Cyrus de la Rubia of Hamburg Commercial Bank noted that the services sector has been “more or less stagnant” since April. Nevertheless, Persistent labor shortages have discouraged firms from cutting jobs, helping stabilize private consumption. But a full recovery still looks elusive, with structural weaknesses continuing to weigh on growth momentum across much of the bloc.

Notably, rising input and output prices in services could be an unwelcome sign for the ECB. However, de la Rubia emphasized that broader disinflationary forces, such as Euro strength and tariff-driven downside risks, may outweigh the uptick in services inflation. While price pressure in services remains on the radar, it’s significance is “receding somewhat into the background”.

UK PMI services finalized at 52.8, a 10-month high

UK PMI Services was finalized at 52.8 in June, up from May’s 50.9, marking the fastest pace of expansion since August 2024. Composite PMI also rose to 52.0, the highest since September. The data signals a modest but broadening recovery, driven by improving domestic demand. S&P Global’s Tim Moore noted that consumer and business spending showed signs of a turnaround after a sluggish spring.

However, the rebound was tempered by “shrinking export sales”, with survey respondents citing pressures from US tariffs and geopolitical uncertainty. Additionally, firms were “reluctant to turn on the hiring taps”, marking the ninth straight month of job shedding.

For the BoE, input cost inflation slowed noticeably, helping to ease pressure on output prices, which saw their weakest rise in over three years. With price pressures softening and labor markets cooling, today’s report strengthens the case for the BoE to deliver another rate cut in August.

Swiss CPI returns to positive territory at 0.1% yoy in June

Swiss consumer prices surprised slightly to the upside in June, with headline CPI rising 0.2% mmm and turning positive on an annual basis at 0.1% yoy, reversing May’s -0.1% yoy print. Core CPI also firmed to 0.6% yoy from 0.5% yoy, suggesting that underlying inflation pressures remain subdued but stable.

Domestic prices were the key driver, up 0.2% mom and 0.7% yoy. Imported goods remained weak—flat on the month and still down -1.9% yoy despite an improvement from May’s -2.4% yoy.

BoJ’s Takata sees “True Dawn” for Japan, urges caution but not pessimism on tariffs

BoJ board member Hajime Takata said in a speech today that Japan may finally be emerging from decades-long economic stagnation. Reflecting on the structural decline since the 1990s, driven by the collapse of the bubble economy and intensifying global competition, Takata noted that while firms built resilience through deleveraging and restructuring, this also entrenched a low-investment, low-wage, and low-price “norm”.

Takata argued Japan is “finally beginning to break free of this norm”. Recent shifts in corporate pricing and wage behavior suggest Japan could be on the cusp of a sustained recovery. Still, he warned that US tariff policies risk derailing progress, recalling how similar global shocks in the 2000s repeatedly interrupted Japan’s economic revivals.

Yet’s Takata’s confident that this time could mark a “true dawn” and emphasized that being “overly pessimistic also poses a considerable risk”. He noted that the BOJ should maintain its accommodative stance for now, but also continue “gradually and cautiously” transitioning policy as conditions allow. Japan, he said, has a history of enduring far more intense trade tensions and should avoid falling into excessive pessimism.

Japan’s PMI composite finalized at 51.5, recovery fragile on sluggish demand

Japan’s private sector posted modest gains in June, with the final PMI Services index rising to 51.7 from 51.0 and the Composite index improving to 51.5 from 50.2 in May. The latest data signalled continued expansion, though momentum softened compared to the first quarter. S&P Global’s Annabel Fiddes noted that second-quarter PMI readings suggest a slowdown in GDP growth.

“Demand conditions remained sluggish” as new business rose only fractionally for the second month, and new export orders continued to decline. Firms are still struggling to gain traction amid US tariff uncertainty.

Meanwhile, inflationary pressures persisted. Businesses reported “strong cost pressures”, partly due to rising staffing levels. These costs were passed on through quicker hikes in output prices, despite muted demand.

China’s Caixin PMI services PMI falls to 50.6, but composite returns to growth

China’s Caixin PMI Services dropped to 50.6 in June from 51.1, missing expectations of 51.0. However, the broader PMI Composite rose from 49.6 to 51.3, marking a return to growth territory driven largely by stronger manufacturing activity. Caixin’s Wang Zhe noted that while supply and demand both improved, the rebound remains uneven and fragile.

Still, the data suggest mounting challenges. Employment continued to contract, and firms were forced to cut selling prices at the fastest rate in over a year, squeezing profitability despite stable input costs. Optimism weakened amid ongoing uncertainty, with business sentiment falling below its long-term average.

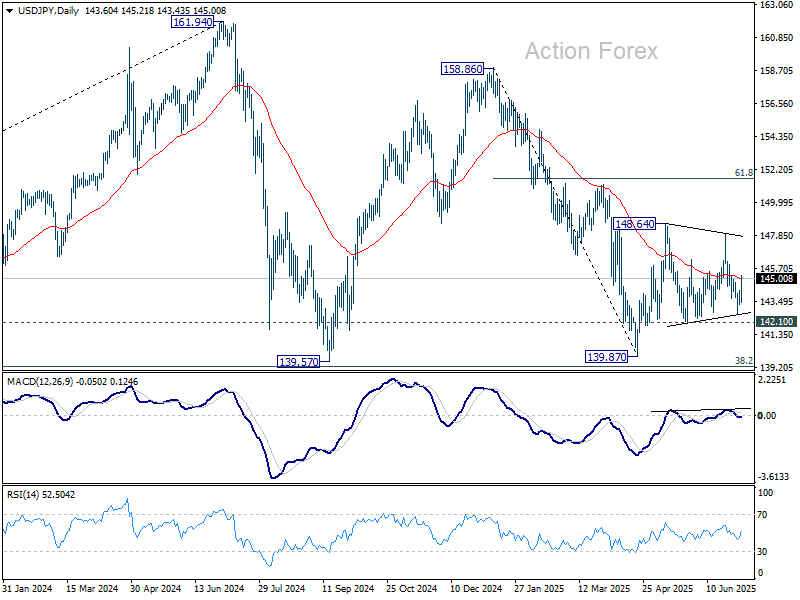

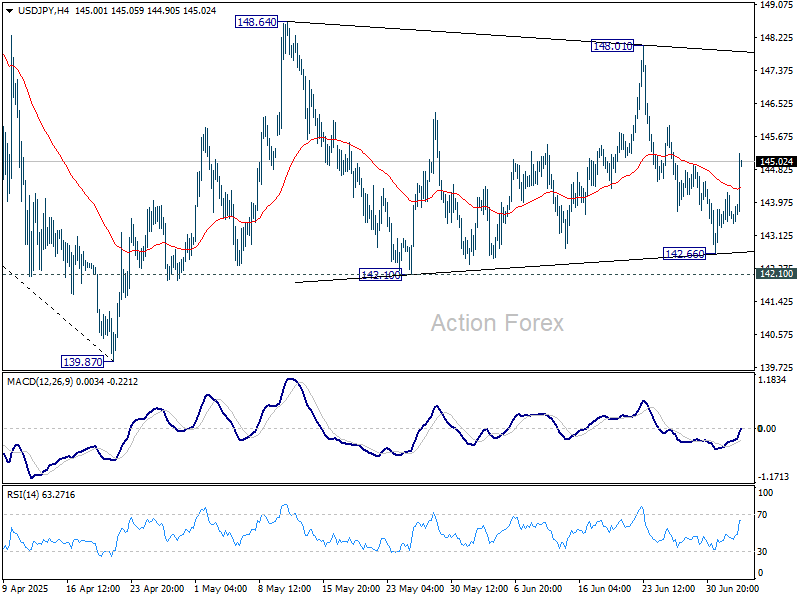

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.24; (P) 143.74; (R1) 144.17; More…

USD/JPY’s rebound suggests that fall from 148.01 might have completed at 142.66. But still, it’s staying inside near term established range. Intraday bias remains neutral at this point. On the upside, firm break of 148.01 resistance will resume the rise from 139.87 to 61.8% retracement of 158.86 to 139.87 at 151.22. However, break of 142.10 will bring deeper fall back to retest 139.87 low.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.